|

|

| Middle East and Africa Morning Review | Jul 2, 2026 |

|

This e-mail is intended for Sample Report only. Note that systematic forwarding breaches subscription licence compliance obligations. Open in browser | Edit Countries on Top

We have launched coverage of Bangladesh |

|

| Large EMs |

|

| Egypt |

|

|

|

|

|

| Nigeria |

|

|

|

|

|

|

|

|

|

| Middle East & N. Africa |

|

| Israel |

|

|

|

|

|

|

|

|

|

| Jordan |

|

|

| MENA |

|

|

| Morocco |

|

|

| Qatar |

|

|

| Saudi Arabia |

|

|

| Tunisia |

|

|

|

|

| Sub-Saharan Africa |

|

| Angola |

|

|

| Ethiopia |

|

|

|

|

| Gabon |

|

|

|

| Ghana |

|

|

|

|

| Ivory Coast |

|

|

|

| Kenya |

|

|

|

|

|

|

|

| Mozambique |

|

|

|

|

| Senegal |

|

|

|

|

|

|

|

| South Africa |

|

|

|

|

|

|

| Uganda |

|

|

|

| Zambia |

|

|

|

|

|

|

| Egypt |

|

| Local markets are closed on 02 Jul 2026 due to a public holiday. |

|

| Egypt | Jul 02, 12:01 |

|

EmergingMarketWatch coverage of Egypt will be limited on 02 Jul 2026 due to a public holiday. |

|

|

|

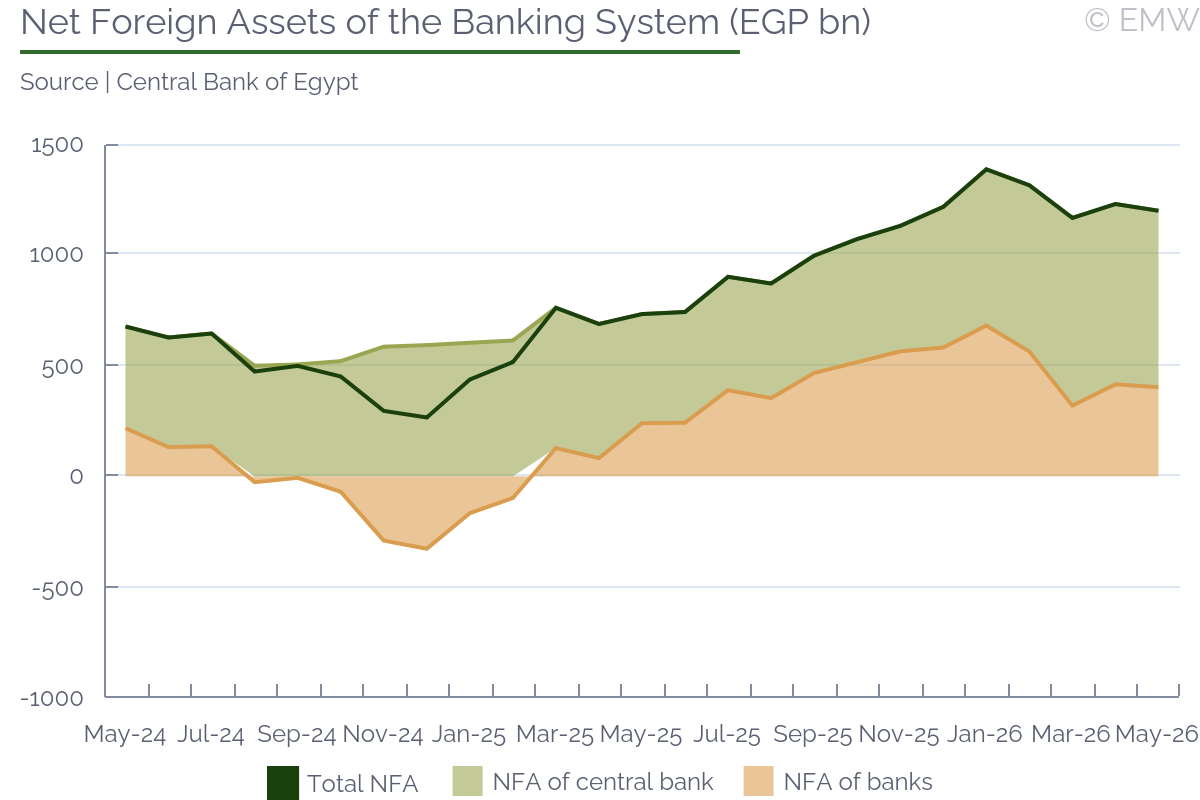

| Banking system’s NFAs hold steady m/m at USD 22.9bn as of end-May |

|

| Egypt | Jul 02, 11:45 |

|

- Foreign assets of commercial banks rise m/m, which we attribute to portfolio inflows

- EGX recorded total capital outflow of USD 3.7bn in Feb-Mar, net inflow of USD 2.9bn in Apr-May

- Net portfolio inflows surge in June attracted by high yields, easing regional uncertainty

The Net Foreign Assets (NFA) of the banking system (banks + CBE) fell by EGP 30bn or 2.5% m/m to EGP 1,199bn as of end-May, following a 5.4% m/m increase in the preceding month, according to data released by the central bank. However, if we take into account the 2.6% m/m appreciation of the pound, the value of NFAs stood unchanged at USD 22.9bn. The foreign assets of commercial banks rose by 2.1% m/m to USD 43.6bn, which we attribute to net portfolio flows and strong remittances recorded in May. Foreign investors were indeed net buyers of debt instruments through the local bourse, acquiring net USD 0.6bn worth of T-bills/bonds in May following a USD 2.3bn net inflow in April. Overall, the local bourse recorded a net inflow of USD 2.9bn in Apr-May against a net outflow of USD 3.7bn in Feb-Mar, but net portfolio inflows surged to USD 8.9bn in June. This is the second highest inflow on record, so we expect a sharp increase in banks' NFAs next month. Meanwhile, CBE's foreign assets kept falling in May, which most likely reflects external public debt service and settlement of energy arrears by the government.  We remind that the system-wide NFAs stood at a USD 22bn net liability as of end-February 2024 and their strong improvement since then was due to USD 35bn UAE deal and a surge of portfolio inflows that followed the pound's float and the securing of massive external financing. While this massive inflow of hot money has raised the risks related to capital outflows and rollover risks, Egypt has largely emerged unscathed from the sell-offs that marked 2025 thanks to recent reforms and relatively large external reserves. Not surprisingly, the Iran war triggered capital outflows, but EGX figures and FX reserve data suggest that the capital outflows were orderly and relatively muted during March, before reversing to capital inflows in April, eventually soaring in June. | Foreign Assets of Banking System (EGP bn) | | Mar-26 | Apr-26 | May-26 | | Foreign Assets With | 4,923 | 5,049 | 4,989 | | Central Bank of Egypt | 2,768 | 2,762 | 2,711 | | Banks | 2,155 | 2,287 | 2,278 | | Foreign Liabilities With | 3,757 | 3,820 | 3,790 | | Central Bank of Egypt | 1,921 | 1,948 | 1,915 | | Banks | 1,836 | 1,872 | 1,876 | | Net Foreign Assets | 1,166 | 1,229 | 1,199 | | Net Foreign Assets (USD bn) | 21.4 | 22.9 | 22.9 |

| | Source: Central Bank of Egypt |

|

|

|

|

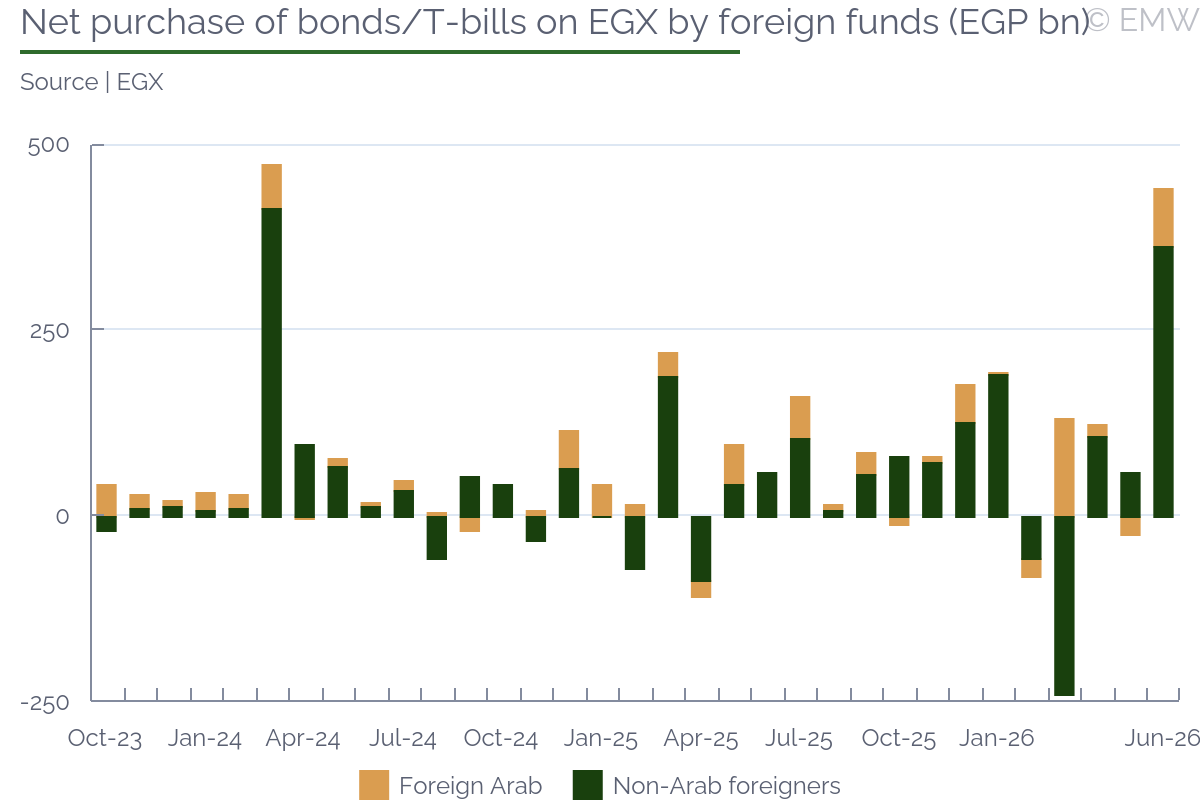

| | Foreign funds buy USD 8.9bn worth of bonds/T-bills on EGX in June (net) |

|

| Egypt | Jul 02, 11:10 |

|

- Both non-Arab and Arab funds stepped up purchases attracted by high yields, easing regional insecurity

- Foreign investors held USD 54bn worth of T-bills as of end-January, but this includes USD 25bn pledged as collateral

- Pound depreciated sharply in March, but has regained most of its losses since then on portfolio, remittance inflows

Foreign institutional investors bought record-high EGP 800bn worth of T-bills and bonds through the local exchange (EGX) in June and sold EGP 362bn worth of the debt instruments, recording a net acquisition of EGP 438bn (USD 8.9bn), according to data from the local bourse. This is the second strongest net flow on record and marks the third consecutive month of net purchases by foreign investors reflecting high yields and easing geopolitical uncertainty. For comparison, foreign funds sold a total of USD 3.7bn worth of T-bills/bonds in February and March after the war in Iran triggered capital outflows across the region. The non-Arab institutional investors, who we believe are more sensitive to global and regional volatility, recorded a net inflow of USD 7.4bn in June, the second largest in the series history. Foreign Arabs were net buyers as well, with USD 1.6bn. Following the strong recent portfolio and remittance inflows, the pound regained most of its strength and currently trades at USD/EGP 49.2 or 3% below its pre-war value.  It should be noted that the EGX does not provide a breakdown by type of instruments - bonds vs T-bills - but we believe that foreign demand is geared heavily towards the short-term notes. Foreign investors held USD 54bn worth of T-bills as of end-January, accounting for 43% of the outstanding stock and for 101% of CBE's official FX reserves. However, the CBE said that these foreign holdings include T-bills pledged by local banks as collaterals worth USD 25bn, so the actual foreign holdings should be around USD 28bn. | Trading of T-bills/bonds by institutional investors on EGX (EGP bn) | | Mar-26 | Apr-26 | May-26 | Jun-26 | | Buy | 2,420 | 2,000 | 1,382 | 2,415 | | Egyptians | 1,746 | 1,439 | 1,054 | 1,616 | | Arabs | 275 | 132 | 60 | 218 | | Foreign non-Arab | 398 | 429 | 268 | 581 | | | Sell | 2,425 | 2,009 | 1,387 | 2,425 | | Egyptians | 1,641 | 1,571 | 1,090 | 2,063 | | Arabs | 146 | 116 | 86 | 142 | | Foreign non-Arab | 638 | 322 | 211 | 219 |

| | Source: EGX |

|

|

|

|

|

| Egypt | Jul 02, 07:59 |

|

Egypt to reinstate quarterly fuel price review mechanism in Q1 of FY26/27: PM Madbouly (Ahram Online) El-Sisi calls for localizing marine vessel manufacturing to support exports (Egypt Today) El-Sisi approves USD 300mn AIIB loan to support resilience programme (Egypt Today) Egypt moves 3 petroleum firms toward stock market offerings (Egypt Today) EU backs Egypt's renewable energy push with EUR 90mn grid upgrade grant (Egypt Today) Egypt and Switzerland sign USD 1.7mn grant for e-waste recycling project (Daily News Egypt) |

|

|

|

| Nigeria |

|

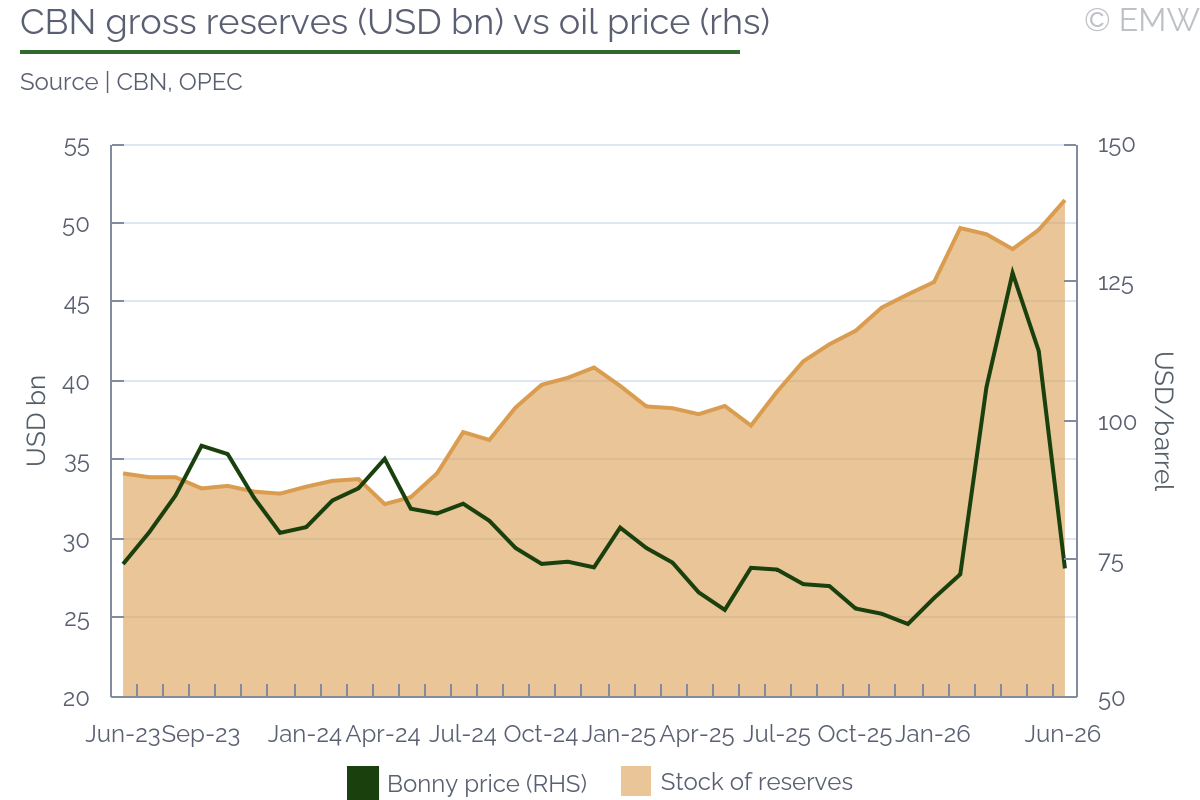

| CBN forex reserves rise 3.8% m/m to USD 51.5bn as of end-June |

|

| Nigeria | Jul 02, 12:57 |

|

- Reserves are up by net USD 6bn since Dec 2025

- Reserves already passed CBN's year-end target of USD 51bn

- Naira depreciated slightly despite stronger reserves

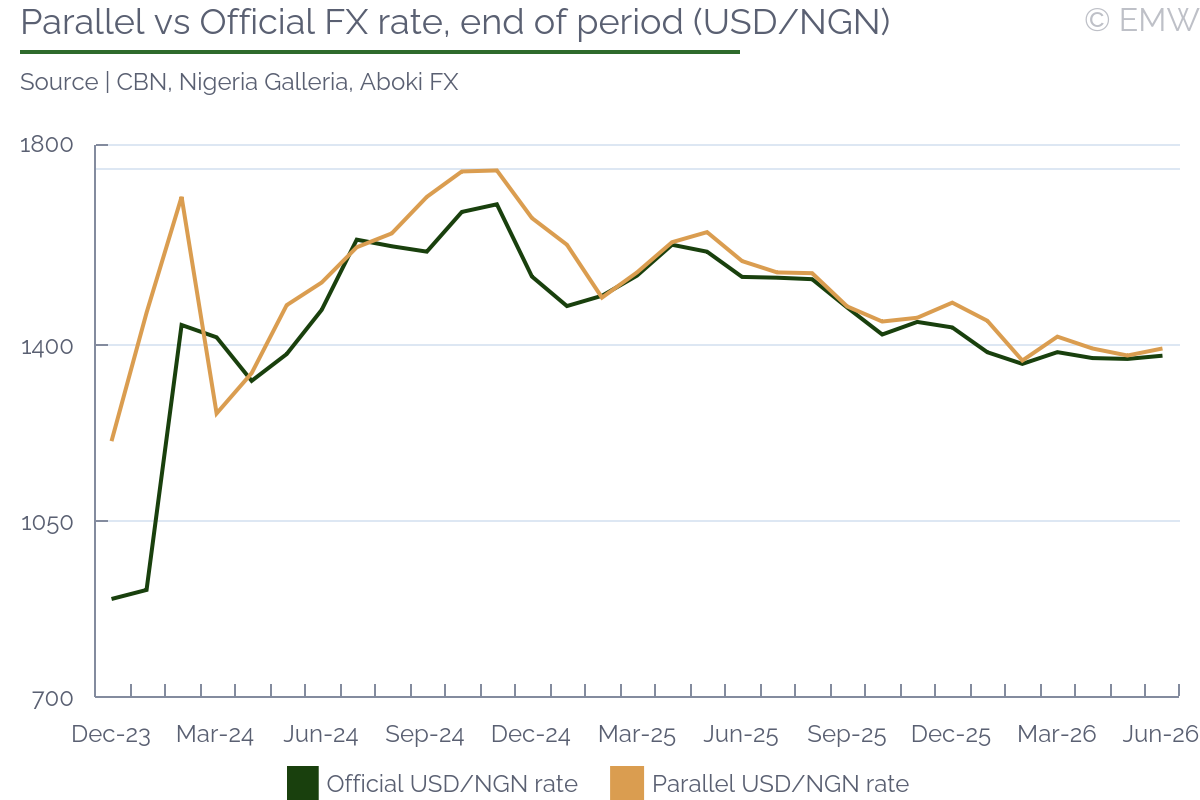

The gross external reserves of the central bank rose by USD 1.9bn or 3.8% m/m to USD 51.46bn as of end of June. This is the highest level of reserves the country has seen since 2009 (surpassing the CBN's year-end target of USD 51.04bn for 2026). Nigeria's reserves crossed the USD 50bn mark during the first week of June and continued to strengthen over the following weeks. For the year-to-date, reserves are up by a net of USD 5.96bn in 2026 (13.1%) from USD 45.5bn at the end of December 2025. The improvement has been supported by stronger oil export receipts and remittances, underpinned by elevated oil prices in the past few months and higher crude oil production. According to the NUPRC, Nigeria's total crude oil production increased by 2.2% m/m to 1.7mn bpd in May from 1.66mn bpd in April. This is a strong recovery from February, when total production was just 1.48mn bpd following the temporary shutdown of the Bonga facility for maintenance. Still, most analysts believe the government's 2026 production target of 1.84mn bpd is unlikely to be achieved, meaning lower-than-budgeted oil revenues.  Despite record reserves, the naira weakened noticeably in the last week of June and ended the month 0.5% weaker compared to end-May. At USD/NGN 1,383.62 on June 29, this was a roughly three-month low on the official market. In the latest Article IV report, the IMF urged the CBN to slow its pace of foreign reserve accumulation and maintain greater exchange rate flexibility, allowing the naira to move closer to its fair value. According to the Fund's models, the naira remains undervalued by approximately 25.6%. An important policy question for the second half of 2026 is whether the CBN should continue stockpiling dollars aggressively or allow the market to play a greater role in price discovery. In related news, a Nigerian policy group recently estimated that Nigeria spent USD 388bn defending the naira between 2000 and 2023 under previous administrations (averaging USD 16.8bn annually) with limited success. The Independent Media and Policy Initiative argues that the current administration's exchange rate unification has largely eliminated the need for such large-scale interventions.  |

|

|

|

| Country joins International Energy Agency as 14th associate member |

|

| Nigeria | Jul 02, 11:23 |

|

- IEA described Nigeria's admission as fastest in agency's history following May bid

- Membership gives Nigeria access to IEA energy data, expertise, policy support

The International Energy Agency (IEA) announced today (July 2) that Nigeria has officially joined the agency as an associate member after the IEA governing board unanimously approved its application. The country had submitted its bid in May 2026. IEA executive director Fatih Birol described it as the fastest admission in the agency's history. As a non-OECD associate member, Nigeria will be able to collaborate closely with the IEA on energy security, statistics, sustainable energy systems and emergency response mechanisms. Africa's largest oil producer joins 13 other associate countries, which have helped raise the IEA's coverage of global energy demand from 40% in 2015 to 80% in 2026. The agency currently also has 32 full-member countries. According to the IEA, Nigeria now has access to world-class real-time energy data and expert advice on investments, technologies and refining. Nigerian officials will also receive specialized training in areas such as oil and LNG markets and energy policy. Birol spoke of the country's contributions to global energy security (namely the Dangote Refinery's capacity) and said he sees no conflict with Nigeria's existing OPEC membership. |

|

|

|

| NNPC revenue, profit after tax decline despite solid oil production in May |

|

| Nigeria | Jul 02, 08:58 |

|

- Crude oil and condensate production rose to highest level in almost one year

- NNPC remitted NGN 4.86tn to Federation Account by end-May

- Progress continued on AKK and OB3 gas pipelines with milestones expected later in 2026

According to its latest monthly report, the Nigerian National Petroleum Company (NNPC) saw a decline in its financial performance in May despite maintaining stable oil and gas production. Revenue fell by 13% to NGN 4.33tn from NGN 4.97tn in April due to lower sales volume, while profit after tax declined to NGN 462bn from NGN 481bn. Gas sales fell 2.4% and crude oil and condensate sales declined nearly 20% during the month. The NNPC reported average crude oil and condensate production at 1.73mn bpd in May (up from 1.68mn bpd in April), the highest level recorded since July 2025. We note that this is slightly higher than the figure reported by the NUPRC for May (1.70mn bpd). Crude oil output increased to 1.47mn bpd from 1.43mn bpd according to the NNPC, while condensate production remained at 250,000 bpd. Natural gas production also edged higher to 7,774mn standard cubic feet per day. The NNPC reported that it remitted a cumulative NGN 4.86tn to the Federation Account by the end of May, up 30.8% from NGN 3.71tn a month earlier. | Oil production, various estimates (mn bpd) | | Jan-26 | Feb-26 | Mar-26 | Apr-26 | May-26 | | NUPRC (crude) | 1.46 | 1.31 | 1.38 | 1.49 | 1.53 | | NUPRC (crude + condensate) | 1.63 | 1.48 | 1.55 | 1.66 | 1.70 | | Budget target (crude + condensate) | 1.84 | 1.84 | 1.84 | 1.84 | 1.84 | | OPEC (secondary sources, crude only) | 1.49 | 1.42 | 1.45 | 1.52 | 1.52 | | OPEC quota (crude only) | 1.50 | 1.50 | 1.50 | 1.50 | 1.50 |

| | Source: NUPRC, OPEC |

Upstream pipeline availability improved significantly to 98% from 79%, although fuel availability at NNPC retail stations remained low at 57%. The company said it is addressing operational challenges (declining reservoir pressure, lifting constraints, maintenance shutdowns, facility reliability issues) to improve production and reduce output losses. The NNPC's report further indicated that work continued on the Ajaokuta-Kaduna-Kano (AKK) and Obiafu-Obrikom-Oben (OB3) gas pipeline projects, with early gas delivery to Abuja expected in 2026 and the OB3 pipeline targeted for commissioning by the end of Q3. |

|

|

|

|

| Nigeria | Jul 02, 08:01 |

|

Post-primary row: INEC, APC may clash over official Senate list (Punch) CBN issues fresh guidance on troubled banks' contract suspensions (Punch) NNPC revenue falls by N636bn despite stable oil production (Punch) Stakeholders seek fresh bidding for $243m pipeline stake (Punch) FG warns of worsening flood threat as rainy season peaks (Punch) State Police: All 36 States in Full Support and Will Give It Speedy Approval, Says Oyebanji (ThisDay) In New Partnership, Nigeria Secures $1.25bn World Bank Support to Boost Jobs (ThisDay) Troops Kill 662 Terrorists, Arrest 1,084 Suspects In Second Quarter Of 2026 (ThisDay) BOI signs $170 million iDICE fund management deal to boost Nigeria's tech, creative sectors (Nairametrics) Nigeria ranks 55th globally, tops Africa in IMD economic performance (Nairametrics) FTSE Russell faces backlash as securities dealers defend Nigeria's T+1 market reform (Nairametrics) |

|

|

|

| FG seeks compensation from South Africa for evacuated citizens' assets |

|

| Nigeria | Jul 02, 07:56 |

|

- Claims will cover businesses, properties, vehicles, other lost assets

- Authorities will verify compensation claims with South African counterparts

- Over 600 Nigerians have been evacuated in three batches since June

Following a government-organized voluntary evacuation of Nigerian citizens from South Africa, Nigerian authorities have formally listed compensation demands to the South African government. The evacuees left in the wake of rising xenophobic attacks and anti-immigrant protests in cities like Durban and Johannesburg. Nigeria's acting high commissioner to South Africa, Alexander Ajayi, confirmed on Wednesday (July 1) the federal government will seek compensation for businesses, properties, vehicles and other assets abandoned by the returnees. Ajayi reportedly discussed the matter with South Africa's deputy minister of finance and instructed returning citizens to provide accurate records of their abandoned assets. Nigeria's government committed to working with South African authorities to verify the claims for compensation. The latest group of 271 Nigerians departed Johannesburg earlier this week and arrived in Lagos. Before that, 334 Nigerians had been evacuated in two previous batches: 268 returned on June 11 and another 66 arrived on June 25. This brings the total to just over 600. Documented Nigerians in South Africa are around 30,000 according to the country's statistics office, while various unofficial estimates put undocumented Nigerians at over 100,000. Ajayi however rejected claims that most Nigerians in South Africa are undocumented. According to him, the majority entered the country legally but were affected by long delays in renewing immigration documents at the South African Home Affairs department. He strongly emphasized that Nigeria will not allow the labour and investments of its citizens to be lost or seized. |

|

|

|

| World Bank approves USD 1.25bn loan, 2026-2032 partnership framework |

|

| Nigeria | Jul 02, 07:39 |

|

- Partnership framework prioritises jobs, infrastructure, private sector-led growth

- Loan backs reforms in capital markets, power, digital regulation, trade

- Loan is second-largest World Bank financing approved for Nigeria under Tinubu

The World Bank on Wednesday (July 1) announced a seven-year country partnership framework for Nigeria covering 2026 to 2032, alongside the approval of a USD 1.25bn loan under the Nigeria Actions for Investment and Jobs Acceleration (NAIJA) Development Policy Financing programme. The announcement comes amid growing public criticism of the country's rising debt burden. According to the Bank, the new country partnership framework targets expanding energy access to 32mn people, improving internet connectivity for 58mn people and increasing healthcare services for 40mn. The programme also aims to support 9.5mn farmers with better agricultural inputs. The USD 1.25bn loan will support these efforts and other reforms intended to boost private sector-led growth. Planned measures include deepening capital markets, modernising regulations for the digital economy and e-governance, advancing power sector reforms and strengthening domestic revenue mobilisation. The funds are further intended to help reduce trade barriers under ECOWAS and AfCFTA commitments. The loan is the second-largest World Bank financing approved for Nigeria under President Bola Tinubu after the USD 1.5bn economic reform facility approved in June 2024. According to the Debt Management Office, Nigeria's debt to the World Bank Group increased from USD 17.81bn at the end of 2024 to USD 19.89bn by the end of 2025 (accounting for 38.36% of the country's total external debt stock). |

|

|

|

| Country failed to report public spending equal to 2% of GDP - IMF |

|

| Nigeria | Jul 02, 06:59 |

|

- Unreported expenditure created gap between reported fiscal deficit, actual financing needs

- Off-budget capital projects were the main source of missing expenditure

- Government is revising budget laws to incorporate previously unrecorded spending

Nigeria failed to report public spending equivalent to about 2% of GDP in recent budgets, according to comments from an IMF official. This created a gap between its reported fiscal deficit and actual financing needs. Speaking at a meeting with business executives in Lagos on Wednesday (July 1), the IMF's Nigeria resident representative Christian Ebeke said some capital expenditure was omitted from budget documents and implementation reports. The unrecorded expenditure reportedly stems mostly from major government projects executed outside the formal budget process. Ebeke said the lack of full disclosure complicates coordination between fiscal and monetary authorities because policymakers do not have a full picture of the government's financing requirements. It also raises questions about procurement processes and oversight. According to him, Nigerian authorities have begun addressing the issue by repealing and revising recent budget laws to include previously unrecorded expenditure. He stressed however that updated budget implementation reports are still needed to fully reflect the changes. This disclosure follows significant changes to Nigeria's 2026 budgeting cycle. President Bola Tinubu initially presented a NGN 58.18tn budget with a NGN 23.85tn deficit (4.28% of GDP). Lawmakers later expanded it to NGN 68.32tn and approved NGN 29.2tn in new borrowing. For the 2025 budget, weak budget implementation has led to repeated extensions of the capital component (first to June 2026 and then further to September 2026) which creates overlaps with the new 2026 budget year. |

|

|

|

| Israel |

|

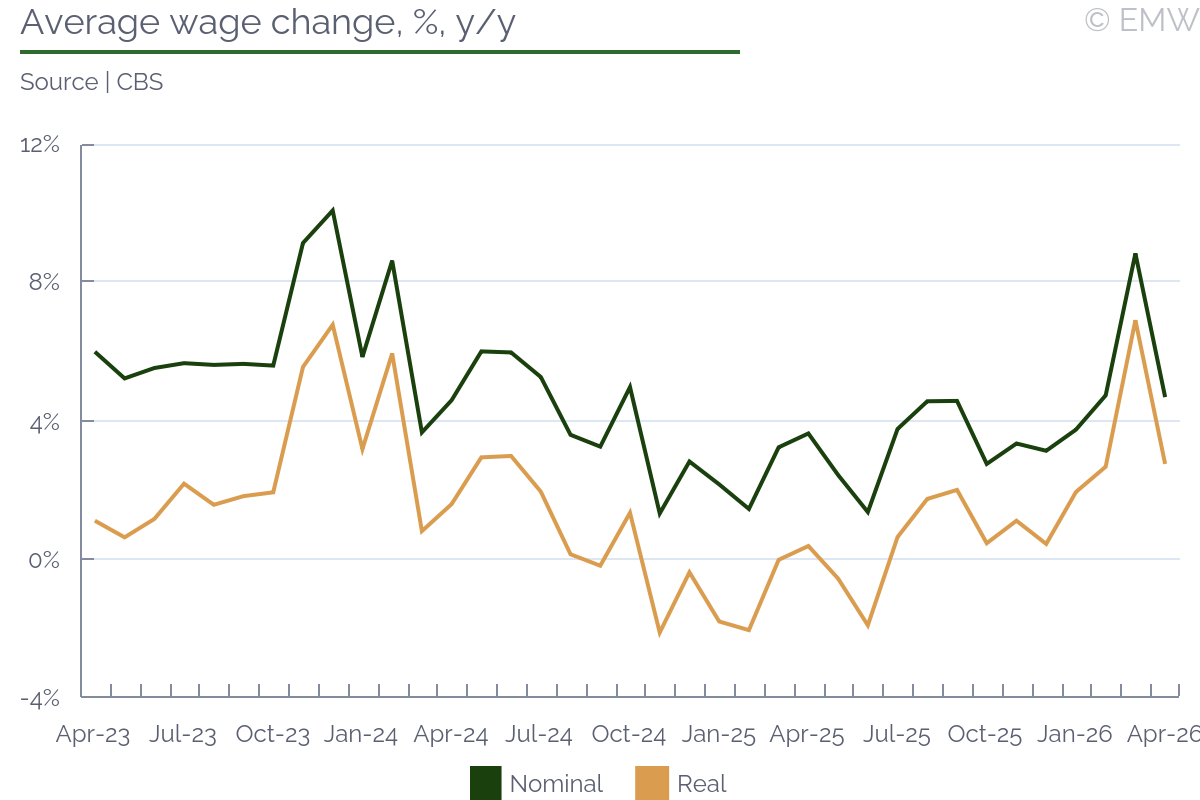

| Real average wage rises by 2.8% y/y in April |

|

| Israel | Jul 02, 12:13 |

|

- Wages increase at faster 6.7% y/y in May

- Employment continues recovering, returns to about normal in May

The real average wage of salaried Israeli workers rose by 2.8% y/y in April (seasonally-adjusted data), marking the tenth consecutive increase, the stat office (CBS) reported. The wage growth eased from the strong 6.9% y/y in March but we think that the March increase was likely affected by the war. Lower-paid workers were likely placed on unpaid leave due to the war and this effect has been in place in previous military conflicts as well as during the coronavirus period. In nominal sa terms, wages grew by 4.7% y/y in April, easing from 8.8% in March but the pace was about the same as in February. Wages in April should have been supported by the increase in the minimum wage by 3.3% as of Apr 1. The disposable income of the middle class should also have been affected positively by the widening in the tax income brackets. According to the flash estimate of the CBS based on partial data, the nominal average wage (non-adjusted) rose by a stronger 6.7% y/y in May and with inflation remaining at 1.9%, the growth in real wages should have also accelerated.  The number of Israeli employees, also part of the survey, fell by 1.6% y/y in April and the pace eased from the 7.6% y/y decline in March after rising in all months since Jun 2024. In monthly terms, the employee jobs switched to an increase of 6.8% m/m, indicating a return to normality. The job positions continued increasing m/m in May and switched back to growth in annual terms, too, hinting that the labour market has more or less recovered from the increase in hostilities in the previous two months. |

|

|

|

| High-tech companies raise USD 7.6bn in H1 - IVC-LeumiTech report |

|

| Israel | Jul 02, 06:58 |

|

- Number of deals continues to decrease, cyber security remains leader in fundraising

The high-tech companies have raised USD 7.6bn in H1, up by 52% y/y, according to a preliminary report of IVC-LeumiTech. The report showed a gradual and steady increase in companies' fundraising capacity in the past two years with the fundraising rate increasing to USD 3.8bn per quarter in the last two quarters from an average of USD 3.0bn previously. The peak was recorded in Q2 when fundraising reached USD 4.2bn. However, the number of deals continued to decrease to 97 in Q2 while the number was at about 105 deals on average per quarter in 2023 and about 140 deals on average in 2019-2020. The cyber sector remained market leader accounting for 33.8% of the fundraising in H1 and the report confirmed a significant acceleration in the financing of the defence-tech, space and quantum computing sectors. The report also showed that late-stage companies are in a better position to cope with the challenges from the strong NIS environment with their fundraising up by 70% y/y while early-stage companies have shown a decrease in their fundraising. The share of foreign funds among all active investors stabilized at 69.1% in H1, following the 68.4% recorded in 2025. |

|

|

|

| Most opposition voters support Arab participation in ruling – poll |

|

| Israel | Jul 02, 06:38 |

|

- Most opposition leaders do not want to team with Arab parties

- Ruling coalition voters do not want Arab parties to support government

Most of the voters supporting the parties currently in opposition support the inclusion of the Arab parties in the next government, according to a poll by the Reichman University's Institute for Liberty and Responsibility quoted by local daily Haaretz. A total of 37% support a government with the participation of ministers from the Israeli Arab sector, 18% support a coalition comprising the Arab parties but without Arab ministers, and 19% said they prefer Arab parties to support the next government but not to be part of the ruling coalition. We note that the previous government comprised most of the current opposition parties as well as an Arab party (Ra'am) for the first time ever but there were no Arab ministers. Latest polls indicate that the opposition parties would find it difficult to reach a majority and establish the next government without including Ra'am again. The other Arab parties are vehemently opposing becoming part of the ruling coalition. However, most of the opposition leaders have said that they do not want to team with Arab parties to establish government. Back to the poll, 77% of the voters supporting Netanyahu's coalition bloc said they completely object to any participation of an Arab party in the government. Only 8% support Arab parties providing support from the outside, 6% support Arab parties to be part of the ruling coalition without holding ministerial positions and 4% support Arab Israelis to become ministers. |

|

|

|

| Knesset plenum passes in first reading Torah Study bill |

|

| Israel | Jul 02, 06:20 |

|

- Move comes as Haredi parties threaten to unseat government

The Knesset plenum passed in the first out of three necessary readings the controversial bill enshrining Torah study into Basic Law. Total of 63 MKs voted in favour while 53 MKs were against. The piece of legislation, which passed a preliminary reading a month ago, is part of a package seeking to enable yeshiva students to continue receiving state subsidies without completing the necessary army service. It was promoted by the two Haredi junior partners who threatened to move to unseat the government if the coalition does not advance the favourable to their sector legislation. The other bill temporarily bans arrests of yeshiva draft dodgers. The bills are seen as a compensation to the Haredi parties for the inability of the government to pass a law that would enable army evasion by yeshiva students. Draft evasion has become a hot topic against the backdrop of shortages of soldiers and the high cost of drafting reservists for long periods of time. |

|

|

|

|

| Israel | Jul 02, 05:53 |

|

Bennett and Lapid Hoped to Force Eisenkot's Hand, but May Need Him to Survive (Haaretz) Israel Police clash with protesters commemorating 1,000 days since Oct. 7 outside Knesset (Jerusalem Post) Knesset passes in first reading bill to enshrine Torah study into Basic Law (Jerusalem Post) Next Israeli gov't main issue will be controlling defence budget, Bank Hapoalim CEO told conference (Jerusalem Post) Knesset passes in first reading bill to enshrine Torah study into Basic Law (Jerusalem Post) A surge in capital raising in Israeli high-tech: USD 7.6bn raised in the first half of 2026 (Calcalist) The price of raw milk drops by 5%, but consumers will continue to pay dearly (Calcalist) A turnaround at the top? The big exits reveal where Israeli high-tech is headed (TheMarker) 37,000 votes will go to hell, and this is just the beginning: Likud changes election procedures (TheMarker) The Ministry of Finance presents: A revolution in the savings market, contrary to the position of the Capital Market Authority (Globes) The Thousandth Day of October 7: The Remaining Threats and What the Signed Agreement Is Worth (Globes) For the first time: Israeli high-tech has become more expensive than its Silicon Valley counterpart (Globes) |

|

|

|

| Airports Authority launches tender to expand Ben Gurion airport major terminal |

|

| Israel | Jul 02, 05:41 |

|

- Goal is to prepare for increase in passengers to 40mn annually by 2040

The Airports Authority published on Wednesday a tender for expanding by 70% the capacity of the main terminal, Terminal 3, at the country's main international airport Ben Gurion near Tel Aviv, local media reported. According to the plan, a new wing will be built covering an area of some 63,000 square meters, which will include 86 check-in counters, passenger lounges, restaurants, commercial areas and duty-free shops. The goal is to provide a response to the expected increase in traffic to 40mn passengers annually by 2040. Earlier this week, the Authority announced the establishment of a new unit to control flights, which will significantly increase the number of takeoffs and landings to 60 from 36 currently. Ben Gurion airport has another terminal, Terminal 1, which operates low-cost and domestic flights. |

|

|

|

| Start-ups raise significant USD 3.3bn financing in June |

|

| Israel | Jul 01, 16:26 |

|

- Amount is much higher than in any single month in past several years

- Several companies complete large fundraisings in June

Local start-ups secured USD 3.3bn worth of financing in June, according to local daily Globes, which warned that the amount might be higher as some companies prefer not to publish information about investments they have received. The amount is much higher than in any single month in recent years. Several companies completed large fundraisings in June - marketing analytics company Appsflyer, which raised USD 1.3bn, cybersecurity company Cyera raised USD 600mn, networking solutions company DriveNets raised USD 410mn, cybersecurity company Dream Security raised USD 260mn, observability company Coralogix raised USD 200mn and waterless cooling solutions company ZutaCore raised USD 100mn. The amount raised so far this year reached USD 8.4bn, by 75% higher y/y. Capital raising reached USD 10.7bn in 2025, according to IVC-LeumiTech, up from USD 9.58bn in 2024 and USD 6.9bn in 2023 but still significantly lower than USD 15bn in 2022, and the record high of USD 25.6bn in 2021. |

|

|

|

| IMF recommends rebuilding fiscal buffers; ensuring price, financial stability |

|

| Israel | Jul 01, 15:12 |

|

- Government should pursue gradual, credible fiscal consolidation, focus on growth-friendly revenue measures

- Inflation to rise temporarily, monetary policy stance should be moderately tight

- IMF keeps inflation, growth projections unchanged from WEO report

The IMF listed rebuilding fiscal buffers, raising labour supply and productivity, and ensuring price and financial stability as major priorities for Israel against the backdrop of looming medium-term growth challenges, the institution said in the concluding Article IV consultations statement. The IMF said the government needed to pursue a gradual and credible fiscal consolidation focusing on growth-friendly revenue measures and stressed that improving spending efficiency remained important. The government needed to stabilise the public debt, the IMF said and pointed to the elevated defence spending and risks for crowding out essential civil spending, namely infrastructure. The IMF also said that increasing labour participation across different groups was important too as well as improving infrastructure, progressing with product market reforms and maintaining the competitiveness in the high-tech sector. The IMF expects inflation to rise temporarily due to energy prices and supply constraints and therefore recommends a moderately tight monetary policy. It urged the BoI to be cautious and monitor risks to inflation as well as assess the impact of the latest rate cut. We note that inflation has been surprising positively in the past few months and the overall sentiments are that the monetary easing would continue on Monday, Jul 6, with another 25bps rate cut to 3.50%. Yet, we also note that the MPC has always stressed that its moves would be cautious and gradual. Back to the report, the IMF also urged banks to assess risks related to their real estate exposure and adds that the financial system remains resilient, with well-capitalised, profitable, and liquid banks. The IMF projects the economy to grow by 3.5% in 2026 and 4.4% in 2027, maintaining its forecasts from the latest WEO report. Yet, the 2026 projection was revised down from the initial 4.8% in the Article IV concluding statement from early February due to the Iran war that started later that month and continued for more than a month. The IMF sees the medium-term outlook as weaker than before putting the potential growth at about 3.5%, down by 0.5pps from its pre-2023 average. Regional developments might push growth forecast either up or down. Public debt is seen steadily rising to 70.7% of GDP by the end of 2027 with budget deficit exceeding the 4.9% of GDP target this year. The IMF has also confirmed its inflation forecast from the WEO report and noted that the risks are tilted to the upside. |

|

|

|

| Jordan |

|

| World Bank grants loan worth USD 700mn to support kingdom's reform agenga |

|

| Jordan | Jul 02, 08:51 |

|

- Financing targets private investment, business reforms, and job creation

- World Bank support reflects confidence in Jordan's macroeconomic management

The World Bank approved a USD 700mn loan to support Jordan's efforts to translate macroeconomic stability into stronger private investment, faster economic growth, and higher-quality job creation, according to a statement by the institution. The financing, provided under the Jordan Growth and Competitiveness Development Policy Financing II programme, will back reforms aimed at improving the business environment, expanding access to finance, and accelerating the country's green and digital transformation. The programme comes as Jordan has maintained macroeconomic stability despite persistent regional tensions, with the economy growing by 2.8% in 2025 while also securing its first sovereign credit rating upgrade in more than two decades. The World Bank believes the next stage of Jordan's reform agenda should focus on converting this stability into higher investment, stronger private-sector activity, and more sustainable employment. The reform package targets several structural bottlenecks by streamlining business licensing, modernising regulations for digital and cross-border transactions, expanding financing options for businesses, and encouraging private investment in the energy sector. Particular emphasis is placed on improving access to finance for micro, small, and medium-sized enterprises, which account for nearly all businesses in Jordan, through new funding instruments such as crowdfunding and cash flow-based lending. The programme also supports broader structural reforms, including expanding financial inclusion, promoting green finance, modernising insurance legislation, and advancing digital government payments. These measures are expected to improve efficiency, reduce transaction costs, and strengthen Jordan's attractiveness as an investment destination. Overall, the new financing underscores international confidence in Jordan's reform agenda. While macroeconomic stability has largely been secured, sustaining stronger long-term growth will depend on the successful implementation of structural reforms that encourage private investment, enhance productivity, and create more inclusive employment opportunities. |

|

|

|

| MENA |

|

| Lasting US-Iran ceasefire is key to GCC banks' continuing resilience – Fitch |

|

| MENA | Jul 01, 17:04 |

|

- GCC bank ratings are mostly driven by expectations of sovereign support

- Banks generally limited exposure to tourism

- Funding and liquidity are a rating strength for the region's banks

The durability of the US-Iran ceasefire and prospects for a permanent de-escalation are central to whether the banking systems of the six countries of the GCC remain resilient to the effects of the conflict, according to Fitch Ratings. The agreement extended the ceasefire agreed on 8 April and set an extendable 60-day deadline for the US and Iran to reach a peace deal. GCC banks' credit fundamentals have proved resilient to the conflict and can remain so in the second half of 2026, assuming no resumption of military combat on a scale that could lead to lasting damage to key energy infrastructure or other GCC assets, or significantly prolong the closure of the strait. If the ceasefire holds, effects on regional banks will mostly stem from the conflict's second-round macro-economic effects, which are already being felt. Fitch is forecasting non-oil GDP to contract in three of the six GCC countries this year, with only Oman forecast to post stronger non-oil growth than in 2025. Weaker non-oil growth will lead to lower loan growth than the agency anticipated at the start of 2026, contribute to moderate asset quality deterioration, and weaken profitability. GCC bank ratings are mostly driven by expectations of sovereign support, and negative actions since the conflict began have been limited to Rating Watch Negative placements on Qatari banks affected by Qatar's sovereign Rating Watch Negative. The two main transmission channels from the conflict are asset quality and liquidity. Asset quality will be affected by weaker borrower performance in sectors including infrastructure, tourism, aviation, logistics, transport and real estate. Banks generally have limited exposure to tourism, and lending to small and medium enterprises, which may be less able than larger corporates to withstand asset quality pressures, is also a low share of total sector lending. However, a deeper Dubai property market correction than anticipated pre-conflict would likely put pressure on asset quality ratios, particularly at smaller UAE banks with higher real estate concentrations. Funding and liquidity are a rating strength for the region's banks, which are predominantly deposit-funded. Sticky government and government-related deposits account for 20% - 30% of sector deposits. Moreover, after an initial pause in public debt issuance, market access has proven more resilient than initially expected at the start of the conflict, as seen in the recent resumption of some public issuance, particularly of subordinated instruments. Finally, GCC banks have good reserve buffers, and forbearance will help them cope with the impact of the conflict, if necessary. The forbearance measures would be withdrawn if geopolitical conditions no longer justified them, according to Fitch Ratings. |

|

|

|

| Morocco |

|

| WB to provide USD 265mn financing for Ifahsa Hydro |

|

| Morocco | Jul 02, 04:59 |

|

- Ifahsa expected to support at least 1GW of new renewable capacity and crowd in roughly USD 1bn of private capital

The WB will provide USD 265mn in financing for Morocco's new 300MW Ifahsa pumped-storage hydropower project, according to a press release. The project acts as a large-scale storage system, allowing excess solar and wind power to be stored and dispatched when demand peaks and is deemed a key step in strengthening grid flexibility and accelerating renewable integration. Ifahsa is expected to support at least 1GW of new renewable capacity and crowd in roughly USD 1bn of private capital. It will displace around 3TWh of fossil-fuel generation annually, cutting about 1.7mn tonnes of CO₂ and improving Morocco's energy security. Construction is expected to generate 820 direct jobs per year, with wider spillovers into export-oriented sectors seeking lower-carbon supply chains. The financing package combines IBRD funding, concessional climate finance, and grants, alongside co-financing from the African Development Bank. Implementation will be led by Office National de l'Électricité et de l'Eau potable. |

|

|

|

| Qatar |

|

| Qatar attracts FDI of USD 3.4bn in 2025 |

|

| Qatar | Jul 01, 14:19 |

|

- More than 50% of FDI goes towards greenfield projects

- Invest Qatar expands its global footprint

In 2025, Qatar attracted USD 3.4bn in FDI capital expenditure across 373 projects that generated 15,051 new jobs, according to the Qatar News Agency. More than 50% of total FDI capex was directed towards greenfield projects, and nearly half of all FDI projects were classified as medium to high tech investments. The 373 projects in 2025 represent a 52% jump compared to the 241 projects in 2024. Similarly, total capital expenditure rose 24% from USD 2.74bn in 2024 to USD 3.4bn in 2025. The top five sectors in 2025 - consumer products, business services, food and beverages, software and IT services, and textiles, accounted for 69% of total projects. This suggests that Qatar is successfully bridging its traditional industries (consumer products, textiles, food) with high-growth digital sectors (software and IT services). During 2025, Invest Qatar, the country's investment promotion agency, expanded by establishing dedicated representative offices in critical international financial hubs: London, New York, Paris, Mumbai, and Istanbul. |

|

|

|

| Saudi Arabia |

|

|

| Saudi Arabia | Jul 02, 08:59 |

|

Saudi Arabia to auction mining rights for three areas (AGBI) Saudis are skipping developers to build their own homes (AGBI) BlueFive Capital to acquire 70% stake in UAE dredging firm Gulf Cobla (Zawya) Saudi reforms, digital innovation take center stage at Saudi Water Week (Arab News) Saudi interior minister receives Pakistani counterpart in Riyadh (Arab News) |

|

|

|

| Tunisia |

|

| Finance committee clears USD 430mn World Bank-backed financing for STEG reform |

|

| Tunisia | Jul 02, 11:34 |

|

- STEG debt stands at TND 7.356bn and unpaid bills at TND 6.061bn as of Jun 23

- Funding is tied to cost recovery, governance and renewables

- MPs warn loans alone will not fix STEG's structural problems

The parliament's finance committee approved two state-guarantee agreements last week for around USD 430mn in World Bank-backed financing for state electricity company STEG, clearing the way for a plenary vote on the package. The funding is linked to the Tunisia Energy Reliability, Efficiency and Governance programme and forms part of the 2024-2028 STEG reform plan. The committee debate highlighted the scale of STEG's financial stress with a debt stock of TND 7.356bn as of Jun 23 and unpaid bills from public and private clients worth TND 6.061bn. The company is also squeezed by tariffs that remain well below production costs, accumulated subsidy claims, technical and commercial losses, and exposure to fuel prices and the exchange rate. MP Issam Chouchane said STEG's full restructuring would require at least TND 12bn and warned that new borrowing would not be enough without stronger management and collection. The World Bank-backed programme is not a direct balance-sheet bailout but it is intended to support reforms that could reduce STEG's financing needs over time. The TEREG programme is expected to enable Tunisia to progress towards its goal of mobilizing USD 2.8bn in private investment to add 2.8 GW of new solar and wind capacity by 2028 and is expected to generate over 30,000 jobs, primarily during the construction phase of renewable energy projects. It will also contribute to reducing electricity supply costs by 23%, improving the cost recovery rate of STEG from 60% to 80%, and reducing state subsidies by TND 2.045bn. During the discussions, MPs questioned the slow progress of major power-sector projects and pointed to service deterioration, delayed connections and electricity theft. The financing may help keep STEG's reform plan moving but parliament's debate showed concern that sovereign-guaranteed borrowing could become a recurring fiscal burden if the utility's arrears, losses and governance problems are not addressed. |

|

|

|

| Finance minister asks banks to support H2 issuance as debt burden shifts inward |

|

| Tunisia | Jul 02, 10:06 |

|

- H2 issuance will rely heavily on banks, but the ministry has not published the auction calendar

- 2026 Treasury resources are set at TND 27.1bn, with domestic borrowing covering the largest share

- Eurobond repayment in July reduces external rollover risk, while higher domestic financing raises crowding-out and liquidity risks

The finance ministry has asked banks and financial institutions to continue supporting the state budget through active participation in Treasury bond issues planned for the second half of 2026. The call was made during a meeting between finance minister Michket Slama Khaldi and the heads of banking and financial institutions, where the ministry presented Treasury bond market activity and the H2 issuance programme. The calendar was shown to banks but has not been published with amounts, dates or maturities. The finance ministry has not yet published budget execution reports for 2026, leaving limited visibility on the progress of state funding. Under the 2026 finance act, Treasury resources are set at TND 27.064bn, mainly to cover the TND 11.015bn budget deficit, TND 7.932bn of domestic debt principal repayments and TND 7.917bn of external debt principal repayments. Financing is expected to come mostly from domestic borrowing, at TND 19.056bn, compared with TND 6.808bn from external borrowing and TND 1.2bn from other Treasury resources. The domestic financing plan includes TND 2.5bn through 52-week Treasury bills, TND 4.84bn through BTA Treasury bonds, TND 716mn through domestic foreign-currency borrowing and TND 11bn through the central bank. The meeting also comes ahead of the repayment of EUR 700mn 6.375% Eurobond maturing on Jul 15, the country's last outstanding international bond. At current exchange rates, the principal and final coupon imply a total outflow of around TND 2.5bn. BCT governor Fethi Zouhaier Nouri has presented the repayment as part of a broader external deleveraging trend. Speaking at the Tunisia Investment Forum last week, he said Tunisia had entered a phase of net external debt reduction since 2023, with long-term external debt falling from about TND 82bn to TND 68bn, or around 18%. He also said yields on Tunisian international bonds had fallen to around 7% in the first five months of 2026 from more than 30% in 2023, reflecting improved market perception after Tunisia continued to meet its external commitments. The improvement in external debt metrics does not remove the financing pressure, but shifts it inward. Finance ministry data show total public debt rising to TND 141.7bn at end-2025, with domestic debt increasing to TND 86.2bn, or 60.8% of the total, while external debt declined to TND 55.5bn, or 39.2%. BCT data also show outstanding BTA Treasury bonds at TND 34.4bn at end-June 2026, up by TND 9.0bn y/y, while short-term Treasury-bill outstanding fell to TND 1.7bn. The shift lowers immediate Eurobond rollover risk and reduces exposure to external market closures, but increases the state's dependence on local banks and the central bank. Higher Treasury absorption raises banks' sovereign exposure and crowds out private-sector credit, while larger direct BCT financing adds liquidity and inflation risks. |

|

|

|

| Angola |

|

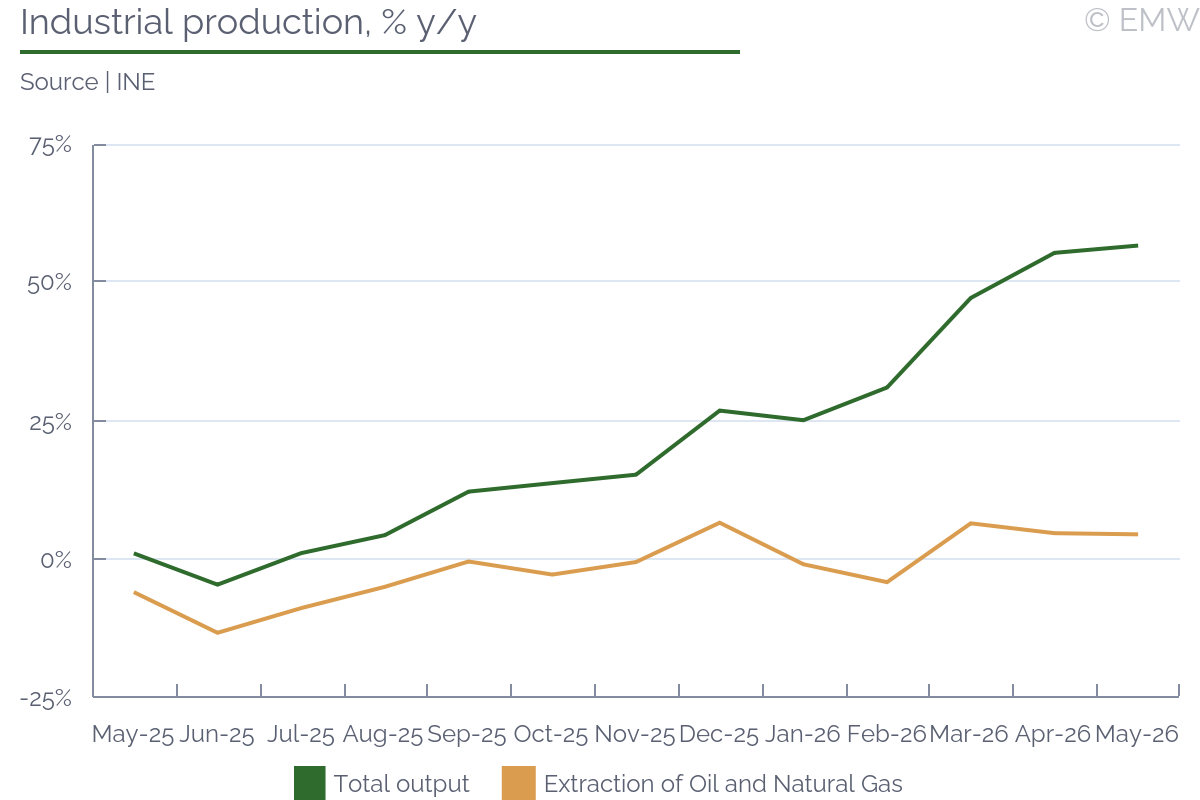

| | Industrial output growth accelerates to 56.7% y/y in May |

|

| Angola | Jul 02, 07:38 |

|

- Manufacturing continues to outpace extractives, rising 210.8% y/y

- Consumer goods remain the core growth driver, led by food production and import substitution

- Extractive sector slows further to 5.7% y/y, reinforcing gradual shift toward non-oil industrial activity

Industrial output growth accelerated further to 56.7% y/y in May from 55.4% y/y in Apr, according to Angola's statistical office INE, extending the strong expansion trend into a fifth consecutive month. Manufacturing remained the main driver, with growth accelerating to 210.8% y/y from 191.5% y/y in Apr, while extractive industries slowed to 5.7% y/y from 6.9% y/y. Electricity output also moderated but remained strong at 39.2% y/y, down from 56.2% y/y in Apr.  Manufacturing gains remained broad-based and increasingly concentrated in consumer-oriented sectors. Food, beverage and tobacco production accelerated to 284.5% y/y from 260.4% y/y, with food industries alone rising 294.4% y/y, underscoring continued domestic demand strength and substitution away from imports. Metallurgical industries also strengthened to 78.0% y/y from 63.8% y/y, while textiles held broadly steady at 45.9% y/y. By contrast, petroleum and chemical products slowed sharply to 5.9% y/y from 8.0% y/y, pointing to a fading boost from refinery ramp-ups. By use category, consumer goods remained the dominant growth engine, accelerating to 276.2% y/y from 252.6% y/y in Apr. Intermediate goods growth moderated to 24.9% y/y from 29.3% y/y, while capital goods edged up to 28.5% y/y from 28.1% y/y. Energy products slowed to 7.4% y/y from 8.3% y/y, reflecting softer hydrocarbon output. On a monthly basis, industrial production rose 7.3% m/m, led by consumer goods and extractives, suggesting momentum remains firm entering mid-year. The May data reinforce Angola's ongoing industrial rebalancing toward manufacturing-led growth, with food processing and light industry increasingly offsetting softer oil sector momentum. Base effects still amplify the headline, but the continued broadening across consumer and capital goods points to firmer underlying activity. Manufacturing should remain the main support for industrial activity through 2026, particularly as food processing capacity expands. However, the modest slowdown in oil production growth highlights persistent structural constraints in the extractive sector. Oil output is still expected to remain broadly flat around 1.05mn bpd over the medium term as declining output from mature fields offsets gains from new developments. This limits upside for export receipts and fiscal revenues, keeping Angola's external position and budget performance highly sensitive to global oil price movements despite improving non-oil industrial activity. | Industrial output, % y/y | | Mar-26 | Apr-26 | May-26 | | TOTAL INDUSTRY (%, y/y) | 47.2% | 55.4% | 56.7% | | Extractive Industry | 7.9% | 6.9% | 5.7% | | Extraction of Oil and Natural Gas | 6.5% | 4.8% | 4.5% | | Extraction of Diamonds | 23.2% | 32.0% | 17.9% | | Other Extractive Industries | 15.6% | 13.8% | 15.8% | | Manufacturing Industry | 164.3% | 191.5% | 210.8% | | Food, Beverage and Tobacco Industries | 218.9% | 260.4% | 284.5% | | Food Industries | 228.3% | 272.1% | 294.4% | | Beverage and Tobacco Industries | 185.4% | 219.1% | 249.3% | | Manufacture of Textiles, Clothing and Footwear | 30.0% | 45.8% | 45.9% | | Wood Industries | 18.0% | 19.7% | 19.3% | | Manufacture of Paper Pulp, Publishing and Printing | 11.2% | 13.8% | 13.9% | | Manufacture of Petroleum, Chemical and Other Products | 20.1% | 8.0% | 5.9% | | Metallurgical Industries | 63.0% | 63.8% | 78.0% | | Manufacture of Mach., Equip. and Automobiles | 11.3% | 28.1% | 28.5% | | Manufacture of Furniture, Mattresses and Others | 21.4% | 21.5% | 27.4% | | | Intermediate Goods (A1) | 28.6% | 29.3% | 24.9% | | Capital Goods (A2) | 11.3% | 28.1% | 28.5% | | Consumer Goods (A3) | 212.3% | 252.6% | 276.2% | | Energy Products (A4) | 9.7% | 8.3% | 7.4% |

| | Source: INE |

|

|

|

|

| Ethiopia |

|

| Govt designates tourism as strategic growth pillar |

|

| Ethiopia | Jul 02, 07:47 |

|

- Tourism among five priority economic sectors to diversify growth and increase foreign exchange earnings

- Prime Minister says sector can attract investment, create jobs and strengthen linkages across the wider economy

Government designated tourism as one of its five strategic economic pillars as the government seeks to diversify growth, attract investment and increase foreign exchange earnings, Prime Minister Abiy Ahmed said. Abiy said tourism had been identified as a key driver of sustainable economic transformation after detailed policy analysis showed agriculture alone could not deliver the country's long-term development ambitions. The prime minister said tourism provides significant opportunities to generate employment, support small businesses, attract foreign direct investment and strengthen domestic industries. He noted that the global tourism industry generates around USD 12.6tn annually, arguing Ethiopia should capture a larger share of international tourism spending. Abiy said tourism creates demand for locally produced goods and services, including handicrafts, traditional clothing, food and cultural experiences, while exposing international visitors to investment opportunities across the economy. Tourism revenues would also support heritage conservation, environmental protection and infrastructure development. The govt's strategic designation of tourism is timely and evidence-based, as official data shows the sector rebounded to record 1.4mn arrivals and USD 5.2bn in revenue in FY 2025/26, a remarkable recovery from COVID-19 lows. According to the World Tourism Organization (WTO), tourism's current GDP contribution stands at roughly one-tenth, but its potential is vastly larger given Ethiopia's 12 UNESCO World Heritage Sites. The UN Economic Commission for Africa (UNECA) projects the sector could contribute over USD 5bn annually to GDP by 2030, welcoming 2mn visitors. Critically, the USD 5.2bn in foreign exchange directly alleviates balance of payments pressures flagged by the IMF. Realizing this demands infrastructure investment, market diversification, and promotional gains. With targeted reforms, tourism can anchor Ethiopia's transformation, generating vital jobs and exports. |

|

|

|

| | IMF completes fifth ECF review, unlocking USD 464mn |

|

| Ethiopia | Jul 02, 06:59 |

|

- Fund says reforms continue to deliver strong macroeconomic outcomes despite Middle East war shock

- Rephasing brings forward USD 200mn to cushion higher fuel import costs, with total disbursements reaching USD 2.65bn

- Reserves projected at 2.1 months of imports, GDP growth at 9.2%, inflation at 11.7%, current account deficit at 2.5% of GDP in FY25/26

- IMF welcomes progress on official and commercial debt restructuring, including agreement-in-principle with Eurobond holders

The Executive Board of the International Monetary Fund (IMF) completed the fifth review of Ethiopia's Extended Credit Facility (ECF), approving an immediate disbursement of approximately USD 464mn. This brings total disbursements under the 48-month, USD 3.4bn programme to about USD 2.65bn, including around USD 200mn in financing brought forward to help Ethiopia absorb pressures arising from the war in the Middle East, particularly higher imported fuel costs. The IMF stated that the authorities continue to make solid progress on their reform agenda, delivering favourable macroeconomic outcomes through strong exports, robust revenue mobilisation, reserve accumulation and continued debt restructuring efforts despite a more challenging external environment. Programme performance remained broadly in line with commitments, with all quantitative performance criteria and most indicative targets achieved. The only shortfall related to the government's contribution to the Productive Safety Nets Programme, which came in below target as donor financing exceeded expectations, leaving total beneficiary support above programme objectives through additional assistance for urban households affected by the external shock. The IMF also approved a rephasing of programme access to provide additional near-term financing support in response to the evolving external environment. The Fund's latest projections continue to point to a strong medium-term macroeconomic outlook despite a slight deterioration in some external indicators. Real GDP growth is projected at 9.2% in FY25/26 before moderating to 7.8% in FY26/27 and recovering to 8.2% in FY27/28. Average inflation is forecast at 11.7% in FY25/26 before edging up slightly to 12.3% in FY26/27 and then declining to single digits thereafter. The current account deficit is projected at 2.5% of GDP in FY25/26 before narrowing to 1.3% in FY26/27. In a statement following the Board discussion, Deputy Managing Director Nigel Clarke stressed that continued progress on central bank governance reforms, financial sector oversight and the appointment of new independent members to the National Bank of Ethiopia's board will be essential to strengthening institutional autonomy and sustaining Ethiopia's reform momentum. The IMF noted that maintaining a tight monetary stance remains appropriate to anchor inflation expectations. The authorities continue advancing foreign exchange market reforms by partially easing exchange restrictions, developing the interbank FX market and strengthening competition among banks to improve price discovery. The Fund also highlighted the importance of enforcing net open foreign exchange position limits, modernising the monetary policy framework and eventually withdrawing the National Bank of Ethiopia from gold market operations in a manner consistent with reserve accumulation objectives. On the fiscal front, strong tax revenue performance and prudent expenditure management were commended, while continued revenue administration reforms, gradual fuel subsidy removal and stronger fiscal transparency were identified as essential for sustaining fiscal stability and protecting priority social spending. Regarding debt, the IMF welcomed continued progress under the Common Framework, noting that several bilateral agreements have now been signed with official creditors while negotiations with commercial creditors have advanced significantly. The Fund also welcomed the agreement-in-principle reached with Eurobond holders, stating that the financing assurances received remain consistent with programme parameters. It reiterated that completing the debt restructuring process through continued good-faith engagement with creditors, prudent borrowing policies and the development of a deeper domestic debt market will be critical to restoring debt sustainability and limiting future vulnerabilities. We recall that the fourth review under the ECF arrangement was completed in January, unlocking USD 261mn and bringing total disbursements to about USD 2.18bn. At that time, reserves were projected to rise to 2.2 months of imports by the end of FY25/26. The latest projections incorporate the impact of the Middle East conflict, with reserves now forecast at 2.1 months this fiscal year before increasing to 2.7 months in FY26/27. While the external shock has modestly weakened the near-term external outlook, the accelerated IMF financing and continued progress in debt restructuring should help cushion financing pressures as negotiations with remaining creditors continue. |

|

|

|

| | Fitch says Eurobond deal should bring closer exit from Restricted Default |

|

| Ethiopia | Jul 01, 14:34 |

|

- Agreement in principle moves Ethiopia closer to exiting Restricted Default, subject to OCC approval and sufficient creditor participation

- Fitch highlights reserves, exports and macroeconomic reforms as key indicators to watch during Ethiopia's restructuring process

- Investor focus is shifting from debt restructuring to Ethiopia's medium-term credit fundamentals

Ethiopia's agreement in principle with an Ad Hoc Committee representing approximately 45% of holders of its USD 1bn Eurobond marks a significant step toward normalising relations with external commercial creditors, according to Fitch Ratings. In response to questions from EmergingMarketWatch, the rating agency said the agreement should bring closer exit from Restricted Default and that, once Ethiopia has normalised relations with a significant majority of its external commercial creditors, it would move the Long-Term Foreign-Currency Issuer Default Rating (LTFC IDR) out of 'Restricted Default' (RD) and assign a rating based on a forward-looking assessment of the sovereign's willingness and capacity to honour its foreign-currency debt obligations. Asked about the main rating implications, Fitch said: "Ethiopia's agreement in principle with Eurobond holders should bring closer exit from Restricted Default. Once Ethiopia has normalised relations with a significant majority of its external commercial creditors, we would move its Long-Term Foreign-Currency Issuer Default Rating (LTFC IDR) out of 'Restricted Default' (RD) and assign a rating based on a forward-looking assessment of the sovereign's willingness and capacity to honour its foreign-currency debt obligations. The agreement between the ad hoc committee of Eurobond holders for Ethiopia's single Eurobond brings this normalisation a step closer." Remaining hurdles before restructuring is completed However, Fitch emphasised that key issues still need to be resolved before the restructuring can be considered fully complete. Asked what key issues still need to be resolved, Fitch said: "The agreement in principal still has to be approved by Ethiopia's official creditor committee (OCC) before it can launch an exchange offer. It has been submitted to Ethiopia's OCC co-chairs (France and China), who provided their non-objection, but it still has to be formally approved by the OCC on a comparability of treatment basis. Progress towards a debt exchange could also be interrupted if the deal reached with the ad hoc committee fails to secure sufficient support among wider Eurobond holders. The ad hoc committee holds some 45% of the Eurobond. The Eurobond documentation contains a collective action clause (set at 75% of principal amount), that eases an orderly debt restructuring by reducing the influence of holdout creditors." Fitch highlights key macroeconomic indicators to watch Looking beyond the Eurobond deal itself, Fitch said in its comments that it is monitoring several indicators closely, including reserves, fiscal discipline, domestic borrowing pressures and progress on external financing. Asked which indicators Fitch would be watching most closely, Fitch said: "Ethiopia has continued to make progress on macroeconomic reforms since July 2024 under the IMF's Extended Credit Facility Arrangement. Macroeconomic stability has improved significantly, supported by strong growth and export earnings (mainly coffee and gold) in FY25 and FY26, disinflation since July 2024, and reserve accumulation. We anticipate the authorities will continue deepening reforms, including further reducing financial repression, enhancing revenue mobilisation, and developing the FX market. Nevertheless, FX shortage persists despite the National Bank of Ethiopia (NBE) continued efforts to liberalise its foreign-exchange and investment regime. Reserve buildup has enabled periodic foreign-exchange auctions to ease shortages, and bids reached USD 1 billion against USD 500 million offered at an auction conducted in May. The Ethiopian birr fell by 63% against the US dollar in 2025, but the pace of depreciation has moderated, with the currency weakening by only 2.4% in 5M26." The next challenge is rebuilding sovereign credit - our assessment We note that Fitch's comments reveal a subtle but important transition in Ethiopia's sovereign credit narrative. Where Fitch's October 2025 rating affirmation focused primarily on the default event and unresolved private creditor negotiations, the agency's responses to our questions provide additional insight into the macroeconomic indicators it is monitoring as Ethiopia's restructuring process progresses. In our view, these comments provide a useful framework for assessing the country's evolving sovereign credit profile: First, the restructuring has entered a more execution-focused phase. The principal financial terms have now been agreed in principle with the Ad Hoc Committee. The remaining uncertainties relate primarily to formal approvals, creditor participation and implementation rather than negotiations over the core economic structure of the deal. Second, the Eurobond is relatively small in relation to Ethiopia's overall debt stock, but strategically significant because its successful restructuring would restore normal relations with private capital markets. At USD 1bn, the bond represents only a fraction of Ethiopia's USD 33.5bn external debt stock and USD 51.8bn total public debt stock recorded in the first 9 months of FY 2025/26. This represents less than 3% of Ethiopia's external public debt stock, illustrating that the Eurobond's importance lies less in its size than in its signaling effect for future market access and investor confidence. Of this debt, external debt stood at USD 33.5bn while domestic debt reached USD 18.3bn. According to the Ministry of Finance, USD 22.1bn of the external debt is owed by the federal government while state-owned enterprises account for USD 11.5bn. Following the recently signed Eurobond AIP, the central bank governor announced that Ethiopia expects to move into a lower debt-risk category within the next year as debt restructuring and macroeconomic reforms strengthen public finances. While that reflects growing official confidence, whether this materialises will ultimately depend on successful completion of the restructuring, continued implementation of IMF-supported reforms and sustained improvements in external liquidity. Therefore, a successful restructuring would signal to stakeholders that Ethiopia can negotiate in good faith with private creditors, a prerequisite for any future international bond issuance. Beyond the Eurobond, Ethiopia continues discussions with Chinese lenders over its approximately USD 5.4bn in outstanding Chinese loans, including financing for the Addis Ababa-Djibouti railway. According to a recent AidData study, Ethiopia could reduce debt servicing costs by up to USD 778mn if it secures a Kenya-style restructuring of these loans, converting some dollar-denominated debt into renminbi and securing longer repayment periods. Third, in our view, Ethiopia's sovereign credit story is gradually transitioning from debt resolution toward longer-term credit quality. The October 2025 RD affirmation focused on the default itself, the non-payment of the USD 33mn coupon, the breakdown of private creditor talks, and the absence of a resolution. As the restructuring process advances, stakeholders are likely to place increasing emphasis on macroeconomic reforms, external liquidity, reserve accumulation and policy credibility alongside the mechanics of the restructuring itself. Once the Restricted Default designation is eventually removed, the sustainability of these reforms is likely to become increasingly important in assessing Ethiopia's sovereign credit profile. Fourth, the IMF programme has become the anchor of Ethiopia's credit story. Many of the macroeconomic indicators highlighted by Fitch are closely linked to reforms being implemented under Ethiopia's USD3.4bn IMF Extended Credit Facility arrangement. The recent staff-level agreement on the fifth review, which would unlock approximately USD 468mn and bring total disbursements to around USD 2.65bn, shows the Fund's continued support. However, the IMF's warning that risks to the outlook have increased materially due to the Middle East conflict and commodity price volatility should not be overlooked. Completion of the restructuring is therefore a necessary condition for Ethiopia's exit from Restricted Default. However, because Fitch has stated that any new rating will be based on a forward-looking assessment of Ethiopia's willingness and capacity to service foreign-currency debt, sustained implementation of IMF-supported reforms is likely to remain an important consideration in that assessment. Fifth, market access is likely to return gradually, not immediately. Even after Ethiopia exits RD, investors and creditors will require evidence of a functioning FX market, sustained reserve accumulation, policy credibility, and continued reform momentum before the sovereign can issue new bonds at competitive yields. This emphasis is unsurprising because stronger reserve buffers improve a sovereign's capacity to service external obligations and reduce refinancing risk, making them one of the key indicators supporting future rating upgrades. The NBE's periodic FX auctions and the moderation in birr depreciation are positive signals, but they are early-stage indicators. On the fiscal front, the IMF's April 2026 Fiscal Monitor projects the general government deficit widening to 1.8% of GDP in 2026 from 1.2% in 2025, reflecting a jump in expenditure to 13.1% of GDP while revenue rises only modestly to 11.3%. The deficit is then expected to narrow to 1.0% of GDP in 2027, but the near-term widening shows that fiscal consolidation remains a work in progress. Encouragingly, the IMF projects public debt to decline from 43.1% of GDP in 2025 to 40.4% in 2026 and further to 31.1% by 2029, supported by strong nominal GDP growth. However, the Fund's broader warnings about thin fiscal buffers and the need for revenue mobilisation apply acutely. Until the fiscal trajectory shows clearer signs of sustained improvement, investors and creditors are likely to remain cautious. The New Money Warrant included in the Eurobond AIP agreement is designed precisely to facilitate Ethiopia's eventual return to international bond markets, but investors and creditors are unlikely to exercise that option unless macroeconomic reforms continue to strengthen confidence in the country's repayment capacity. The fiscal constraints are further illustrated by Ethiopia's FY 2026/27 draft budget, which allocates ETB 542.1bn to domestic and external debt repayment nearly 30% of total expenditure and 43.8% of recurrent spending. The government also plans to raise ETB 329bn through domestic borrowing, raising the risk that public borrowing crowds out private sector credit just as manufacturers, exporters and farmers need financing to respond to reforms. This means that even after the Eurobond restructuring is completed, domestic fiscal pressures will remain a significant constraint on Ethiopia's credit profile. Additionally, the projected decline in the debt-to-GDP ratio from 43.1% in 2025 to 40.4% in 2026 and further to 31.1% by 2029 reflects the IMF's baseline assumption of robust real GDP growth of 9.2% in 2026 and 7.9% in 2027, which continues to erode the debt burden through a favourable interest-growth differential. This shows that sustained high growth is a critical assumption underpinning Ethiopia's debt sustainability, and any growth shock would materially alter this trajectory. Conclusion In our view, the agreement in principle represents less the end of Ethiopia's restructuring process than the beginning of a new phase in its sovereign credit story. The key question for investors and creditors is no longer whether Ethiopia can restructure its Eurobond, but whether the authorities can convert that restructuring into durable improvements in external liquidity, policy credibility and market access. It is our view that once the restructuring process is completed, these broader macroeconomic and external indicators are likely to play an increasingly important role in shaping Ethiopia's future sovereign credit profile. Equally important, exiting Restricted Default does not imply Ethiopia will necessarily receive a high sovereign rating. Fitch has indicated it will assign a new Long-Term Foreign-Currency Issuer Default Rating based on a forward-looking assessment of credit fundamentals rather than on the restructuring itself. This means investors and creditors should distinguish between the technical removal of a default designation and the sovereign's underlying creditworthiness, which will continue to depend on external liquidity, fiscal performance, reserve adequacy and policy credibility. |

|

|

|

| Gabon |

|

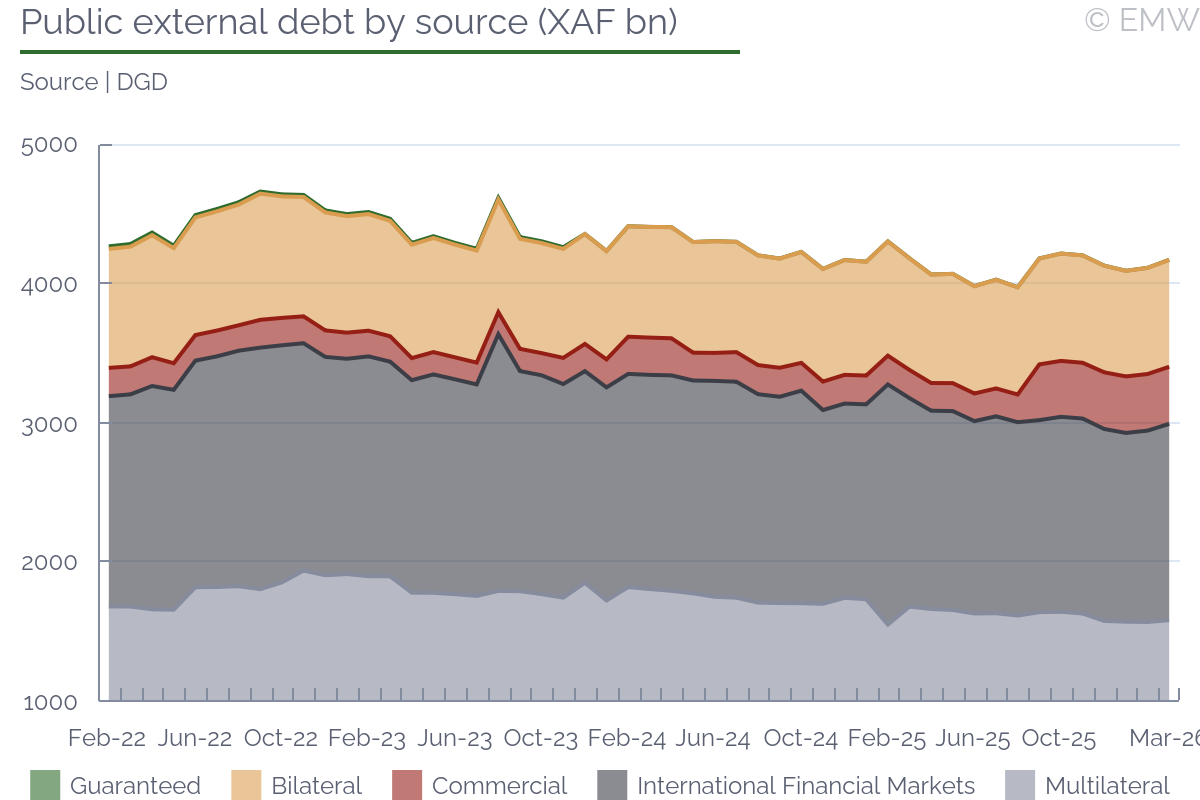

| | Public debt rises 22.5% y/y to XAF 8,877bn at end-March |

|

| Gabon | Jul 02, 10:39 |

|

- External debt amounted to XAF 4,169.7bn; domestic debt at XAF 4,707.1bn

- Major external lenders included World Bank (XAF 10.2bn) and AfDB (XAF 4.1bn)

- Total public debt service reached XAF 354.5bn in March

Gabon's total public debt stock amounted to XAF 8,876.7bn at end-March 2026, according to the latest data from the debt directorate. Total debt rose by 22.5% y/y, mainly reflecting higher domestic debt which surged by 53.5% y/y and reached XAF 4,707.1bn. The domestic share in total debt increased from 42% in March 2025 to 53% by March 2026. The debt directorate attributes this to increased borrowing on the regional financial market. Domestic debt comprised XAF 441.2bn in bank loans, XAF 750.3bn in moratorium debt and XAF 3,515.5bn in regional market debt. Meanwhile, external debt amounted to XAF 4,169.7bn as of March (falling by 0.3% from the level one year ago). External debt consisted of XAF 766.7bn in bilateral obligations, XAF 409.3bn in commercial debt, XAF 1,586.5bn in multilateral debt and XAF 1,407.2bn in international market debt.  Total loan disbursements reached XAF 185.0bn as of March, of which XAF 17.2bn were external drawdowns and XAF 167.8bn were domestic drawdowns. External financing consisted of project loans, including XAF 10.2bn from the World Bank for the HISWACA-SOP2 project and XAF 4.1bn from the African Development Bank for infrastructure and economic diversification. On the domestic side, financing consisted entirely of Treasury bonds (OTA) totaling XAF 167.8bn (mobilised via regional and local primary dealers). According to the debt directorate's report, total public debt service amounted to XAF 354.5bn as of March, comprising XAF 132.8bn in external debt service and XAF 221.7bn in domestic debt service. The external service included XAF 73.2bn in principal repayments and XAF 59.5bn in interest, while the domestic portion consisted of XAF 116.3bn in principal and XAF 105.4bn in interest. Meanwhile, debt arrears stood at XAF 526.5bn in March, including XAF 95.5bn in current due payments and XAF 431bn in older arrears. We note that, with the IMF's support, Gabon is currently undertaking an audit of the country's public debt. Government officials have previously said this will be completed by the end of this month. | Public debt stock | | Nov-25 | Dec-25 | Jan-26 | Feb-26 | Mar-26 | | Total debt | 8,547.24 | 8,780.34 | 8,689.60 | 8,741.96 | 8,876.74 | | External debt | 4,201.52 | 4,127.62 | 4,091.02 | 4,112.16 | 4,169.68 | | Domestic debt | 4,345.72 | 4,652.72 | 4,598.58 | 4,629.80 | 4,707.06 | | Banking | 444.09 | 444.09 | 441.24 | 441.24 | 441.24 | | Moratorium | 726.33 | 758.68 | 756.80 | 756.72 | 750.32 | | Regional Financial Markets | 3,175.30 | 3,449.95 | 3,400.54 | 3,431.84 | 3,515.50 | | Total debt y/y change | 21.80% | 23.09% | 23.04% | 18.97% | 22.47% | | External debt y/y change | 2.37% | -0.98% | -1.57% | -4.41% | -0.27% | | Domestic debt y/y change | 49.19% | 56.93% | 58.24% | 51.97% | 53.47% |

| | Source: DGD |

|

|

|

|

| Govt declares water emergency as authorities discover illegal water trade |

|

| Gabon | Jul 02, 08:17 |

|

- Govt deployed security forces to distribute drinking water in Greater Libreville

- Authorities uncovered illegal network allegedly involving SEEG employees

- Govt is now setting water prices with payments to be made directly to security personnel

The Gabonese government declared a state of 'water emergency' on Wednesday (July 1) and deployed security forces to distribute drinking water across Greater Libreville. Announcing the measure, water and energy minister Philippe Tonangoye said firefighters, the Republican Guard, the military engineering corps and the national gendarmerie will deliver water to affected neighbourhoods. This announcement follows a recent meeting between president Brice Clotaire Oligui Nguema and employees of Société d'Énergie et d'Eau du Gabon (SEEG), after authorities said they had uncovered an illegal water-selling network involving some utility staff, with water reportedly sold for XAF 10,000-20,000 or more per cubic metre. The authorities have now launched a crackdown on the black market for water. They ordered security forces to dismantle illegal supply storage facilities and to seize 55 vehicles allegedly used in the trade. The government has also set fixed prices of XAF 3,000 per cubic metre, XAF 600 for a 200-litre drum and XAF 300 for a 100-litre delivery. Payments have to be made directly to security personnel. |

|

|

|

| Ghana |

|

| TOR refinery management in recapitalisation talks with government |

|

| Ghana | Jul 02, 08:59 |

|

- Managing director says this could involve releasing TOR's outstanding share of ESLA receivables

- He says company's balance sheet needs strengthening given GHS 7.9bn accumulated deficit, GHS 4.5bn negative equity

- Board chairman has revealed that of GHS 3.4bn collected for TOR from ESLA, only GHS 1.5bn has been released