|

|

| Morning Review | Jul 2, 2026 |

|

This e-mail is intended for Sample Report only. Note that systematic forwarding breaches subscription licence compliance obligations. Open in browser | Edit Countries on Top

We have launched coverage of Bangladesh |

|

| Large EMs |

|

| Czech Republic |

|

|

|

|

|

|

| Hungary |

|

|

|

|

|

|

|

|

| Poland |

|

|

|

|

|

| Turkey |

|

|

|

|

|

| Argentina |

|

|

|

| Brazil |

|

|

|

|

|

|

|

|

| Mexico |

|

|

|

|

|

|

|

|

|

| Egypt |

|

|

|

|

| Nigeria |

|

|

|

|

|

|

|

| India |

|

|

|

|

|

|

|

|

| Indonesia |

|

|

|

|

|

| Pakistan |

|

|

|

| Philippines |

|

|

|

|

|

| CEE |

|

| Albania |

|

|

| Bosnia-Herzegovina |

|

|

|

|

|

|

| Bulgaria |

|

|

|

| Croatia |

|

|

|

|

|

|

|

| Latvia |

|

|

| Lithuania |

|

|

| Montenegro |

|

|

| North Macedonia |

|

|

| Romania |

|

|

|

|

|

|

|

|

|

|

| Serbia |

|

|

|

|

| Slovakia |

|

|

|

|

|

|

|

|

| Ukraine |

|

|

|

|

|

|

|

|

|

|

| CIS & Central Asia |

|

| Armenia |

|

|

|

|

|

| Azerbaijan |

|

|

| Georgia |

|

|

|

| Kazakhstan |

|

|

|

|

|

|

|

| Kyrgyzstan |

|

|

|

| Mongolia |

|

|

| Russia |

|

|

|

|

|

|

|

|

|

|

| Tajikistan |

|

|

|

|

|

|

|

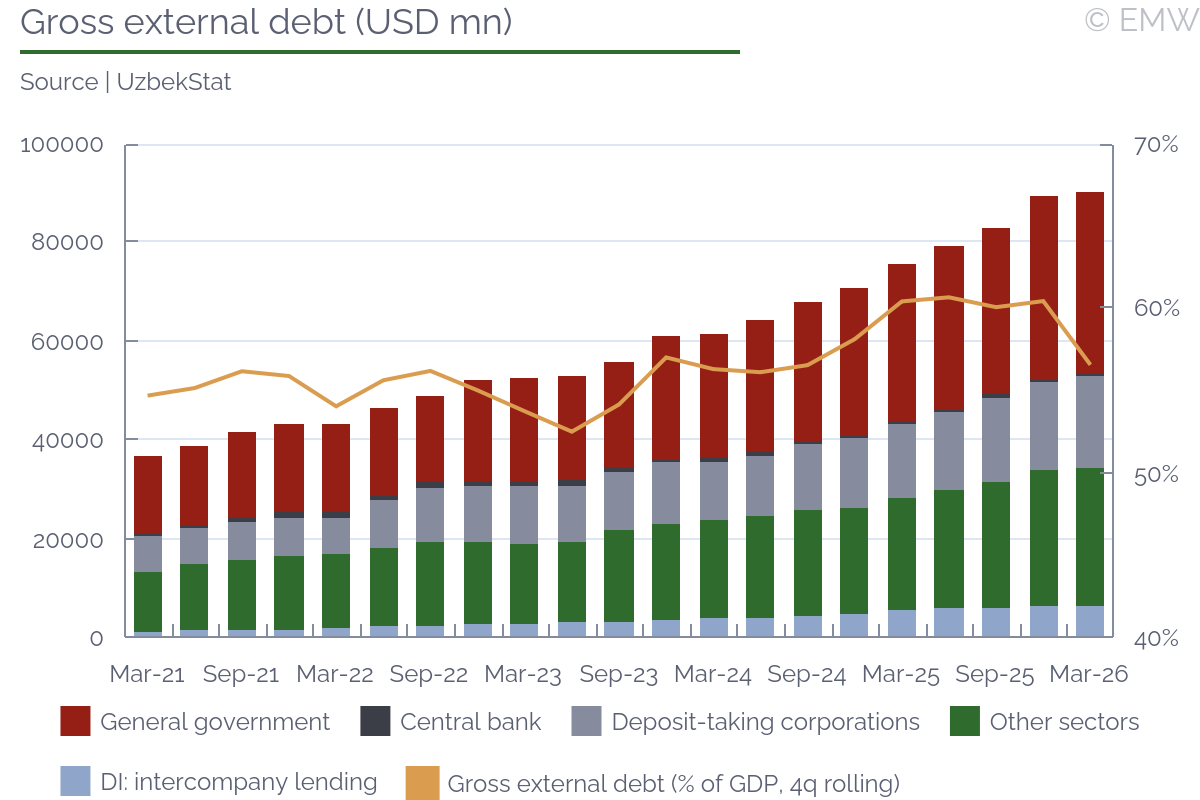

| Uzbekistan |

|

|

|

|

|

| Latin America |

|

| Chile |

|

|

|

|

| Colombia |

|

|

|

|

|

|

| Costa Rica |

|

|

|

|

| Dominican Republic |

|

|

|

| Ecuador |

|

|

|

| El Salvador |

|

|

|

| Panama |

|

|

|

| Peru |

|

|

|

|

| Venezuela |

|

|

|

|

|

| Middle East & N. Africa |

|

| Israel |

|

|

|

|

|

|

|

|

|

| Jordan |

|

|

|

| MENA |

|

|

| Morocco |

|

|

| Qatar |

|

|

| Saudi Arabia |

|

|

| Tunisia |

|

|

|

|

| Sub-Saharan Africa |

|

| Angola |

|

|

| Ethiopia |

|

|

|

|

| Gabon |

|

|

|

| Ghana |

|

|

|

|

| Ivory Coast |

|

|

|

| Kenya |

|

|

|

|

|

|

|

| Mozambique |

|

|

|

|

| Senegal |

|

|

|

|

|

|

|

| South Africa |

|

|

|

|

|

|

|

| Uganda |

|

|

|

| Zambia |

|

|

|

|

|

|

| South & Southeast Asia |

|

| Bangladesh |

|

|

|

| Malaysia |

|

|

|

|

| South Korea |

|

|

|

|

|

|

|

|

| Sri Lanka |

|

|

|

|

|

|

|

|

|

| Thailand |

|

|

|

|

|

| Vietnam |

|

|

|

|

|

| Czech Republic |

|

|

| Czech Republic | Jul 02, 06:31 |

|

Only USD 2.5mn Tomahawks were in the thousands. How the war with Iran bled the US dry (Lidove Noviny) Skoda manager: There will never be a Fabia for CZK 300,000 any more (Mlada Fronta Dnes) Dead souls and other people's data. A new report adds jobs to companies (Pravo) Prospective investors flock to Bubny. Komarek, Kellnerova, and Strnad want to build there (Hospodarske Noviny) Kremlin needs to import petrol (Pravo) What faces Rehka's successor [as chair of the general staff], Hlavac? (Hospodarske Noviny) Solek is already being divvied up. A part of "priceless" Green project ends up in J&T's fund (E15) Prague to have two direct links to Saudi Arabia. Lines to be served three times a week (Lidove Noviny) Google's tradition continues, it paid almost no taxes in the Czech Republic. Sales were transferred through Ireland (E15) Football boss wants a foreign coach and a full restart (Mlada Fronta Dnes) |

|

|

|

| Finance ministry sells CZK 80bn of retail bonds in May and June |

|

| Czech Republic | Jul 01, 14:01 |

|

- The original plan was for sales of about CZK 20bn

- A new round of retail bond sales is planned to start in late August

The finance ministry sold about CZK 80bn of retail bonds in its latest issue, which launched in mid-May, according to a press release. Originally, the finance ministry planned to sell about CZK 20bn, but demand turned out to be much stronger than expected. There were three types of bonds on offer - a fixed income one, an inflation-indexed one, and a revolving investment one. A new round of retail bond sales is planned to start in late August. The stronger-than-expected sale has not had a major impact on regular government bond issuance, at least for now. However, the finance ministry has been setting lower borrowing ceilings lately, which could have been impacted by the retail bond issues. It will likely embolden the finance ministry, as it can have more control over borrowing terms that way. |

|

|

|

| Finance ministry again raises maximum fuel prices slightly |

|

| Czech Republic | Jul 01, 13:55 |

|

- Maximum petrol prices will rise by 0.2% d/d, while maximum diesel prices will increase by 0.4% d/d

- We expect maximum fuel prices to ease a bit in the coming days

The finance ministry delivered one more slight increase in maximum fuel prices, which will apply on Thursday (Jul 2), according to a press release. The cap on petrol prices will rise by 0.2% d/d, while the cap on diesel prices will be higher by 0.4% d/d. This is the same rate of increase as the cap applying on Wednesday (Jul 1). As a result, maximum petrol prices will be higher by 0.2% w/w, while maximum diesel prices will be higher by 1.2% w/w. Maximum fuel prices are calculated through a 3-day moving average of wholesale prices, and there was a slight increase late last week, which has likely led to the current increase. However, oil prices have eased since then, so we expect maximum fuel prices to be lowered in the coming days. In any case, the latest developments suggest only a slight increase in fuel prices, by about 0.5% w/w in the first week of July. | Fuel price caps, CZK/l | | Date | Petrol | Change, d/d | Change, w/w | Diesel | Change, d/d | Change, w/w | | 08-Apr | 43.15 | | | 49.59 | | | | 30-Apr | 43.13 | 0.8% | 4.9% | 43.51 | -1.4% | 5.7% | | 29-May | 43.58 | -1.3% | -3.6% | 40.26 | -1.4% | -4.8% | | 30-Jun | 40.47 | 0.0% | -0.1% | 36.47 | 0.2% | -0.2% | | 1-Jul | 40.56 | 0.2% | 0.0% | 36.61 | 0.4% | 0.7% | | 2-Jul | 40.64 | 0.2% | 0.2% | 36.74 | 0.4% | 1.2% |

| | Note: Final price, excise tax and VAT included | | Source: Ministry of Finance |

|

|

|

|

| | State government budget reports a deficit of CZK 183.6bn in H1 2026 |

|

| Czech Republic | Jul 01, 13:40 |

|

- The budget reported a deficit of CZK 13.4bn in June, compared to a surplus of CZK 18.2bn a year ago

- The end of windfall tax collection at the end of 2025 led to a much slower revenue growth in 2026

- It was only partially mitigated by delayed payments from the EU budget from late 2025

- Spending growth picked up to 6.2% y/y, with a big impact of capital expenditure, which rose by 25.8% y/y

- This government has decided to spend much more on motorway construction, which will boost deficits

- We see it as more likely than not that this year's deficit target of CZK 310bn will be missed

The state government budget reported a deficit of CZK 183.6bn (2% of GDP) in H1 2026, higher by 20.5% y/y, according to figures from the finance ministry. In June alone, the budget reported a deficit of CZK 13.4bn, compared to a surplus of CZK 18.2bn a year ago. We should note that there are some base effects in play, like windfall tax, whose collection ended at the end of 2025. Furthermore, this government stepped up on capital expenditure, spending a lot more on transport infrastructure than the previous one. As a reminder, the deficit target is currently at CZK 310bn in 2026. Nevertheless, revenues and expenditure are not spread evenly throughout the year, so performance thus far is not a strong indication of whether the full-year target will be met.  Revenues rose by 4% y/y in H1, primarily because of social contributions, whose collection was stronger by 6.4% y/y. There is a strong impact from windfall tax, whose collection ended at the end of 2025. If we exclude windfall tax, revenue would rise by 6.2% y/y, while tax revenue would be higher by 5.2% y/y, against 2.8% y/y in the current report. The other strong growth driver was gross EU flows, which increased by 36.5% y/y. This is mostly due to RRF payments, as well as to a one-off windfall, as some payments from the EU budget due in late 2025 were delayed to early 2026. As a reminder, the state government budget is reported on a cash basis, which can be impacted by one-off developments. Expenditure increased by 6.2% y/y, and it is no longer under the impact of the provisional budget that was applied during most of Q1. Capital expenditure took over as the main source of spending growth, rising by 25.8% y/y. This is primarily because this government has started to spend much more on transport infrastructure projects, primarily motorway construction. Social spending followed closely with a 4.4% y/y increase, out of which pension spending was higher by 3.9% y/y. Moreover, the Czech contribution to the EU budget increased by 45.5% y/y, reflecting a higher GNI and upward revisions of past GNI data. Personnel expenses rose by 6.4% y/y, along with the wage hikes granted to the public sector, while maintenance expenses were higher by 7.4% y/y, mostly due to pricier fuels. Overall, budget performance has started to reflect the policies of the current government, mostly through significantly higher public investment. The government has argued that this will pay off in the coming years, though there is doubt the government will be able to contain spending after the initial push. As a reminder, the ruling coalition plans plenty of measures that will reduce revenue and increase spending as of 2027, like a 2pp cut of the corporate income tax (to 19%), or restoring a faster indexation of pensions. On the optimistic side, this year's budget performance will benefit from about CZK 40bn of delayed payments from the EU budget, which may mitigate the spending increase. On the other hand, there is already a net inflow from the EU of CZK 20bn in H1, compared to a net outflow of CZK 1.6bn a year ago, which implies that budget performance is actually worse. As a reminder, the finance ministry already expects the general government budget to reach 2.6% of GDP in 2026, which suggests that the deficit target at state government level will be likely missed. | State government budget, January-June, CZK bn | | 2025 | 2026 | Change, % y/y | Change | Plan 2026 | % of plan | | REVENUE | 1,010.8 | 1,051.5 | 4.0 | 40.7 | 2,118.0 | 49.6 | | Tax revenue | 919.3 | 945.1 | 2.8 | 25.8 | 1,915.5 | 49.3 | | VAT | 194.1 | 201.0 | 3.5 | 6.9 | 416.0 | 48.3 | | Excise tax | 79.3 | 80.7 | 1.8 | 1.4 | 170.1 | 47.5 | | Corporate income tax | 120.5 | 125.6 | 4.2 | 5.0 | 227.9 | 55.1 | | Personal income tax | 89.0 | 96.1 | 8.1 | 7.2 | 196.0 | 49.0 | | Windfall tax | 21.7 | 0.6 | n/m | -21.1 | 6.9 | 8.4 | | Social and healthcare contributions | 398.4 | 424.0 | 6.4 | 25.6 | 867.7 | 48.9 | | Retirement contributions | 352.0 | 374.4 | 6.4 | 22.4 | 761.7 | 49.2 | | Other taxes | 16.2 | 17.0 | 4.9 | 0.8 | 30.8 | 55.1 | | Non-tax and capital income, o/w: | 91.5 | 106.4 | 16.3 | 14.9 | 202.5 | 52.5 | | EU transfers | 60.9 | 83.1 | 36.5 | 22.2 | 139.4 | 59.6 | | Property income | 7.0 | 7.4 | 6.0 | 0.4 | 21.3 | 34.7 | | | | | | | | | EXPENDITURE | 1,163.1 | 1,235.1 | 6.2 | 71.9 | 2,428.0 | 50.9 | | Current expenditure | 1,082.5 | 1,128.6 | 4.3 | 46.1 | 2,166.9 | 52.1 | | Personnel | 71.8 | 78.2 | 8.9 | 6.4 | 197.4 | 39.6 | | Maintenance | 88.9 | 95.4 | 7.4 | 6.5 | 217.0 | 44.0 | | Interest | 47.8 | 50.7 | 6.1 | 2.9 | 110.0 | 46.1 | | Transfers | 411.8 | 409.5 | -0.6 | -2.3 | 680.8 | 60.2 | | Social expenses | 462.0 | 482.2 | 4.4 | 20.2 | 949.1 | 50.8 | | o/w: pensions | 357.9 | 371.9 | 3.9 | 14.0 | 738.8 | 50.3 | | Contribution to EU budget | 28.3 | 41.2 | 45.5 | 12.9 | 70.7 | 58.3 | | Other current expenses | 19.6 | 22.0 | 12.4 | 2.4 | 52.0 | 42.4 | | Capital expenditure | 80.7 | 106.5 | 32.0 | 25.8 | 261.1 | 40.8 | | o/w: transfers | 65.6 | 80.9 | 23.3 | 15.3 | 161.0 | 50.2 | | | | | | | | | BALANCE | -152.4 | -183.6 | 20.5 | -31.2 | -310.0 | 59.2 | | EU flows | -1.6 | 20.0 | n/m | 21.6 | 0.0 | n/m | | Non-EU balance | -150.8 | -203.6 | 35.1 | -52.9 | -310.0 | 65.7 |

| | Source: Ministry of Finance |

|

|

|

|

| Satisfaction with government performance reaches 29% - poll |

|

| Czech Republic | Jul 01, 13:03 |

|

- 41% are unhappy with the government

- Yet, the opposition gets poor marks as well, since only 18% are happy with its performance

- PM Babis (ANO) is the highest-rated party leader, followed by lower house speaker Okamura (SPD)

Satisfaction with the government's performance reached 29%, according to the latest opinion poll of STEM, carried out on Jun 16-21. Meanwhile, the share of people unhappy with the government reached 41%. There is a sharp split across party lines, as two thirds of ANO's voters are happy with the government that the party leads. Supporters of the two junior partners, the SPD and the Motorists, are less supportive, but support is higher than disapproval. Meanwhile, more than 80% of opposition voters are unhappy with the current government. Meanwhile, only 18% are satisfied with the opposition, and 46% are not. Again, opposition voters have expressed much greater support than supporters of the government. An earlier poll from the same pollster shows that PM Andrej Babis (ANO) is the party leader held in the highest regard, followed by lower house speaker Tomio Okamura (SPD), and Martin Kuba (Our Czechia), who is not even an MP. Among opposition parties, the highest-rated leader is Vit Rakusan (STAN), who is ahead of foreign minister Petr Macinka (Motorists) and Martin Kupka (ODS). Thus, while voters might not be completely happy with the current government, they don't see a strong alternative in the current parliamentary opposition. |

|

|

|

| Hungary |

|

| | State debt manager raises 84.8% of net issuance plan in H1 |

|

| Hungary | Jul 02, 06:42 |

|

- Issuance of forint debt exceeds pro-rata level for period, forex debt issuance is close

- AKK warns debt financing plan will be revised in case of 2026 budget revision

The State Debt Management Agency (AKK) issued net HUF 4,615bn of government debt in H1, the AKK announced. The net issuance represented 84.8% of the annual plan for 2026. A high execution ratio was achieved in the areas of retail securities and forint wholesale government securities. Specifically, the net issuance of wholesale domestic securities exceeded the annual target by around 50%. We think the strong execution ratio was partly helped by solid demand as of April when investor interest was significantly boosted by the outturn of the parliamentary elections. Gross issuance of wholesale forint debt was at 57.8% of the full-year plan, in our opinion showing that uneven expiries in the course of the year partly contributed to the overachievement of the net issuance target. The gross issuance execution was still above the pro rata level for the period, confirming the conclusion of favourable government access to this financing channel. The execution ratios were above the prorated levels planned for H1 in the case of the forint and overall financing, while it was close to the prorated levels in the case of forex financing, the AKK confirmed. Net issuance of forex debt came at 45.2% of the annual target and gross forex debt issuance - at 47.0%. Hungary raised USD 3.0bn of forex bonds in January and an additional USD 1.2bn of bonds in February, compared to the full-year forex bond issuance programme of EUR 5.2bn. The AKK had also planned to tap the Asian markets via a EUR 500mn placement this year, but we suspect these plans might be revisited with the new management after the government transition. The previous Fidesz government had regularly issued on the Panda market for the sake of building good relations with China, while the new Tisza government has not appeared enthusiastic to continue this general policy, we assess. A prospective revision of the 2026 budget will also require a revision of the financing plan, the AKK explicitly warned. The 2026 financing target has been based on an assumption of a budget deficit of 5.0% of GDP, while PM Peter Magyar recently signalled that the actual deficit could be north of 7%, we note. | Government debt issuance, H1 2026 | | Gross | Net | | HUF bn | % of annual plan | HUF bn | % of annual plan | | Retail securities | 2,729.0 | 59.1% | 988.0 | 76.0% | | Forint institutional debt | 4,977.0 | 57.8% | 2,476.0 | 154.5% | | Forex securities and loans | 1,675.0 | 47.0% | 1,151.0 | 45.3% | | Total issuance | 9,381.0 | 55.8% | 4,615.0 | 84.8% |

| | Source: AKK |

|

|

|

|

|

| Hungary | Jul 02, 06:30 |

|

Tisza government launches campaign against countryside (Magyar Nemzet) Purge continues, PM Peter Magyar also fires president of media regulator (Magyar Nemzet) Chinese battery producer Semcorp must leave Debrecen (Magyar Nemzet) Oil and gas group MOL receives new US approval to continue NIS negotiations (Magyar Nemzet) PM Peter Magyar makes extraordinary announcement: Hundreds of thousands of Hungarian families will receive school start support (Vilaggazdasag) Croatia resurrects its dead steel factory while Hungarian Dunaferr is living its last days (Vilaggazdasag) Chinese battery factory CATL announces: Production can start at any time, it only needs official permits (Vilaggazdasag) Glass is full in Debrecen: Fidesz mayor Laszlo Papp does not want any scandals, demands immediate departure of battery giant Semcorp (Vilaggazdasag) President Tamas Sulyok dismisses president of media regulator at suggestion of PM Peter Magyar (Heti Vilaggazdasag) Median: Tisza euphoria persists, Fidesz voters are decreasing (Heti Vilaggazdasag) Here is balance sheet of NBH Foundation: Not even a tenth of initial public assets (Heti Vilaggazdasag) Politico: EC investigation finds that spy group operating at Hungarian permanent representation in Brussels targeted EU officials (Heti Vilaggazdasag) PM Office head Balint Ruff has initiated extraordinary parliamentary session for next week as well (Heti Vilaggazdasag) |

|

|

|

| Ruling Tisza solidifies its popularity lead – poll |

|

| Hungary | Jul 01, 14:54 |

|

- Tisza leads with 73% on Fidesz' 21% among decided voters certain to vote

- Poll captures impact of Tisza's efforts to dismiss President Tamas Sulyok, we note

- Our Homeland maintains levels of support around 5% parliamentary threshold

The ruling Tisza Party has solidified its popularity advantage after taking office, the latest Median poll showed, commissioned by the HVG portal. Tisza attracted 60% of support among all voters, down by 1pp m/m. The decline was within the statistical margin of error, while the main opposition party, Fidesz, shed 3pps m/m to just 18%, the pollster pointed out. Tisza had substantial support of 71% among decided voters and 73% among voters certain to vote, compared to 21% for Fidesz in each of these two samples. Tisza's lead among decided voters certain to vote expanded by 5pps m/m, seemingly due to a continued transfer of voters from the Fidesz to the Tisza camp. Voting discipline has weakened among Fidesz voters, the pollster observed, which we consider expected after Tisza's sweeping win in the Apr 12 parliamentary elections. The survey was conducted in the Jun 22-29 period, so it should have captured voter sentiment towards the anti-corruption strategy and controversial draft constitutional amendment of Tisza, we note. The amendment will, among other things, terminate the mandate of President Tamas Sulyok immediately after it enters into force and will set a limit of the number of years served as MP. Both provisions have been disputed as unacceptable or borderline acceptable in a democratic context by some legal and political analysts, we note. In this context, the poll results could be read as a signal that voters might implicitly give a mandate to Tisza to dismiss Sulyok, in our view. Such a conclusion cannot be definitive though and warrants a high degree of caution, we warn. Nationalist Our Homeland has maintained support around the parliamentary threshold of 5%, while liberal DK had only 1%, the poll showed. |

|

|

|

| Finance ministry to re-write budgetary procedure |

|

| Hungary | Jul 01, 14:27 |

|

- Government to have to submit draft budgets to parliament in Oct 1-31 period

- Detailed rules of new budget procedure to be presented by end-August

The finance ministry will entirely re-write the procedure for the drafting of the budget, finance minister Andras Karman announced in a social media post. The government will definitely do away with the practice of the previous Fidesz administration of submitting the draft budgets in the spring, since they needed to be revised many times afterwards, worsening the predictability of fiscal policy, he said. The 2027 budget will be prepared according to the new procedure, which will bring the planning and the start of the fiscal year closer together in order to set a realistic basis for the budget, he pointed out. This will mean that the government will have a deadline to submit the draft budget to the parliament in the Oct 1-31 range, he specified. A detailed account of the new budget procedure will be published at the end of August, Karman promised. The new rulebook for drafting the budget will aim to improve transparency, ensure stronger parliamentary control and realistic budget planning. The reform will also result in better monitoring of the use of public funds. It will not introduce any changes to the general order of institutional cooperation in the process. Budgetary units will send their proposals to the finance ministry, which will consolidate them into a state budget proposal after consultations. The draft budget will be subsequently sent to the Fiscal Council watchdog for opinion and will afterwards be submitted to the parliament. The ministry will expect more conservative and realistic revenue planning from budgetary units compared to the previous years, according to the announcement. Units will be also required to submit detailed justification for the amount of public funds they request, linking them to specific policy goals or quality and quantity of services provided. |

|

|

|

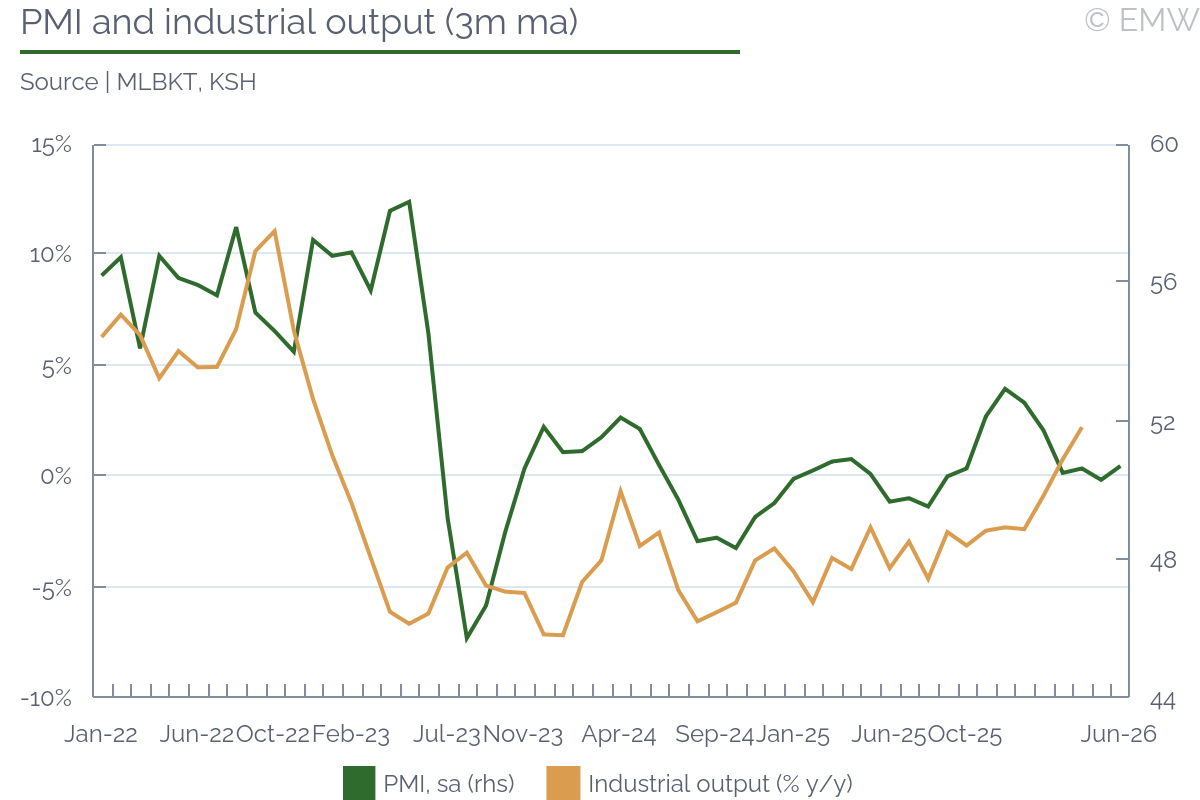

| PMI rises by 1.3pts m/m to 51.5pts in June |

|

| Hungary | Jul 01, 14:04 |

|

- Favourable PMI signal might show up in actual manufacturing performance this time, we expect

- Output, demand increase at accelerating pace, but hiring plans remain subdued

The Purchasing Managers' Index (PMI) rose by 1.3pts m/m to 51.5pts in June, the logistics association Halpim reported. The print thus showed strengthening growth in manufacturing activity. On the other hand, industrial output has been mostly in negative territory for the past couple of years, although the latest data did show some tentative signs for a gradual rebound, we note. We therefore maintain our caution that the PMI has not been a good predictor of manufacturing trends lately but this time, there is a good chance for the positive PMI signal to materialise in the actual performance of the sector. Both the production and new order indices improved by 2.2pts and by 3.7pts, respectively, signalling accelerating expansion of output and demand. Conversely, employment intentions remained subdued, falling m/m and signalling a contraction. Margin pressures likely discouraged manufacturers from using the demand increase to create jobs and the strengthening of the forint exchange rate possibly added to this pressure, we believe. The delivery lead times sub-index improved by 3.4pts m/m, in our opinion possibly due to increased optimism for supply chain repair after the seeming de-escalation of the Middle East conflict. The delivery lead times sub-index remained below the neutral threshold of 50pts, the survey showed. |

|

|

|

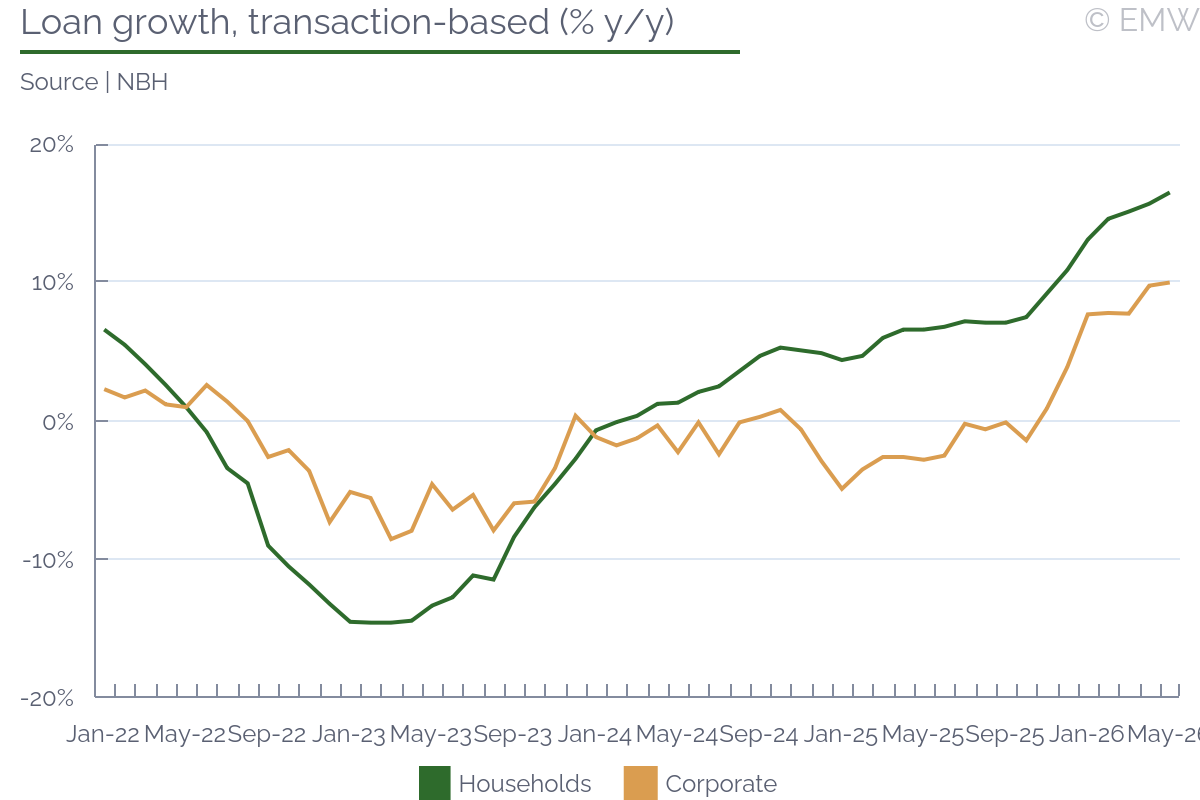

| | Lending growth slows down to 11.4% y/y at end-May |

|

| Hungary | Jul 01, 13:38 |

|

- Slowdown masks sustained underlying borrowing demand in corporate, retail sectors

- High corporate loan growth does not necessarily mean better investment prospects, we caution

- Demand for subsidised housing loan programme remains stable

The outstanding stock of bank loans to the private sector rose by 11.4% y/y at end-May and slowed down from the 11.9% y/y increase in the previous month, according to the monetary statistics of the National Bank of Hungary (NBH). The print represented some turnaround of the upward trend in the series, which stemmed from the corporate loan portfolio. New corporate loans, however, maintained robust dynamics, in our opinion defending the overall impression of still solid underlying borrowing demand. Part of the growth of corporate loans was likely related to the working loan pillar of the subsidised loan programme, which has been recently temporarily shut down to prevent companies from using the resources for riskless arbitrage instead of business development, we note. In this context, the strong growth of corporate loans might not necessarily mean prospects for rebound in private investment activity, we caution.  Corporate loans increased by 10.0% in real-, transaction-based terms in May, accelerating further after the 9.8% y/y growth in the previous month. Non-financial companies borrowed net HUF 61.1bn of bank loans in May and the new borrowing consisted entirely of forint loans. Seasonally-adjusted new loan volumes confirmed the pattern for relatively high corporate borrowing demand in the month, we note. Interest rates on forint loans edged down m/m in May, closing slightly the gap to the interbank market borrowing rate in the case of large forint loans. The interest rate on corporate EUR loans remained more volatile but exhibited a flat trajectory on average in the past few months. New retail loan growth picked up further to 16.5% y/y in the month. It extended its upward trajectory, in our opinion helped to a large extent by the popular home subsidy programme. The monthly volumes of new housing loans have maintained roughly unchanged since the programme's introduction in Sep 2025, showing sustained interest in the programme. Demand for loans under the programme could thus ensure solid loan growth on a y/y basis until October when the impact of the programme will enter the base and depress the y/y dynamics, we expect. In addition, the monthly volumes of new consumer loans have shown gradual a increase in the past few months. This growth should probably include the career start-up loan programme but might also indicate gradual improvement in consumer spending propensity, we assess. Consumer loan demand was likely helped by a gradual decline in interest rates, the data suggested. |

|

|

|

| State debt manager AKK reduces six-month T-bill issuance on primary auction |

|

| Hungary | Jul 01, 12:52 |

|

- Yield continues to decline compared to previous tender

The State Debt Management Agency (AKK) sold HUF 24.0bn of six-month T-bills on the latest primary auction, AKK data showed. The issued amount was HUF 6.0bn lower than originally planned for the auction, as the AKK reacted to relatively weak demand. Total bids amounted to HUF 33.2bn, slightly less than on the previous auction two weeks ago. Demand provided a modest 1.1x bid-to-cover ratio against supply. The average yield dropped further by 14bps from the previous tender to 5.32%, also landing below the three-month yield from yesterday's primary tender. The six-month yield was still 7bps higher than the secondary market benchmark rate. |

|

|

|

| Poland |

|

|

| Poland | Jul 02, 03:51 |

|

Without govt program, fuel prices increase, but not everywhere [BenzynaMAPA says avg PB95 price was PLN 6.25/l and avg diesel price was PLN 7.10, up from final max price of PLN 6.00 and PLN 6.19, but prices said to vary widely] (Rzeczpospolita) Fuel-tax cut program defused political bomb (Rzeczpospolita) Coalition partners are concerned over KO's Southern Hospital crisis (Gazeta Wyborcza) Electronics prices are rising due to a small item [i.e., memory] (Rzeczpospolita) Banning the promotion of Banderism is a good idea [PL-UA history row continues] (Rzeczpospolita) Zelensky is not interested in UPA (Rzeczpospolita) We think less and less of Ukrainians (Rzeczpospolita) Anti-Ukrainian sentiment is becoming more widespread and more strident [Ukrainians make up 22% of workers in manufacturing, 18% in construction, 14% in retail, 11% in hotel and gastronomy, 10% in care, and 9% in transport] (Gazeta Wyborcza) Fight for next EU budget has begun (Rzeczpospolita) Europe is heating up at a record pace (Rzeczpospolita) Men who feel aggrieved are ganging up to exact revenge on women [front-page story] (Gazeta Wyborcza) |

|

|

|

| | MPC set to hold rates and remain in neutral for now |

|

| Poland | Jul 01, 15:24 |

|

- Next MPC meeting: Jul 7-8, 2026

- Current policy rate: 3.75%

- EmergingMarketWatch forecast: 3.75%

Rationale: The Monetary Policy Council had already become much less hawkish and we believed a couple of weeks ago the only chance of a hike was a worsening of the situation in the Middle East, but after CPI inflation for June was flashed at a lower-than-expected 2.5% y/y, then that put paid to any chance of a hike. The Middle East conflict appears to have stabilised, and it is likely the US administration will eschew any true worsening of the situation ahead of the mid-term elections in November. That should mean global oil prices at the least don't rise. The fall of global oil prices has allowed the government to end the fuel-tax-cut program at end-June as well as the setting of maximum retail prices. Fuel prices will thus rise. The fuel-market monitoring company Reflex estimated last week that the ending of the government measure might raise fuel prices by around PLN 0.60 a litre. If that is the actual increase -- which will depend on where oil prices are when fuel stations adjust their prices -- the contribution of passenger fuel prices to annual headline CPI inflation will be about 0.5pp more in July. Though the MPC had moved much more dovish in recent weeks, the unwinding of bets on rate hikes has hit the PLN of late. The PLN has weakened in the past several days and that will help stoke inflation to one degree or another. This is likely to help the MPC stay on hold. The PMI reading for June, as released on Jul 1, was dismal, and the print is the worst in nearly a year. That would suggest weaker sentiment than might have been expected and would point in the direction of a weakening of the economy in Q2. Softer economic growth will work to assuage MPC fears of demand-push inflation and help the MPC become more dovish. The July Inflation Report will be ready for the Jul 7-8 MPC sitting and will include the updated CPI and GDP projections. Though there was a time when these updates were likely to be critical, that time has passed. The MPC will welcome the sketching in of the outlook, but it is likely to confirm rather that inflation pressure is not going to be a threat than provide a pretext for any decision. Overall, the MPC has clearly become more dovish in the past several weeks and the fact CPI inflation is at the target will only cement this. Fuel prices will rise, but that is an exogenous development the MPC is likely to ignore and wait till it fades out of the data. The weaker PLN will encourage caution, as will the still fraught geopolitical situation. In the end, we believe the MPC will likely confirm a 'wait-and-see' and data-dependent stance and only begin moving towards easing later in the year. | MPC breakdown | | Member | Backer | Date in | Date out | Pol. support | Last comments | Comment | | Adam Glapinski | Pres/Sejm | Jun. 22, 2022 | Jun. 22, 2028 | PiS | Jun. 3, 2026 | Becomes more dovish, though doesn't rule out hikes | | Wieslaw Janczyk | Sejm | Feb. 23, 2022 | Feb. 23, 2028 | PiS | Apr. 13, 2026 | Says rates to remain flat in coming quarters | | Gabriela Maslowska | Sejm | Oct. 6, 2022 | Oct. 7, 2028 | PiS | Jun. 9, 2026 | Sees less chance of hike, more of a cut this year | | Iwona Duda | Sejm | Oct. 6, 2022 | Oct. 7, 2028 | PiS | Jun. 18, 2026 | Baseline path is stable rates | | Ludwik Kotecki | Senate | Jan. 25, 2022 | Jan. 25, 2028 | PO/KO | Jun. 15, 2026 | Says rates might remain flat to end-Q1 2027 | | Przemyslaw Litwiniuk | Senate | Jan. 25, 2022 | Jan. 25, 2028 | PSL | May. 13, 2026 | Backs wait and see, sees chance of hikes | | Joanna Tyrowicz | Senate | Sep. 7, 2022 | Sep. 7, 2028 | KO/Left | May. 19, 2026 | Continues to back 100bps of hikes | | Ireneusz Dabrowski | President | Feb. 22, 2022 | Feb. 22, 2028 | PiS | Jun. 12, 2026 | Says a cut is now more likely than a hike | | Henryk Wnorowski | President | Feb. 22, 2022 | Feb. 22, 2028 | PiS | May. 14, 2026 | Sees flat rates until at least July | | Marcin Zarzecki | President | Dec. 22, 2025 | Dec. 22, 2031 | PIS | Jun. 10, 2026 | Says rates likely to remain flat or rise this year |

| | Source: NBP |

MPC's post-sitting statements Latest council minutes Latest NBP inflation report (March 2026) Most recent MPC voting results Archived video of all MPC press conferences |

|

|

|

| FinMin says cost of fuel-tax cut measures was PLN 4.7bn |

|

| Poland | Jul 01, 13:03 |

|

- FinMin has now fully ended the program, allowing fuel VAT to return Wed. to 23% from 8%

The Finance Ministry has put the total cost of its fuel tax cutting program at PLN 4.7bn, according to data reported Wed. by the PAP news agency. The program has now ended, and, from Wed., the VAT on fuels has returned to the standard 23% from the previously reduced 8%. The return of the VAT to the normal level has also ended the setting of maximum prices by the Energy Ministry. The reduction of the excise on petrol by PLN 0.29 a litre and diesel by PLN 0.28 a litre was ended on Jun 16. The program went into effect on Mar 31. "The program proved successful: it lowered costs for households and a large number of businesses, and kept inflation low-standing at 2.5 percent year-on-year in June," the ministry was cited saying. Overall, the monthly cost of the program was put at some PLN 1.7bn, and though the PLN 5bn is worth only some 0.1% of GDP, the strained budget situation makes each additional PLN 1bn a burden. The government does plan to offset the budget cost of the fuel tax cuts with a windfall tax on fuel companies that has been adopted by the Sejm [and which is being worked on by the Senate] and which is to raise PLN 3.8bn, putting the net cost of the measures at some PLN 1bn. The senior ruling Civic Coalition (KO) has been hit by a scandal involving local party officials in Warsaw, and the rise in fuel prices at fuel stations is not going to help. According to forecasts released last week by the fuel-market monitoring company Reflex, the return of the VAT on fuel to prior levels could up petrol and diesel prices by some PLN 0.60 a litre and that might add some 0.5-0.6pp to inflation in July, we estimate. |

|

|

|

| | PMI sinks 3.3pts m/m to 46.1 in June in surprise worsening |

|

| Poland | Jul 01, 12:30 |

|

- PMI comes in well below consensus of 49.8 to be worst since July 2025

Poland's manufacturing PMI fell a sharp 3.3pts m/m to 46.1 in June from 49.4 in May, to come in much worse than the consensus expectation of 49.8 and thereby hitting the worst level since July 2025 (45.9), according to a statement published Wed. by S&P Global. The index remained in negative territory for the fourteenth straight month and is now further below the 50-pt neutral mark. There was a steep drop in new orders, output fell again, purchasing and employment also fell, and stocks of unsold goods built up, though inflationary pressures also eased further. A sharp drop in new orders helped drive the overall deterioration in the PMI, with the pace of decline the fastest since June 2025 and the declining streak now at 15 months. New order issues were hit by weaker demand, an economic slowdown, difficulties gaining new customers, high customer inventory levels, and reduced client budgets, S&P said. New export orders also fell, doing so for the seventh straight month. Production fell as a result of the new order drops, but inventories of unsold stock still built up due to the scale of the order decline. Backlogs of work also declined for the fifth month running, and employment was cut for the fourteenth month in a row. The volume of inputs purchased also declined, doing so at the fastest rate since February. Still, suppliers' delivery times continued to lengthen due to geopolitical disruptions, material shortages, and logistical problems. Average input prices were said to have remained strong, though they did slow to a three-month low. Cost pressures were based on rising raw material costs (i.e., oil, metals, and chemicals) and higher energy, fuel, packaging, and transport costs. Output prices rose in June and though they remained strong, they did moderate for the second month running and hit a three-month low. The outlook index staged the biggest one-month fall since the start of the COVID-19 pandemic in March 2020, although it remained above the neutral 50.0 mark. Positive expectations were held by 23% of firms, compared with negative outlooks at 20% of them. Overall, the PMI reading brings a sharply negative surprise considering that there should be more optimism considering the Middle East conflict appears to be over and the economy can sail the wind of strong EU fund inflows to higher levels. The delayed impact of that conflict on the situation of companies and consumers in Europe might be an issue, and of course a heat spell did hit late in the month (the survey is done in the second half of the month). If one-off or weather issues were in play, then the PMI print for July should rebound, though it looks like a wave of pessimism has hit manufacturers. | PMI index | | Jun-25 | Dec-25 | Jan-26 | Feb-26 | Mar-26 | Apr-26 | May-26 | Jun-26 | | Polish PMI | 44.8 | 48.5 | 48.8 | 47.1 | 48.7 | 48.8 | 49.4 | 46.1 |

| | Source: S&P Global |

|

|

|

|

| Turkey |

|

| Car and LCV sales slide by 11.4% y/y in June |

|

| Turkey | Jul 02, 06:59 |

|

- Passenger cars and LCVs both trail last year's levels

- Market shrinks in H1 as LCV momentum turns negative

Total passenger car and LCV sales declined by 11.4% y/y to 105,041 units in June, after a much steeper 22.6% y/y fall in May, the Automotive Distributors and Mobility Association (ODMD) data showed. Passenger car sales fell by 10.4% y/y to 83,978 units, while LCV sales dropped by 15.5% y/y to 21,063 units. That said, June was still not a weak month in historical terms. Total sales stood 25.4% above the 10-year June average, with passenger cars 25.2% above and LCVs 26.4% above their respective 10-year June averages. The monthly picture therefore looked less like a fresh demand collapse and more like a market normalising from a distorted May base, we assess. The Iran war and the long Eid Al Adha holiday likely hit showroom traffic in May, while June recovered some of that lost flow. Still, the market did not return to positive annual growth. On a cumulative basis, the market contracted by 8.2% y/y to 558,179 units in H1, compared with a 7.4% y/y decline in Jan-May. Passenger car sales fell by 9.8% y/y to 440,234 units. The bigger change came from LCVs. Their cumulative performance moved from a 1.9% y/y increase in Jan-May to a 1.7% y/y contraction in H1. |

|

|

|

| World Bank and French partners provide EUR 400mn for quake rebuild |

|

| Turkey | Jul 02, 06:34 |

|

- World Bank lends EUR 250mn to rebuild resilient rural housing

- Funds to build 3,000 homes, shelter 10,470 people in quake zones

The World Bank approved a EUR 250mn additional loan to Turkey for post-earthquake recovery and reconstruction, with the financing aimed at resilient rural housing and the restoration of essential services after the Feb 2023 earthquakes, the WB said. The package came on top of EUR 150mn in co-financing from the Agence Francaise de Developpement, lifting the total new financing to EUR 400mn. The programme will fund 3,000 additional rural homes for families still living in temporary shelters, a reminder that reconstruction needs remain material more than three years after the disaster, we note. The financing was provided under the Turkey Earthquake Recovery and Reconstruction Project, which the World Bank approved in Jun 2023 to support municipal infrastructure, health services and resilient housing in affected provinces. The Global Facility for Disaster Reduction and Recovery also helped prepare the additional financing. With the latest package, the project will provide resilient rural housing for another 10,470 people in earthquake-hit areas, the WB stated. |

|

|

|

|

| Turkey | Jul 02, 06:31 |

|

Nearly 900 surprise raids are carried out in Ankara before NATO summit (Hurriyet) President Erdogan receives delegation of Catholic Bishops of Turkey (Hurriyet) AKP deputy chairman Huseyin Yayman reacts to CHP MP Ozgur Ozel's article in FT (Hurriyet) AKP reaches 11,709,913 members (Hurriyet) AKP spokesperson Omer Celik reacts to Israeli foreign minister's statement (Hurriyet) Istanbul CPI rises by 1.1% m/m in June (Sozcu) 31 out of every 100 people are unemployed (Sozcu) Highway and bridge tolls increase (Sozcu) CHP leader Kemal Kilicdaroglu faces backlash in his hometown of Tunceli (Sozcu) Transport minister Abdulkadir Uraloglu: Osmangazi Bridge is 10 years old and we save TRY 211bn in fuel and time (Sabah) Turkey's maritime trade is rising (Sabah) Striking picture ahead of NATO Summit: 57% of defence exports go to allies (Sabah) Manufacturing PMI falls to 47.1pts in June (Sabah) CBT takes new simplification step for banks: Reserve requirement for FX deposits changes (Sabah) |

|

|

|

| | CBT likely to hold, weekly repo return also stays on table |

|

| Turkey | Jul 01, 16:16 |

|

- Next MPC meeting: Jul 23, 2026

- Current policy rate: 37.0%

- EmergingMarketWatch forecast: Hold

- Rationale: Inflation eases, but sticky services, reserves and political risk keep CBT cautious

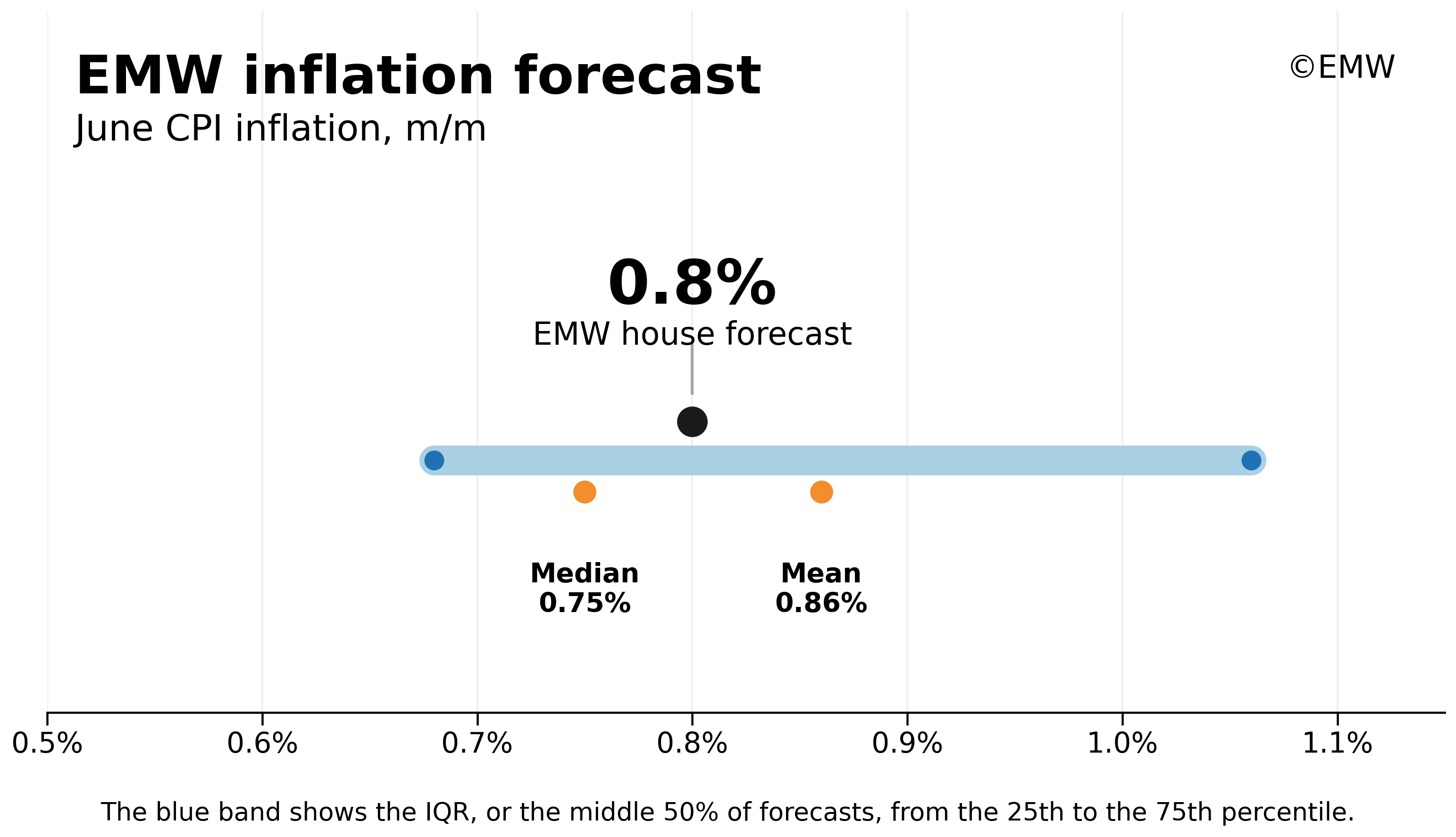

We expect the CBT to keep the policy rate unchanged at 37.0% at the forthcoming MPC meeting. Our latest inflation model set points to 0.8% m/m June CPI, with estimates clustered in a 0.7%-1.1% range. If inflation lands around these levels, annual CPI would ease modestly below 32%. This would also sit comfortably with the CBT's own communication, as it stated in its MPC summary that leading indicators pointed to a further decline in the underlying inflation trend in June. In plain terms, the CBT's message and our model signal move in the same direction, we note.

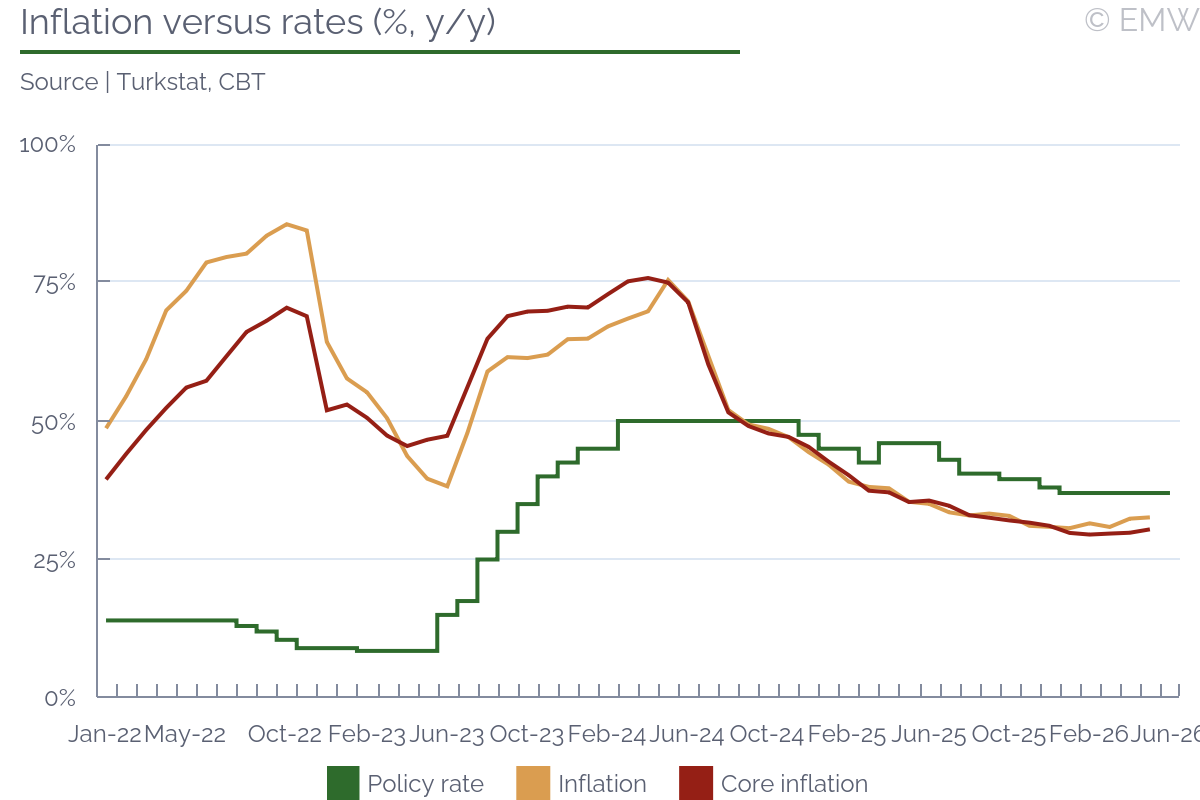

The liquidity angle still deserves attention. Since the start of the Iran war, the CBT has not relied on the one-week repo channel in any meaningful way. It has instead funded the market mainly through the overnight lending window, where the rate stands at 40.0%. Against that background, we do not rule out a return to one-week repo funding around the upcoming meeting.  The headwinds remain familiar: politics and reserves. Based on the latest available weekly figures, gross reserves fell below USD 150bn. Lower gold prices could add a further valuation drag, we note. On the domestic side, the political climate around CHP remains the main risk. Further legal or political pressure on Ozgur Ozel, and potentially Mansur Yavas, could still create market strain, in our view. For now, the available figures do not suggest a major increase in local FX demand, and that gives the CBT some room to manage the policy setting. Still, political shocks can shift expectations fast, especially when reserve credibility and disinflation confidence remain tightly connected, we note. There are also tailwinds, to be fair. The external backdrop turned more supportive for the CBT, although we would not overstate the improvement, we note. The Iran ceasefire and the subsequent fall in oil prices, if sustained, would ease pressure on inflation, the CA deficit and carry-trade sentiment. The tourism season should provide an additional reserve buffer as well, even though tourist arrivals have remained weaker than in previous years, we remind. These factors improve the near-term policy environment, but they do not give the CBT a clean opening for a softer stance yet. Overall, inflation remains sticky. Neither the CBT's 24% year-end target nor the 26% upper bound of its forecast range looks easy to reach from here. Therefore, we think the CBT is more likely to preserve a cautious tone, keep the policy rate unchanged, and avoid giving markets a strong rate-cut signal at this stage. A technical return to the one-week repo channel is possible, but it would not, on its own, change the broader policy message, we highlight. The burden of proof still sits with inflation. Until the services trend, expectations and reserve position improve more convincingly, the CBT has limited room to sound comfortable, we assess. Summary of June rate-setting meeting MPC rate decision in June Quarterly Inflation Report for Q2 Monetary policy strategy for 2026 |

|

|

|

| Argentina |

|

|

| Argentina | Jul 02, 03:54 |

|

The BCRA stepped in to stem the dollar's rise, selling bills and futures contracts to contain the currency (Infobae) Details of the BCRA charter reform Milei is preparing (La Nación) Tax revenue fell 7.4% in real terms in June due to the collapse in export taxes and the extension of the income tax deferral (Clarin) The owner of the world's largest gold fortune promised Milei a new USD 1.5bn investment (Clarin) The government is considering using the "pensioners' fund" to revive credit and the economy (Clarin) |

|

|

|

| Loan delinquency rates keep hitting new highs, BCRA not reacting yet |

|

| Argentina | Jul 01, 18:34 |

|

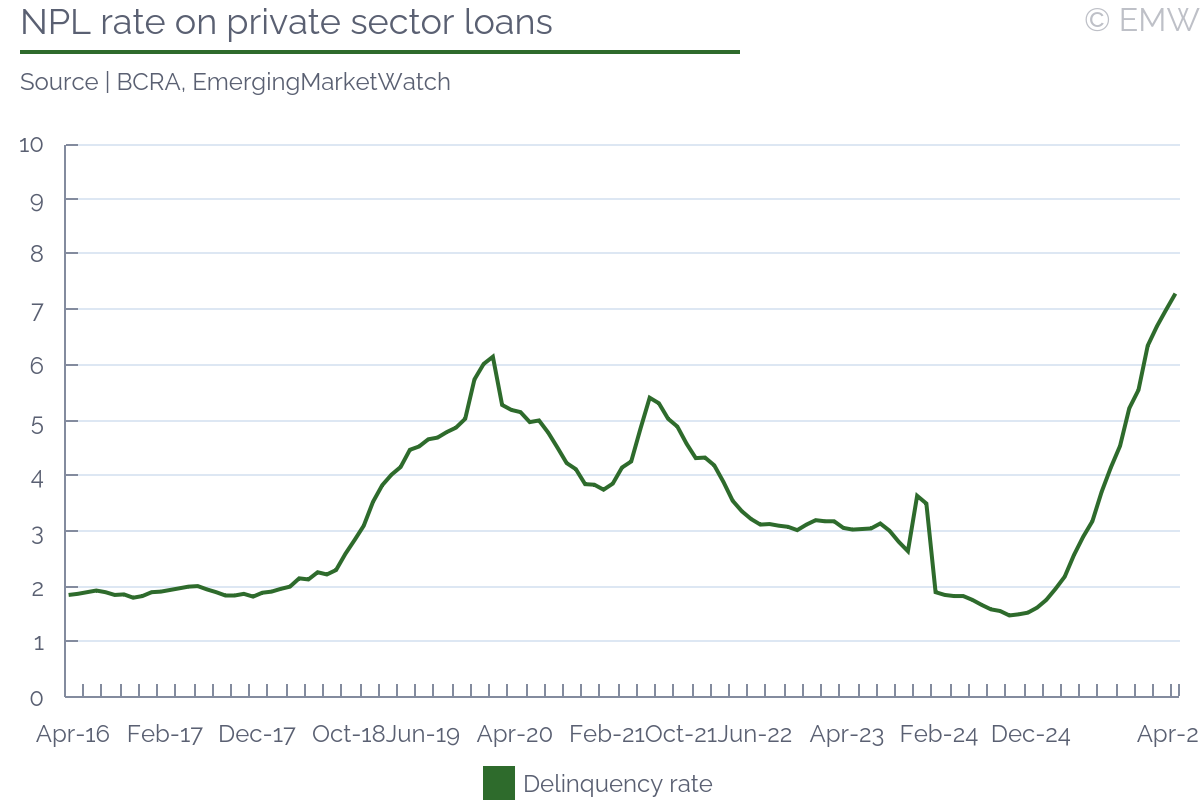

- Delinquency rate for households surges to 12.7% in bank loans, 32.2% in non-bank loans

- Corporate loan delinquency lower at 3.3%, but keeps rising and has reporting lag

- BCRA says delinquency likely peaked in Q2, sees problems tied to lenders and borrowers learning to live in low inflation

- Delinquency problems could hurt GDP forecasts as credit unlikely to remain a strong domestic demand driver

Bank loan delinquency rates for households reached 12.7% in May, climbing for the 19th month in a row, and rising fivefold since the start of the Milei administration, according to estimates by the consultancy firm 1816. Delinquency rates in financing given by non-bank financial institutions were even higher at 32.2%, and rose sharply from less than 10% at the end of 2024. Nearly 75% of the mass of non-performing loans was concentrated on people under 35 years old. The NPL rate on corporate loans was comparatively much lower at 3.3%, but has also been on the rise and there is a longer reporting lag (banks have more leeway to wait before designating a corporate loan as non-performing).  This trend of rising delinquency rates became a hot topic toward the end of 2025. At the time, the rise seemed a temporary surge tied to the tightening of monetary policy to contain currency volatility ahead of the 2025 midterm elections. The consensus was the problem would be resolved naturally as monetary policy conditions normalized, and that there wouldn't be system-wide problems because the stock of loans was small and banks were very liquid. The BCRA still seems unfazed by these developments in credit markets and has not taken any particularly strong policies to address the issues. Their view is that the increase in delinquency rates was to be expected because both lenders and borrowers were used to dealing with a rising inflation environment in which ex-post real rates were always negative, eroding loans. The current macro stabilization process shows the opposite, with declining inflation and positive real rates. In a recent presentation, BCRA Vice President Vladimir Werning said delinquency rates have likely peaked in Q2. He also argued that a new credit cycle will be starting, and that it will be a healthier and more selective cycle, with both lenders and borrowers having learned that debts don't get eroded by inflation and that credit history matters. Local consultancy firms and commentators are starting to show more concern because delinquency rates keep rising, but also because of what these issues could mean for the economy over the next year and a half. In particular, a fast-growing credit cycle was expected to play an important role in supporting economic growth and domestic demand in the run-up to the 2027 general election. | Non-performing loans %, private sector | | | | | | | Apr-23 | Apr-24 | Apr-25 | Apr-26 | | NPL | 3.1 | 1.8 | 2.2 | 7.3 | | Overdrafts | 1.6 | 1.3 | 1.8 | 6.5 | | Commercial paper / Discounted notes | 1.2 | 0.7 | 0.6 | 3.2 | | Mortgage loans | 1.7 | 1.6 | 1.4 | 2.0 | | Secured loans | 1.5 | 2.4 | 2.2 | 5.5 | | Personal loans | 4.4 | 4.3 | 4.6 | 14.8 | | Credit card balances | 2.1 | 1.7 | 2.9 | 11.2 | | Export financing | 25.5 | 1.3 | 0.4 | 0.5 | | Others | 5.1 | 3.1 | 3.2 | 12.2 |

| | Source: BCRA, EmergingMarketWatch |

|

|

|

|

| Brazil |

|

|

| Brazil | Jul 02, 03:37 |

|

Atlas/Bloomberg: Lula leads in second-round scenarios and would defeat Flávio (UOL) Caiado announces Kassab, president of the PSD, as his running mate on the presidential ticket (G1) Flávio gives a nod to Michelle and calls for unity at a meeting with women (Metrópoles) Michelle Bolsonaro considers leaving politics, sources say (CNN Brasil) Brazil reacts to the tariff hike and tells the US that the surcharge will harm Americans (Carta Capital) Treasury will lose BRL 347bn over 30 years due to state debt restructuring (Folha de São Paulo) US imposes sanctions on Brazilians and companies for alleged ties to the PCC (O Globo) Attorney General's Office argues that Bolsonaro should remain under house arrest (Veja) [Workers' Party] PT sets Aug 2 as the date for Lula's official candidacy announcement (Gazeta do Povo) |

|

|

|

| FinMin’s Freire says govt to revise 2026 inflation forecast up due to El Niño |

|

| Brazil | Jul 01, 20:05 |

|

- Freire says El Niño will push the government's 2026 inflation forecast above the current 4.5% forecast

- But he says the GDP growth forecast is likely to remain unchanged at 2.3% for 2026

Economic Policy Secretary Débora Freire said Wed. that the government will revise up its 2026 inflation forecast due to the El Niño phenomenon and its potential impact on domestic prices, according to remarks made in an interview with the daily Jota. With the expected revision, the government's inflation forecast will rise above the 4.5% given in May. Still, Freire noted that the updated forecast should remain below the 5.3% expected by analysts polled by the BCB in the Focus Report. Regarding GDP growth, Freire said the government is likely to keep its 2026 forecast unchanged at 2.3%. Overall, the government's updated macroeconomic forecasts are expected to be published later in July. Potential impacts on food prices from El Niño, which is expected to increase rainfall in southern Brazil while prolonging the dry season in the Center-West, Northeast, and North regions, also prompted the BCB to raise its 2026 inflation forecast to 5.2%, along with renewed demand-driven inflationary pressures. This scenario has increased uncertainty over the total magnitude of the BCB's ongoing "calibration" cycle, with a potential pause in the near future. Still, one thing appears certain: the Selic is likely to remain at a restrictive level for a prolonged period. |

|

|

|

| Treasury says primary surpluses will depend on additional revenue measures |

|

| Brazil | Jul 01, 20:04 |

|

- Treasury expects additional revenue efforts through 2030 in order to achieve primary surpluses

- Treasury says mandatory expenditure will grow at an average real rate of 2.7% per year between 2026 and 2036

- Govt forecasts a 0.4% of GDP primary deficit in 2026, though the lower bound of the fiscal target is expected to be met through exclusions from the fiscal framework

- Govt forecasts gross public debt to peak at 87.9% of GDP in 2029, pressured by interest payments

The National Treasury said that meeting the government's primary surplus targets in the coming years will depend on additional revenue-raising efforts, according to the Fiscal Projections Report. The Treasury forecasts that net revenue will follow an upward trend over the coming years, rising from 18.9% of GDP in 2026 to a peak of 19.6% in 2030 before declining to 18.0% of GDP by 2036. It estimates that additional revenue averaging 1.2% of GDP per year will be required between 2028 and 2036, ranging from 0.2% of GDP in 2027 (around BRL 30bn) to a peak of 1.9% of GDP in 2032 (around BRL 300bn). This scenario assumes total expenditure will fall below 19.0% of GDP from 2027 onward due to the expenditure caps established by the fiscal framework, and it considers no budget freeze. In our view, it is highly unrealistic to expect the government to sustain such a pace of revenue increases over the coming years. The primary surplus targets also become progressively more ambitious, reaching 1.0% of GDP in 2028, 1.25% in 2029, and 1.5% in 2030, although these targets could still be revised (and are likely to be, in our view). The forecasts assume average real GDP growth of 2.8% per year between 2026 and 2036, with inflation returning to the 3.0% target by 2028. The government also projects a gradual decline in the Selic rate over the coming years, and the benchmark rate is to reach some 6.5% by 2036. The Treasury also said that mandatory expenditure is projected to grow at an average real rate of 2.7% per year between 2026 and 2036, driven by social security spending, the BPC welfare program, unemployment insurance, and expenditures linked to the constitutional minimum spending requirements for health and education. This growth exceeds the 2.5% ceiling established by the fiscal framework for total expenditure growth, thereby squeezing discretionary spending. To comply with the fiscal framework, the Treasury estimates that discretionary expenditure will need to decline by an average real rate of 3.2% per year. The forecasts reinforce the need for a spending review and measures to reduce budget rigidities. The Treasury likewise estimates that the government will post a primary deficit of 0.4% of GDP in 2026, which is worse than the 0.2% deficit forecast in January. Nevertheless, the primary fiscal target of a 0.25% of GDP surplus is expected to be met in the sense the deficit will come in at the lower tolerance band (-0.25% of GDP, effectively allowing for a zero primary balance) due to exclusions from the fiscal framework, including defense spending, court-ordered judicial payments (precatórios), temporary health and education expenditures, and reimbursements to retirees affected by the recent social security fraud scheme. Regarding gross public debt, the Treasury forecasts it will rise to 83.5% of GDP in 2026 and peak at 87.9% in 2029 before declining to 83.1% by 2036. Overall, the Treasury report reinforces the urgent need for a mandatory spending review and a reduction of Brazil's budget rigidities. At the same time, it suggests that, if reelected, President Lula da Silva's fiscal strategy would likely continue to rely primarily on raising revenues, with this possibly increasing fiscal uncertainty at a time when the fiscal framework approved in 2023 has not succeeded in placing public debt on a sustainable path. In our view, this reliance on higher revenues creates the need for additional fiscal stimulus to sustain economic growth -- which is crucial for achieving revenue records -- while simultaneously reinforcing the need for higher interest rates to contain inflation and increasing pressure on public debt. Although Lula's revenue measures have contributed to greater social equity, such as the income tax exemption and higher taxation on high-income individuals, the limited focus on expenditure reforms is likely to become increasingly unsustainable during a second term if he is reelected. In our view, the period immediately following the elections and the beginning of the next presidential term will represent a key window for more structural spending reforms, particularly regarding the indexation of pension benefits to the minimum wage and the constitutional minimum spending requirements for health and education, which are currently linked to net revenue. Although we believe reforms to mandatory spending will be unavoidable under the next administration regardless of who wins the election, it remains uncertain whether Lula would be willing to spend political capital on measures that could alienate his electoral base. Moreover, even if he decides to address spending, it remains unclear how far he would be willing to go, raising the risk that only incremental adjustments would be adopted, merely postponing the fiscal problem. Flávio Bolsonaro, in turn, is expected to pursue a more assertive fiscal adjustment agenda, with members of his economic team suggesting that mandatory spending should be indexed only to inflation. However, two important risks should be highlighted. First, it remains uncertain whether Flávio would use his political capital during the post-election honeymoon period to advance fiscal reforms, particularly given that his initial political priority could be securing an amnesty for his father, ex-President Jair Bolsonaro, in regards to the attempted coup conviction. Second, the composition of Congress is likely to remain dominated by centrist parties, which have limited incentives to reduce social spending, and that could make it difficult to obtain the three-fifths majority required to amend the constitution to implement fiscal reform. | Fiscal forecasts (% of GDP) | | 2026 | 2027 | 2028 | 2029 | 2030 | 2031 | 2032 | 2033 | 2034 | 2035 | 2036 | | Public setor primary result | -0.4 | 0.0 | 0.6 | 0.9 | 1.2 | 1.3 | 1.4 | 1.4 | 1.4 | 1.4 | 1.5 | | Central govt primary result | -0.4 | 0.0 | 0.6 | 0.9 | 1.3 | 1.3 | 1.4 | 1.4 | 1.4 | 1.5 | 1.5 | | Net revenue | 18.9 | 19.0 | 19.4 | 19.4 | 19.6 | 19.6 | 19.6 | 19.1 | 18.7 | 18.3 | 18.0 | | Total expenditures | 19.4 | 18.9 | 18.7 | 18.5 | 18.4 | 18.3 | 18.2 | 17.6 | 17.2 | 16.8 | 16.5 | | Regional governments | 0.2 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | | Public companies | -0.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | | Nominal interest | 8.6 | 8.0 | 7.3 | 6.9 | 6.5 | 6.0 | 5.9 | 5.8 | 5.6 | 5.6 | 5.6 | | Nominal deficit | -9.0 | -8.0 | -6.7 | -6.0 | -5.2 | -4.7 | -4.5 | -4.4 | -4.2 | -4.1 | -4.1 | | Gross debt | 83.5 | 85.9 | 87.3 | 87.9 | 87.4 | 86.9 | 86.2 | 85.5 | 84.7 | 83.9 | 83.1 |

| | Source: Treasury |

Click here for our comprehensive database of macro forecasts. |

|

|

|

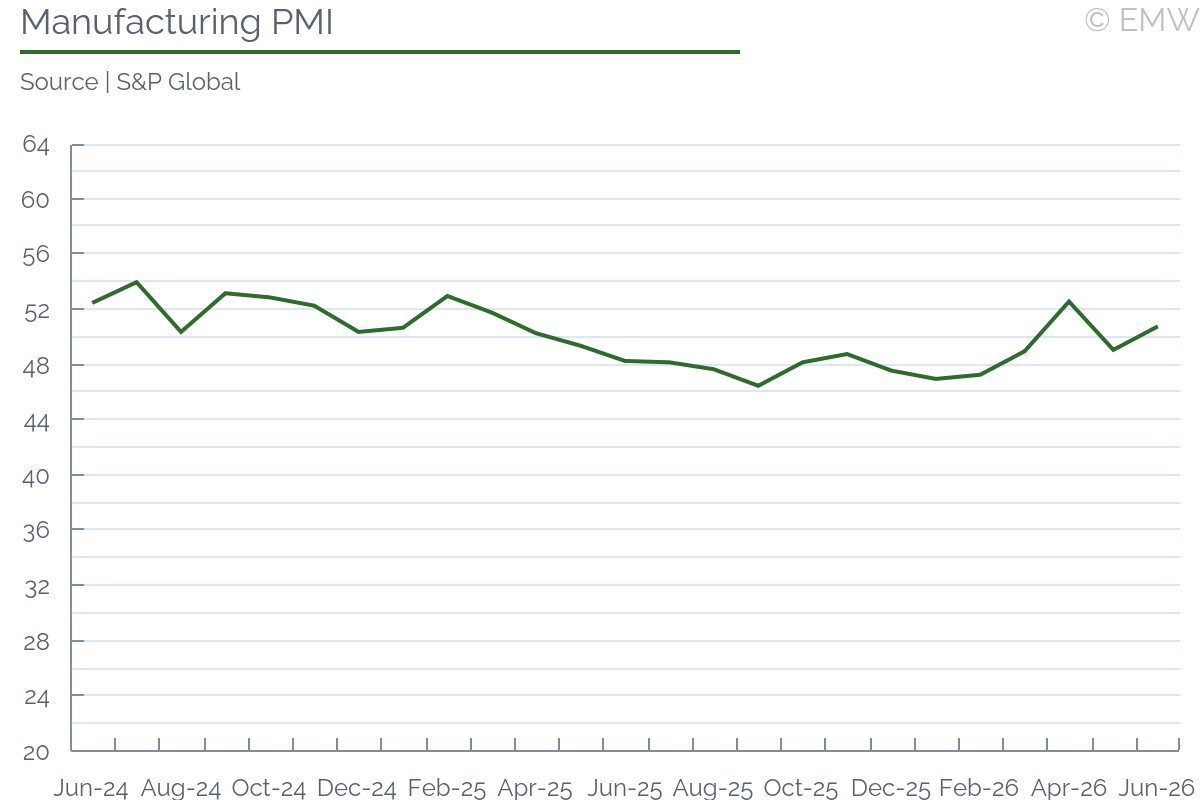

| Manufacturing PMI rises 1.7pts m/m to 50.8pts in June |

|

| Brazil | Jul 01, 15:40 |

|

- PMI returns in June to a level topping the neutral mark after holding below at 49.1pts in May

- Increase is driven mainly by employment and inventory accumulation, while output remains in contraction territory

The S&P Global Brazil Manufacturing PMI rose 1.7pts m/m to 50.8pts in June from 49.1pts in May, taking the indicator back above the 50-pt neutral mark, according to data released Wed. by S&P Global. S&P said the increase was mainly driven by rising employment, which increased for the fifth consecutive month, and inventory accumulation, while output remained in contraction territory in June. Longer supplier delivery times also supported the increase as this usually signals strong demand, but in this case it reflected supply chain disruptions stemming from the Middle East conflict, S&P said. International orders also declined in June. Expectations for the next 12 months remained positive but fell to their lowest level in 14 months amid concerns about competition, demand trends, political uncertainty, and global instability, S&P said.  Companies reported lower input cost inflation in June but continued to point to higher fuel, material, and transportation costs stemming from the Middle East conflict. Selling prices also increased in June, though at their slowest pace in three months. Overall, the improvement in the manufacturing PMI in June was driven by employment and inventory accumulation rather than stronger output, while inflationary pressures eased following the US-Iran agreement. In our view, the result supports the BCB's expectation of an economic slowdown, although the deceleration could be occurring more gradually than anticipated due to a robust labor market and ongoing fiscal and credit stimulus. With renewed demand-driven inflationary pressure, the Copom is likely to keep the Selic rate at a restrictive level for a prolonged period, continuing to weigh on manufacturing activity. | Manufacturing PMI (pts) | | Jun-25 | Mar-26 | Apr-26 | May-26 | Jun-26 | | Manufacturing PMI | 48.3 | 49.0 | 52.6 | 49.1 | 50.8 |

| | Source: S&P Global |

|

|

|

|

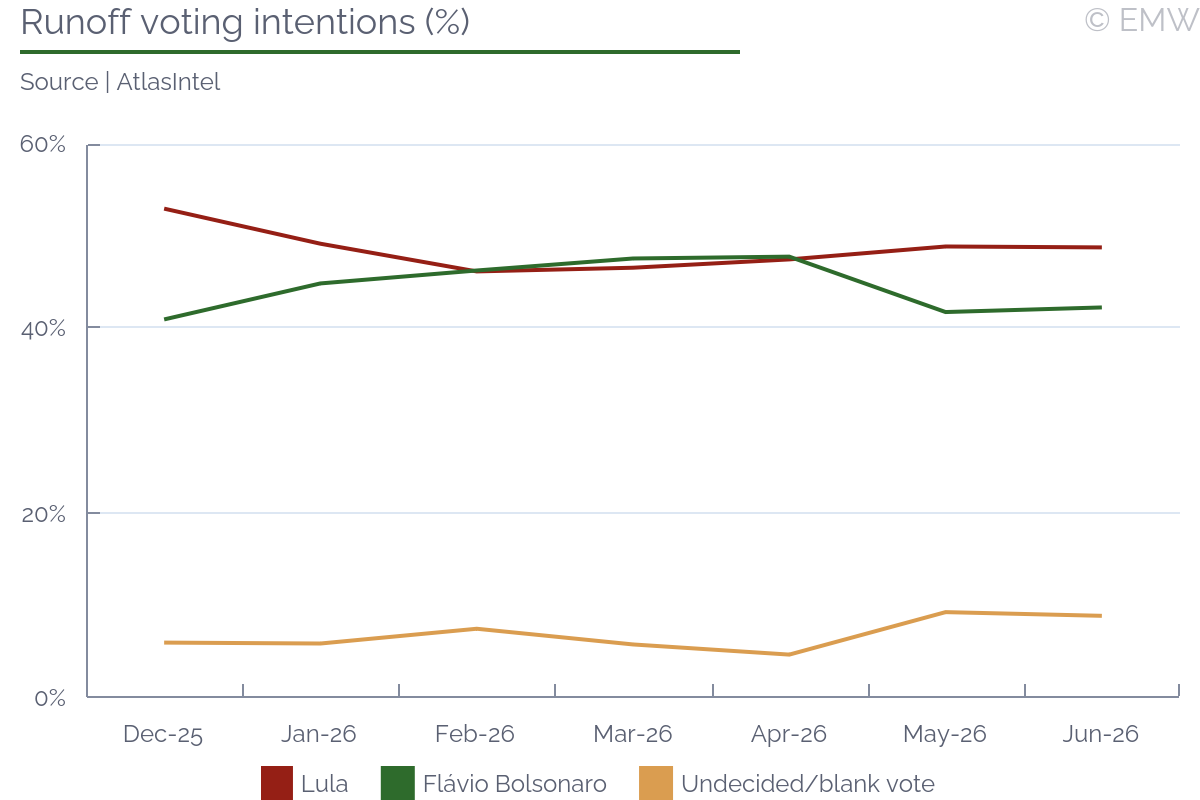

| Lula holds 6.5-pp lead over Flávio Bolsonaro in runoff – Atlas |

|

| Brazil | Jul 01, 14:56 |

|

- Lula consolidates his lead over Flávio as Banco Master scandal continues to hit latter's campaign

- Missão's Renan Santos rises to third place in first round, limiting potential gains by Caiado and Zema from a weakened Flávio Bolsonaro candidacy

- Atlas does not assess voters' reactions to the feud between Michelle and Flávio Bolsonaro or the involvement of Lula ally Jaques Wagner in the Banco Master case

- Lula remains the frontrunner for Oct election, but the Banco Master investigation continues to hover over the electoral landscape

President Lula da Silva had a 6.5-pp over Flávio Bolsonaro in a potential presidential election runoff, leading by 48.8% to 42.3%, according to a Jun 26-30 poll released Wed. by Atlas. The lead is slightly narrower than the 7.1-pp advantage Lula held in the May poll, which was the first to reflect the impact of the scandal involving Flávio's relationship with former Banco Master owner Daniel Vorcaro. Lula maintained his lead despite a decline in his approval rating, which fell to 45.9% in June from 47.0% in May. His disapproval rating also declined, to 52.3% from 53.0%, while the share of respondents who did not know or did not answer rose to 1.8% from 1.0%. We note that the May poll was taken offline after the Electoral Court accepted a request from the Liberal Party alleging voter inducement.  Lula remains the clear frontrunner in the first-round scenario, holding a 9.7-pp lead over Flávio Bolsonaro, reflecting the impact on Flávio's campaign of the Banco Master scandal and the recent feud with his stepmother, Michelle Bolsonaro. The main surprise in the first-round poll was the rise of Renan Santos from the Missão Party. Santos's voting intentions rose to 7.8% in June from 6.9% the month before as he enjoys strong support among younger voters and those who reject both Flávio and Lula. Although we do not expect Santos to become a significant challenger to either Lula or Flávio, he appears to be attracting voters disappointed with Flávio because of his relationship with Vorcaro. Moreover, Santos's candidacy seems to be preventing the two other main right-wing candidates, Romeu Zema and Ronaldo Caiado, from benefiting from Flávio's weakened position, which is likely to help preserve Flávio's status as the main opposition candidate through the end of the campaign. Regarding rejection rates, Flávio's rose to 53.0% from 52.0% while Lula's fell to 48.6% from 50.6%. Atlas did not include many questions regarding the latest political developments, particularly the dispute between Flávio and Michelle Bolsonaro and the involvement of Lula's former Senate leader, Jaques Wagner, in the Banco Master case. This was likely related to the Electoral Court's decision to remove the previous poll over allegations of voter inducement. The Liberal Party argued that the order of questions regarding the Banco Master scandal encouraged respondents to form a negative view of Flávio, though Atlas has denied this. The ruling was widely criticized by local media because it was issued unilaterally by Justice Kassio Nunes, who was appointed by former President Jair Bolsonaro. Overall, the poll consolidates Lula's lead over Flávio Bolsonaro following the Banco Master scandal and the threat of new US tariffs, which Lula has associated with Flávio. Although Atlas did not ask respondents about the involvement of Lula's former Senate ally in the Banco Master investigation, it appears to have had little impact on Lula's support. Still, any potential effect may have been overshadowed by the public feud between Michelle and Flávio Bolsonaro, which dominated headlines and further weakened Flávio's campaign. With fewer than 100 days until the first round of the October elections, Lula appears to have regained the advantage he held in late 2025, while Flávio now faces the challenge of recovering support lost because of his ties to Vorcaro. That task may have become even more difficult after his confrontation with Michelle, which could hinder his efforts to gain support among women and evangelical voters, with the latter being a crucial constituency. Still, we continue to expect Flávio to remain Lula's main challenger. At the same time, the ongoing Banco Master investigation continues to hover over the election and could still reshape the presidential race. | Voting intentions in first-round | | Quaest | Datafolha | Atlas | | Candidate | May | June | May-13 | May-22 | June | May | June | | Lula | 39.0% | 39.0% | 38.0% | 40.0% | 41.0% | 47.0% | 46.3% | | Flávio Bolsonaro | 33.0% | 29.0% | 35.0% | 31.0% | 31.0% | 34.3% | 36.6% | | Ronaldo Caiado | 4.0% | 3.0% | 3.0% | 4.0% | 3.0% | 2.7% | 2.9% | | Romeu Zema | 4.0% | 2.0% | 3.0% | 3.0% | 2.0% | 5.2% | 2.0% | | Renan Santos | 2.0% | 3.0% | 2.0% | 3.0% | 3.0% | 6.9% | 7.8% | | Others | 3.0% | 5.0% | 7.0% | 7.0% | 9.0% | 0.6% | 3.2% | | Undecided | 5.0% | 10.0% | 3.0% | 3.0% | 4.0% | 1.9% | 0.1% | | Blank/null | 10.0% | 9.0% | 9.0% | 9.0% | 7.0% | 1.4% | 1.1% |

| | Source: Pollsters, EmergingMarketWatch |

| Rejection of Political Leaders | | Atlas | Datafolha | Quaest | | May | June | May-13 | May-22 | June | May | June | | Lula da Silva | 50.6% | 48.6% | 47.0% | 45.0% | 46.0% | 53.0% | 53.0% | | Flávio Bolsonaro | 52.0% | 53.0% | 43.0% | 46.0% | 48.0% | 54.0% | 56.0% | | Michelle Bolsonaro | 45.6% | 43.2% | Not polled | 31.0% | Not polled | Not polled | Not polled | | Ronaldo Caiado | 38.0% | 38.6% | 13.0% | 15.0% | 14.0% | 32.0% | 32.0% | | Romeu Zema | 42.2% | 38.5% | 15.0% | 18.0% | 17.0% | 27.0% | 29.0% | | Jair Bolsonaro | 49.1% | 45.2% | Not polled | Not polled | Not polled | Not polled | Not polled | | Renan Santos | | 35.8% | | | 12.0% | | 20.0% |

| | Source: EmergingMarketWatch, pollsters |

|

|

|

|

| | BCB sees inflation above target band through 2026, weighing on cycle |

|

| Brazil | Jul 01, 14:34 |

|

- Copom meeting: Aug 4-5, 2026

- Current policy rate: 14.25%

- EmergingMarketWatch forecast: Hold

The BCB raised its inflation forecast for 2026 to 5.20% in its June Monetary Policy Report, up from 3.90% in March, reflecting recent inflationary pressures, a larger positive output gap, higher fuel and commodity prices due to the Middle East conflict, and higher inflation expectations. Although the BCB noted that the tight monetary policy in place has partially offset this upward pressure, it forecasts inflation to remain above the 4.50% upper limit of the +/- 1.50-pp fluctuation band around the 3.0% target through end-2026, thus remaining above the target limit for more than six months and requiring the BCB to send an explanatory letter to the finance minister in October. Amid renewed inflationary pressures and a worsening inflation outlook, the Copom's next decision remains unclear and could be either a pause or an additional 25-bp cut before then pausing. BCB Governor Gabriel Galípolo has said of late that providing forward guidance amid elevated uncertainties could do more harm than good. He acknowledged that the Copom's latest post-meeting statement generated noise, which he attributed to over-explanation rather than a lack of it. The comment referred to a paragraph in the post-meeting statement in which the Copom used a longer horizon to explain its decision to cut the Selic at the meeting by 25bps to 14.25%. BCB Director of International Affairs and Corporate Risk Management Paulo Picchetti also clarified that the committee did not actually extend the relevant policy horizon, but merely referred to a longer horizon to explain the June decision under a very specific set of circumstances. Picchetti added that the BCB does not intend to change the relevant policy horizon. Uncertainty about the Copom's next decision stems mainly from two remarks made in its latest communication. The BCB said that the tight monetary policy implemented in 2025, which has contributed to the Copom cutting the Selic rate for three consecutive meetings, allows different interest-rate paths to be consistent with inflation converging toward the target, although uncertainty regarding model parameters remains elevated due to geopolitical developments. The committee also said that bringing inflation back to the 3.0% target by Q4 2027 would require abrupt changes in the Selic rate, likely resulting in inflation remaining below target for several quarters afterward. However, it noted that alternative scenarios involving temporary pauses followed by additional rate cuts would reduce output volatility while still bringing inflation back to the target by Q1 2028. As the committee mentioned alternative scenarios involving temporary pauses followed by additional cuts, we remain split between whether the Copom will pause at the next policy sitting on Aug 4-5 or will cut by an additional 25bps to 14.00% at the sitting before pausing. Yet, as the government continues to implement demand-supporting measures, which have tilted the inflation risk balance to the upside, and the labor market remains robust with real wage gains, we believe the most likely scenario is a hold in August, though another cut cannot be ruled out. Overall, the Copom's next decision remains unclear amid elevated domestic and external uncertainties stemming from the government's fiscal policy ahead of the October elections, the effectiveness of the US-Iran peace agreement, and US trade policy toward Brazil. Although the restrictive monetary stance adopted by the BCB in 2025 has allowed the Copom to begin cutting the Selic rate this year, the pace and magnitude of the ongoing "calibration" cycle continue to be shaped by these uncertainties. Still, amid mounting demand-driven inflationary pressures supported by a robust labor market and additional fiscal and credit stimulus, we believe the Copom is slightly more likely to hold the Selic at its August policy meeting. An additional 25-bp cut before pausing the cycle, however, cannot be fully ruled out, and incoming inflation and activity data should provide further clues as to the committee's next move. | Copom structure and latest voting results | | Board member | Overall bias | Position | Latest vote | Latest comments | | Gabriel Muricca Galipolo | Dovish | Governor | Cut | 25-Jun | | Rodrigo Alves Teixeira | Dovish | Director of Administration | Cut | | | Izabela Correa | Dovish | Director of Institutional Relations and Citizenship | Cut | | | Gilneu Astolfi Vivan | Dovish | Director of Regulation | Cut | | | Ailton De Aquino Santos | Dovish | Director of Inspection | Cut | undefined | | Nilton David | Dovish | Director of Monetary Policy | Cut | 28-May | | Paulo Picchetti | Dovish | Director of International Affairs and Corporate Risk Management | Cut | 25-Jun | | Vacant | - | Director of Financial System and Resolution | - | | | Vacant | - | Director of Economic Policy | - | |

| | Source: BCB |

|

|

|

|

| Lending growth slows to 9.5% y/y in May |

|

| Brazil | Jul 01, 13:25 |

|

- Lending slows from revised 9.6% y/y in Apr

- Lending rises 0.6% m/m in May, driven by public credit

Total lending by the financial sector rose 9.5% y/y in May to BRL 7.3tn, slowing from a revised 9.6% increase the month before, according to data released Wed. by the BCB. This marks the 99th consecutive yearly increase. On a monthly basis, lending rose 0.6% m/m in May, accelerating from a revised 0.3% the month before, driven by public lending. In real terms, lending grew 4.3% y/y in May, slowing from a revised 4.9% in April. Public-sector lending grew 8.9% y/y in May, accelerating from 8.3% in April as lending to the federal government quickened from the month before. On a monthly basis, public lending grew 1.0% m/m in May, easing from a revised 1.8% increase the month before. Private lending rose 9.5% y/y in May, slowing slightly from a revised 9.6% the month before and supported mainly by household lending once again. In monthly terms, private lending grew 0.5% m/m, also accelerating from 0.2% in April. The BCB also reported that the average loan interest rate fell 0.1pp m/m but rose 1.7pps y/y to 33.4% in May. The default rate on the total credit portfolio for loans overdue by more than 90 days reached 4.7%, rising 0.1pp and 1.0pp y/y. In household lending, the default rate rose 0.1pp m/m and 1.2pps y/y to 5.6%. In April, the BCB noted that household debt held at 49.8%, remaining unchanged from the month before while rising 0.9pp y/y. The income-commitment ratio fell to 28.2% from 29.3% the month before. Overall, lending in Brazil continues to expand, albeit at a slower pace than it did in 2025, reflecting the tight monetary policy. Still, the lending market remains resilient despite an average real interest rate of around 10%, likely supported by a strong labor market and directed credit measures implemented by the government. The government recently launched the Desenrola 2.0 debt-relief program to help households reduce their debt burden, which may partly explain the decline in the income-commitment ratio. It also introduced an additional program targeting borrowers who remain current on their debt payments, aiming to reduce borrowing costs for this group. These initiatives are part of the government's efforts to improve households' perceptions of the economy, which President Lula da Silva argues has been hurt by elevated indebtedness. We remain skeptical about the extent to which these programs can effectively support Lula's reelection bid as the first Desenrola program had only a limited impact on his approval. From a monetary policy perspective, however, these measures could require interest rates to remain restrictive for longer by increasing disposable income and adding to demand-driven inflationary pressure. | Financial sector lending (BRL mn) | | May-25 | Mar-26 | Apr-26 | May-26 | | Domestic Credit | 6,666,287 | 7,239,523 | 7,258,599 | 7,299,615 | | Private | 6,394,304 | 6,951,512 | 6,965,356 | 7,003,447 | | Corporates | 2,260,725 | 2,398,838 | 2,391,380 | 2,408,382 | | Individuals | 4,133,579 | 4,552,674 | 4,573,976 | 4,595,065 | | Public | 271,983 | 288,011 | 293,243 | 296,168 | | Federal government | 53,388 | 57,409 | 55,002 | 57,742 | | States and municipalities | 218,594 | 230,602 | 238,241 | 238,426 |

| | Source: BCB |

|

|

|

|

| Mexico |

|

|

| Mexico | Jul 02, 05:57 |

|

Ebrard says the USMCA remains in force until 2036 (La Jornada) Ebrard says uncertainty will decline when the USMCA revision mechanism is clarified on July 20 (El Economista) Federal govt injects more than MXN 100bn into PEMEX in H1 2026 (El Financiero) The Treasury will stop collecting MXN 3.4tn in 2026-2027 because of fiscal exemptions and stimuli (Expansión) Elections Institute grants PAZ and We are Mexico registrations as political parties (Milenio) Carlos Slim says Mexico's oil production can grow with private investment (El Financiero) |

|

|

|

|

| Mexico | Jul 02, 03:33 |

|