We have launched coverage of Bangladesh

| BCRA to keep policy rate and crawling peg moving closely in line with m/m CPI |

| Copom leaves room for either an additional cut or pause in easing cycle |

| CNB will likely hold in August, but door for more rate hikes remains open |

| MPC likely to hold interest rates in Jul despite US-Iran deal, slowing inflation |

| MPC clearly shifts into rate-cut mode, cycle to be re-considered in September |

| RBI to hold rate in upcoming August meeting |

| Bank Indonesia to stand pat after 100bps cumulative rate hikes |

| Inflation slows in May, June H1, but no monetary easing should follow |

| MPC to hold policy rate in July to allow for return to disinflation |

| SBP likely to hold policy rate for extended period |

| BSP likely to raise policy rate on Aug 27 |

| MPC is clearly on hold for some time, cut questions arise |

| CBT likely to hold as caution still outweighs easing signals |

| MPC reinforces 'hold' stance as inflation risks become more balanced |

| BanRep's Jun 30 hike call splits 50-75bp as fiscal rally meets min wage shock |

| Chances for rate cut on Jul 7 strengthen due to soft inflation |

| NBK cuts base rate by 100bps, downgrades year-end inflation forecast |

| BOK set to raise policy rate by 25bps in July as inflation pressures intensify |

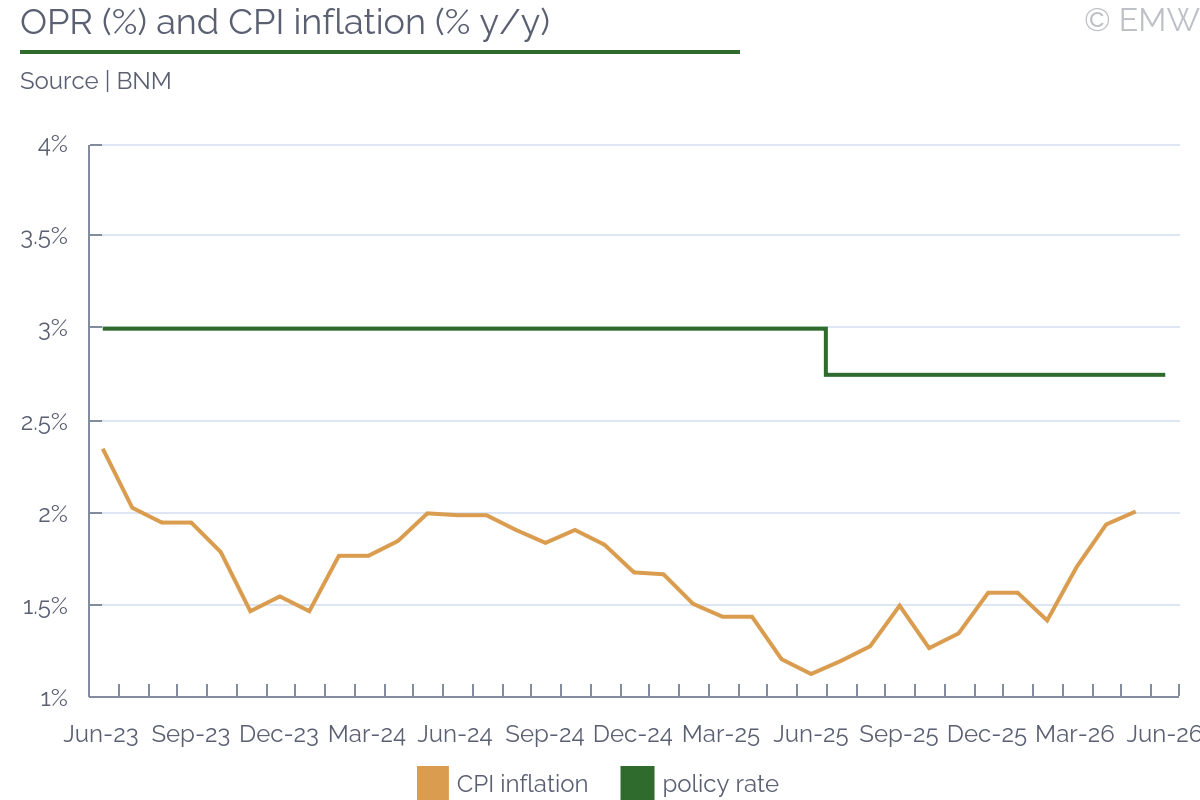

| BNM set to keep rates unchanged despite more hawkish Fed |

| Renewed inflation pressures delay prospects for rate cuts this year |

| Slowing inflation strengthens case for another CBR rate cut |

| MPC July call finely balanced after May hike and weaker expectations |

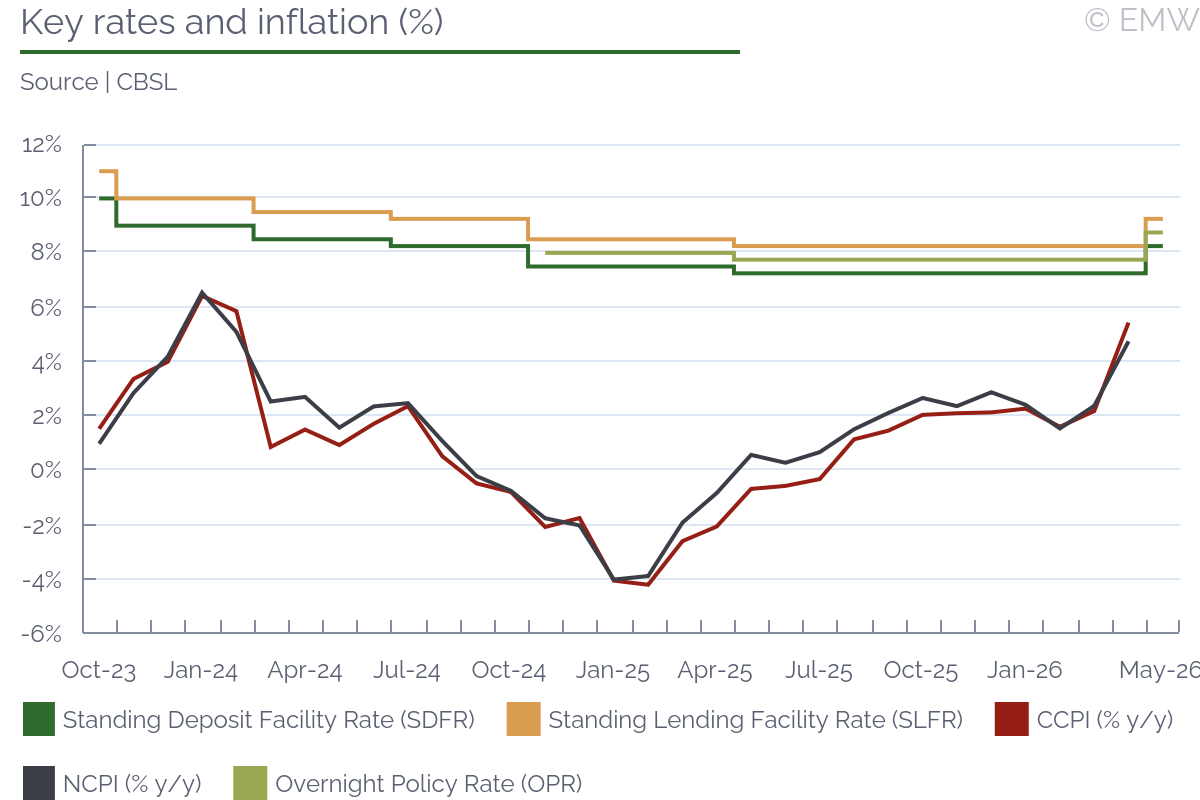

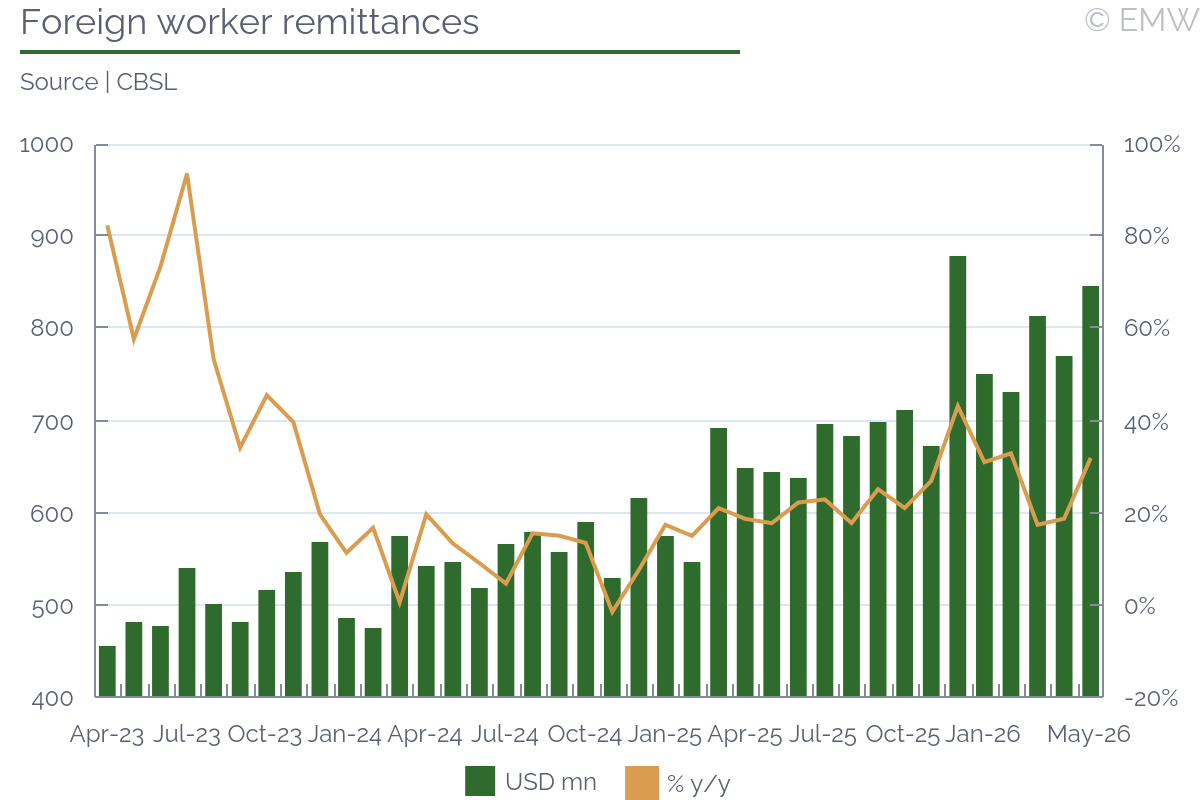

| CBSL to keep key rate flat in wait-and-assess mode in July |

| BOT’s MPC likely to maintain policy rate at 1.00% on Aug 26 |

| Central bank likely to keep key rate on hold again |

| BCRA to keep policy rate and crawling peg moving closely in line with m/m CPI |

- BCRA to raise quickly next time CPI inflation comes at 7.0% m/m or close

- BCRA needs to keep monthly effective rate and crawling peg closely in step with inflation to reduce export delay and portfolio dollarization incentives

- Unsustainable deficit+debt dynamics keep BCRA from pursuing positive real rates or depreciation

- BCRA can only passively respond to rising inflation, this status quo likely remains until regime change

The BCRA's future monetary policy rate decisions will remain bounded by the evolution of effective inflation, expected inflation for the short-term, and the interest rate limitations the central bank faces if it is to keep the official real exchange rate steady in the coming year, which is something the bank is paying close attention to. The BCRA hiked its benchmark 28-day bill rate by 300bps to 78.0% in mid-March to accommodate the monthly effective rate at 6.5%, up from 6.3%, in what was the first move for the rate since last September. The decision was taken following the release of a surprisingly high 6.6% m/m CPI inflation print for February and with market expectations of a similar reading for March. The BCRA is likely to raise another 200bps or 300bps if the CPI reading for March is close 7.0% m/m, unless high-frequency price trackers show a deceleration in early April.

Monetary policy has been passive for most of the past three years, sitting under the weight of massive fiscal dominance and past policy mistakes, and there are no prospects for this to change until the end of this government in December. To put it in short, the BCRA needs to keep its monthly effective benchmark rate and the official exchange rate crawling peg moving right in step with CPI inflation, and it doesn't have room to deviate much or for too long, which means monetary policy should be fairly predictable this year. The BCRA has slightly more room to delay rate cuts if inflation declines than it has room to delay rate hikes if inflation rises, but it seems very unlikely that inflation will decline this year anyway.

The dangerous inflation spiral and the massive real exchange rate appreciation that took place in 2021-22 put pressure on the BCRA to raise nominal interest rates and push the pace on the crawling peg when inflation rises. If the crawling peg lags versus inflation, the government would be increasing the incentives for exporters to withhold sales abroad and wait for an inevitable devaluation, while also reducing competitiveness (most exporters are forced to convert their FX income into local currency). This would add to an FX market crisis that has the government burning through its low FX reserves. However, if the nominal crawling peg is to move faster, interest rates also need to rise in step to avoid creating incentives to delay exports. Interest rates that at least match inflation are also key to discourage portfolio dollarization through parallel exchange rates, which are an increasingly important benchmark for price-setting practices.

The BCRA also needs to be careful of not going too high with real rates because it would contribute to the explosiveness of public debt dynamics and inflation. With the government running a fiscal deficit of more than 4.0% of GDP every year despite having virtually no access to market financing, the deficit has been covered by a mix of inflation tax and central bank balance sheet deterioration. The higher the real interest rate goes, the faster the deterioration of the central bank's balance sheet and the growth of the federal government's short-term debt. However, the evolution of market financing for the government and the BCRA's remunerated liabilities suggests that the room to get financing through these avenues is pretty much closed now, which only leaves inflation tax as an option. In this scenario, nominal interest rate hikes are inflationary as long as there are no drivers to increase the private sector's willingness to finance the government.

| Ask the editor | Back to contents |

| Copom leaves room for either an additional cut or pause in easing cycle |

- MPC meeting: Aug 4-5, 2026

- Current policy rate: 14.25%

- EmergingMarketWatch forecast: Hold

The BCB's Monetary Policy Committee (Copom) cut its benchmark rate by 25bps at its latest sitting on Jun 16-17, but left its next monetary policy decision open with likely outcomes being an additional 25-bp cut in the key Selic rate to 14.00% or a pause in the easing cycle, according our view of the post-sitting statement and the minutes to the meeting released Jun 23. After cutting the Selic by 25bps for a third consecutive meeting in June, the Copom said it had considered multiple interest-rate paths and noted that bringing inflation back to the 3.00% target within the relevant policy horizon (Q4 2027) would require abrupt adjustments to the Selic, potentially resulting in inflation remaining below target in subsequent quarters. The committee likewise assessed alternative scenarios involving temporary pauses in the easing cycle followed by additional rate cuts, which it said would reduce output volatility while still returning inflation to target by Q1 2028, the relevant horizon for the next policy meeting. In our view, the main message is that the committee remains uncomfortable with the inflation outlook but appears willing to tolerate a slower convergence to target to avoid excessive volatility in economic activity, reflecting a somewhat more dovish approach despite its hawkish tone.

As a result, we believe the Copom could either deliver one additional 25-bp cut at its next policy sitting on Aug 4-5 before pausing the cycle or pause as early as the August meeting. In our view, if inflation indicators remain elevated and economic activity continues to be supported by a robust labor market, which seems likely, a pause appears more likely. But of course there is also much time until the August sitting, meaning the coming data will be important.

That is especially so since the Copom said in its minutes that the Middle East conflict has pushed inflation expectations higher across all horizons, particularly for 2028, requiring a more restrictive monetary stance than would otherwise be necessary. The persistent deterioration in inflation expectations is likely to continue weighing on the committee's decisions. However, we note that the Copom's less clear communication may itself contribute to this trend, given uncertainty surrounding the future path of monetary policy and the committee's decision to extend the relevant policy horizon in order to justify the June rate cut. If this deterioration in inflation expectations, reinforced by mixed signals from the Copom, continues, it could further increase pressure for a pause in the ongoing Selic "calibration" cycle.

Another factor supporting a pause is the committee's updated inflation risk balance, which is now tilted to the upside due to risks associated with demand-supporting fiscal measures in an election year. If economic data continue to show resilient activity supported by these measures, such as the income tax reform and new credit programs, demand-driven inflationary pressures are also likely to reinforce the case for pausing the easing cycle.

Overall, after delivering a third consecutive 25-bp cut and bringing the Selic rate to 14.25% in June, the Copom's communication has become less clear regarding its next move, which should remain data-dependent, as noted. In our view, the minutes could result in a marginal deterioration in the committee's credibility as its members chose to rely on a horizon beyond the traditional 18-month relevant window to justify the June cut, which could require a firmer stance during the remainder of the year to reverse that perception. Amid elevated external uncertainties surrounding the agreement to end the Middle East conflict and domestic uncertainties related to the October elections, coming inflation and activity data, as well as comments from BCB directors, will be key to assessing the next decision. At this stage, we believe inflationary pressures are more likely to push the Copom toward a pause than toward additional rate cuts.

| Copom structure and latest voting results | ||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||

| Source: BCB |

| Ask the editor | Back to contents |

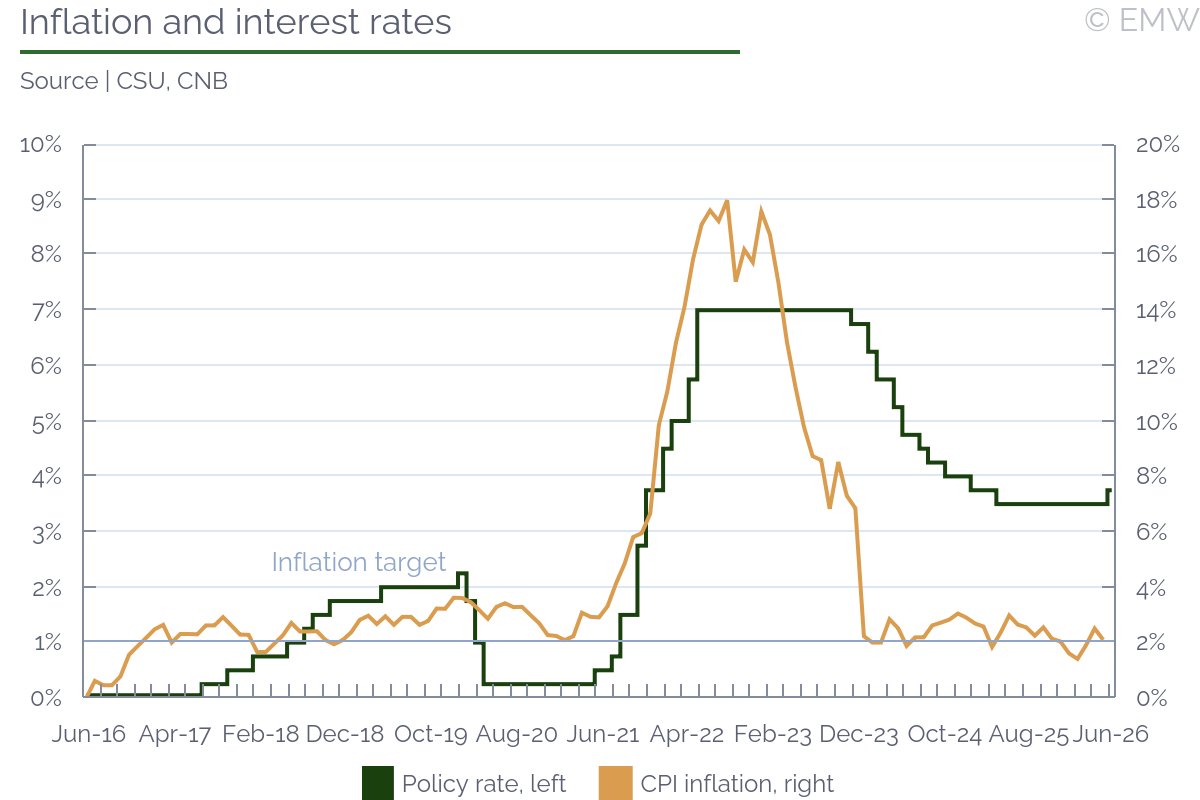

| CNB will likely hold in August, but door for more rate hikes remains open |

- Next MPC meeting: Aug 6, 2026

- Current policy rate: 3.75%

- EmergingMarketWatch forecast: Hold

Rationale: After the first rate hike in 4 years, we believe the CNB board will hold for now, especially after assurances that the June hike was not the start of a new tightening cycle. We still expect one more rate hike in 2026, given that the reasons given for the June hike are unlikely to go away. Namely, the labour market is likely to remain relatively tight, particularly in the service sector, and there is no major likelihood that consumer lending growth will decelerate soon. Even though there are some anecdotal reports that property price growth is slowing down, we doubt rising mortgage rates will be a major deterrent to housing loan growth. The main reason is that expectations continue to be that property prices will go up, which makes it more rational to get a mortgage now, despite deteriorating credit terms, rather than wait, when a mortgage could become prohibitively expensive.

You may note that we are excluding any mention of price data, but the reason is mostly because this is what the CNB board did in June. All high-frequency data points suggest that inflation will ease further, likely slightly under 2% y/y in June, even though core inflation remains elevated. However, the CNB argued that inflation is expected to pick up and reach close to 3% y/y in late 2026 and early 2027, which is why they acted preventively. With this rationale, current price data becomes less relevant, so we don't expect the CNB board's view to shift even if inflation ends up lower than anticipated in June, or even in Q3. What benign price data could do is postponed the other 25bp rate hike we expect before the end of 2026.

At this point, we are still uncertain about the timing of that second rate hike, though we believe it will arrive not later than November. If money supply and nominal wages shows no sign of easing growth by the MPC meeting in September, then the odds are for another 25bp hike then. On the other hand, if there is some growth slowdown, and inflation remains consistently below the CNB's projections, then the next rate hike could take place in November. We doubt that the CNB board will push the policy rate beyond 4%, unless core inflation starts accelerating again, and exceeds 3% y/y. Naturally, any re-escalation of conflict in the Middle East will also push towards more monetary tightening. After the CNB is happy that inflation is contained, we expect the policy rate to return to 3.50%, around the middle of 2027. However, we don't expect further easing, given that the ETS2 is still planned to be implemented at the beginning of 2028. According to the latest available CNB analysis, the direct impact on inflation is projected to reach 0.4pps, while second-round effects could be around 0.2pps.

Further Reading:

CNB board statement from latest MPC meeting, Jun 18, 2026

Post-meeting press conference, Jun 18, 2026 (in Czech)

Q&A after the latest MPC meeting, Jun 18, 2026

Minutes from the latest MPC meeting, Jun 18, 2026

Monetary Policy Report, May 2026

Macroeconomic forecast, May 2026

Meeting with analysts, May 11, 2026

CNB board members' presentations, articles, interviews (Czech)

CNB board members' presentations, articles, interviews (English)

| Ask the editor | Back to contents |

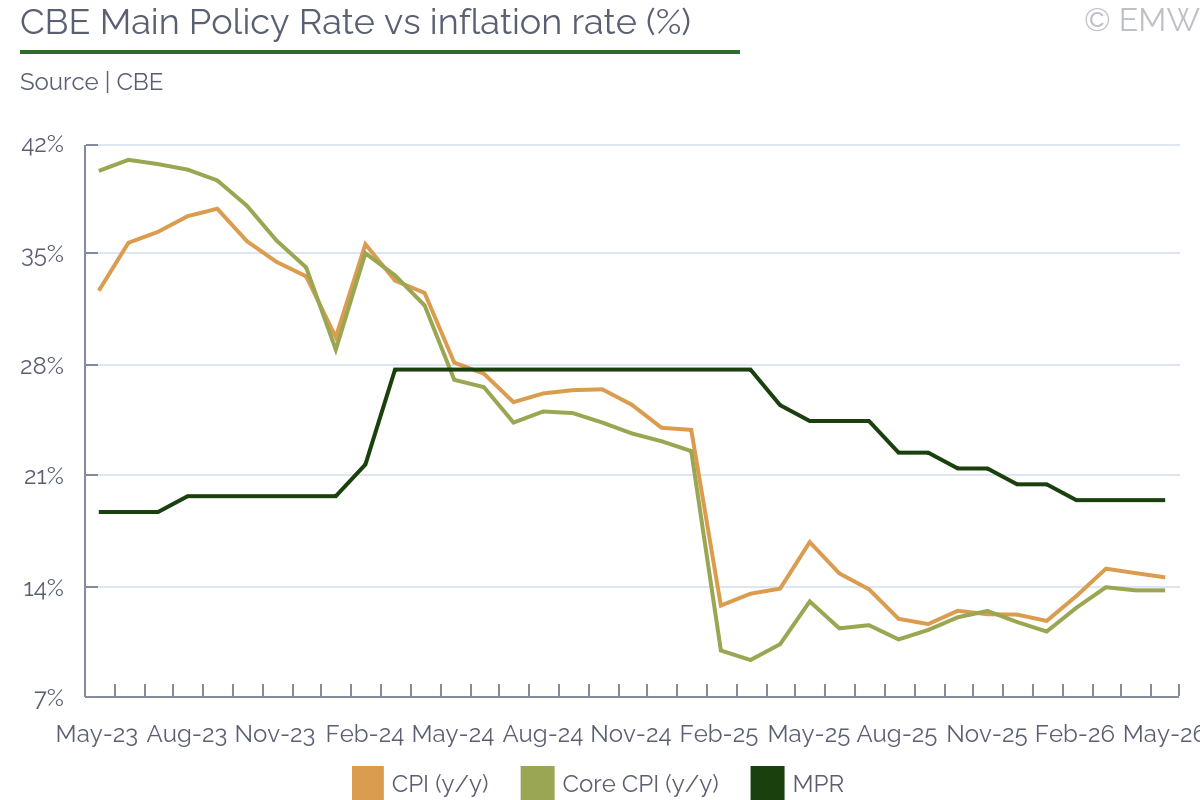

| MPC likely to hold interest rates in Jul despite US-Iran deal, slowing inflation |

- Next MPC meeting: July 9, 2026

- Current policy rate: 19.5%

- EmergingMarketWatch forecast: 19.5%

The MPC will hold an interest rate meeting on July 9, and we think the committee will keep interest rates on hold despite better-than-expected CPI print in May and the progress in US-Iran peace talks. Further, the pound has strengthened in recent days, reaching its strongest value since March. While all these factors could support a resumption in the monetary easing cycle, we think the MPC will remain cautious and hold the rates as supply-side inflationary risks remain elevated. The central bank has recently revised upwards its inflation forecasts for the medium term because of the Middle East conflict, as Egypt is vulnerable to supply line disruptions, gas imports, and investor sentiments. CBE expects annual inflation to average 16-17% y/y in 2026 - thus exceeding the 7% +/- target for Q4 2026 - before moderating to 12-13% in 2027 and eventually moderating to single digits during H2 2027.

Overall, despite more than three months of heightened uncertainty, Egypt appears stable and resilient to the regional crisis. This was not the first time CBE was confronted with capital flight triggered by major external shock. In fact, this is the third such shock in a year, and CBE's track record has been robust. Importantly, the CBE has refrained from intervening in the FX market to shore up the pound - which is now only 3% weaker than pre-war levels - consistent with its commitment to a flexible FX regime and the broader policy framework agreed with the IMF.

| Ask the editor | Back to contents |

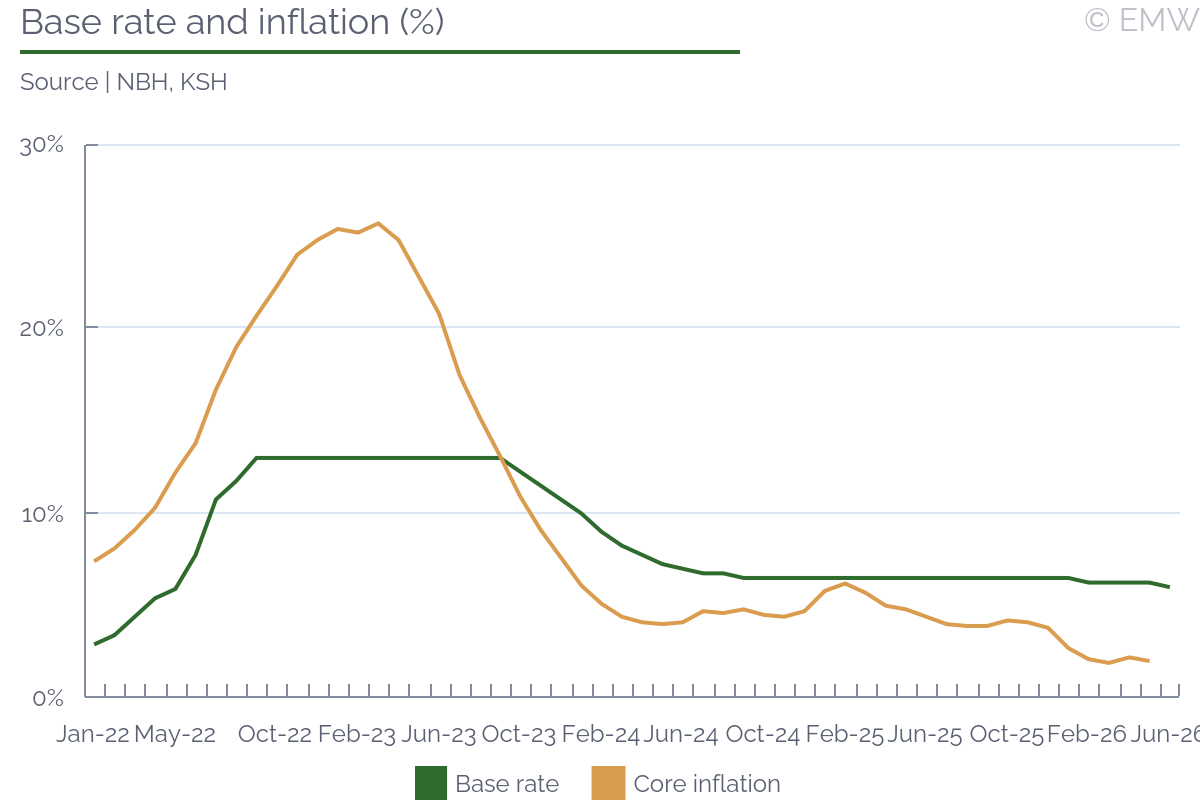

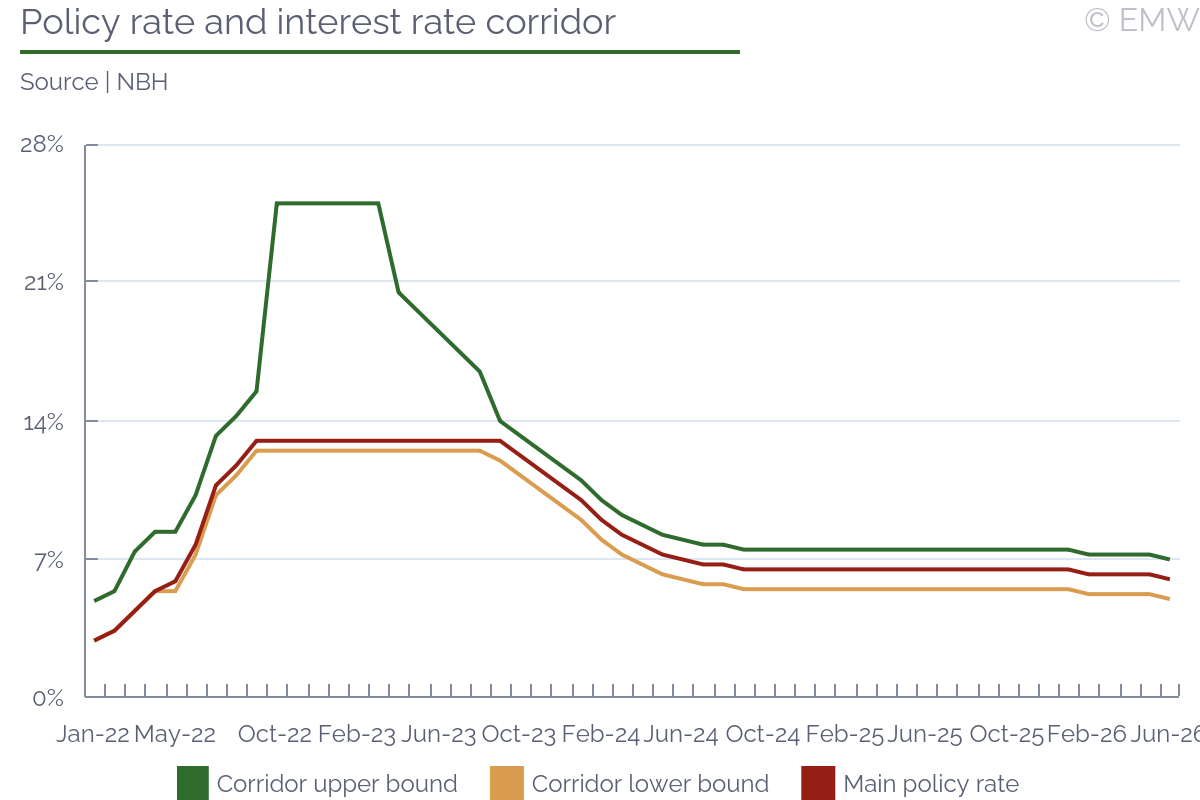

| MPC clearly shifts into rate-cut mode, cycle to be re-considered in September |

- Next MPC meeting: Jul 21, 2026

- Current policy rate: 6.00%

- EmergingMarketWatch forecast: 25bps rate cut

- Rationale: NBH governor Varga explicitly flags further rate cuts in Jul-Aug

The outlook for the summer months has certainly crystalised in favour of two more 25bps rate cuts. The MPC resumed policy easing with a 25bps rate cut in June, citing favourable inflation and financial market development. NBH governor Mihaly Varga explicitly signalled that the NBH expected the rate cuts to continue in the summer months, in case the favourable developments continue. The baseline scenario should be called a mini-rate cut cycle, since the easing stance will be reviewed in September when the NBH will update its macroeconomic projections, Varga underlined. The monetary policy guidance from the June rate-setting meeting also echoed the continued tilt towards further easing of rate conditions, as the MPC highlighted the room for interest rate cuts during the summer conditional on sustained favourable developments. Interestingly, Varga revealed that the MPC 25bps rate cut in June was not a unanimous decision. The MPC voted for a hold in May, with the vote of Peter Gottfried in favour of a 25bps rate cut, we remind. The lack of unanimity in June could suggest that some members remained in favour of a hold, while another possibility could be that some MPC members had proposed a stronger 50bps cut. The minutes from the meeting will be published on Jul 8 and should provide insight as to the easing propensity among the individual MPC members.

The improvement in the inflation outlook was a definite factor behind the rate cut decision in June. The NBH reduced its inflation forecast substantially to 1.8% for 2026 and Varga elaborated that inflation was not expected to exceed the 3.0% mid-term inflation target either in the remainder of this year or in 2027. In contrast, the NBH had previously expected headline inflation to get close to 5% in the autumn months. Varga and the MPC still underlined that the real interest rate will be kept in positive territory during the rate-cut cycle. Accordingly, the downward revision of the inflation projection had an instrumental role for the easing process, as it provided room for rate cuts while ensuring a positive real interest rate. The inflation outlook was scaled down by 2pps, in our opinion creating somewhat smaller room for rate cuts, given the pressure from expected rate hikes by leading central banks. The MPC might want to step on a slightly higher real interest rate path due to the expected tightening by major central banks, we believe, taking into account that Varga directly noted these prospects as constraining factors for easing in Hungary. The easing trend will be re-considered in September, precisely because of the limiting role of global central bank tightening, he suggested.

The loosening trend of monetary policy was supported by moderating inflationary expectations of households, Varga commented. Still, he cautioned that the durability of the decline in inflation expectations should be further assessed, so we think that inflation expectations will remain an important policy factor in the short term. The strength of the forint also supported the policy loosening stance and it has already started to have a downward impact on domestic prices, contrary to the previous months, Varga observed. Financial market stability has been helped by the NBH move to provide euro liquidity to energy importers, but the stabilisation of the global energy market allowed for this instrument to be phased out as of end-June, he noted. Financial market stability remained an important factor for anchoring inflation expectations and achieving price stability, the MPC said in June.

| MPC Members | ||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||

| Source: NBH, EmergingMarketWatch estimates |

Post-meeting MPC statement from May rate-setting meeting

Background presentation of NBH governor Varga after May rate-setting meeting

Minutes from May MPC rate meeting

| Ask the editor | Back to contents |

| RBI to hold rate in upcoming August meeting |

Next MPC Meeting: August 3-5, 2026

Current Policy Rate: 5.25%

Last decision: Hold (June 5, 2026)

Our forecast: Hold

Rationale: Inflation remains contained, although risks are tilted to the upside. RBI will look through global energy supply shock in near-term to sustain growth momentum.

We expect the Reserve Bank of India (RBI) to keep the repo rate unchanged at 5.25% at its upcoming August policy meeting. The MPC's 61st meeting, held from June 3 to 5, delivered a unanimous hold, the third consecutive pause, which in our view marks the effective end of the rate-cutting cycle, during which the RBI delivered cumulative cuts of 125bps between February and December 2025. While inflation has remained contained so far, it is set to pick up sharply as fuel price hikes already underway feed through to consumers. Retail prices for petrol and diesel have been raised cumulatively by 7.4% and 8.4% respectively since May, with the RBI estimating a direct impact of around 36bps on headline CPI. Higher fuel prices, coupled with rising input costs for producers, are also likely to generate second-round effects. Although this could risk de-anchoring inflation expectations, a scenario the MPC described as a "distinct possibility, warranting a close vigil", we believe the RBI may refrain from acting prematurely, as tighter policy could further hamper economic activity already strained by supply chain disruptions. The RBI continues to view the rally in global oil prices as largely supply-driven, warranting a wait-and-watch approach.

Inflation environment

CPI inflation rose to 3.9% y/y in May from 3.48% y/y in April, driven by higher fuel, food prices and rising dining-out costs following a sharp increase in commercial LPG prices. State-owned oil marketing companies (OMCs) raised fuel prices for the first time since the onset of the Iran war, with cumulative hikes of 7.4% for petrol and 8.4% for diesel, steeper than the 4.2% and 4.4% reported ahead of the April meeting. The move was widely anticipated amid mounting losses faced by fuel retailers, particularly after the conclusion of the state elections. The government typically discourages state-owned OMCs, which account for nearly 90% of the country's fuel stations, from revising pump prices in the run-up to elections. Pass-through of higher global energy prices is also now visible in commercial LPG, industrial raw materials, chemicals, and rubber and plastic products. The RBI also raised its CPI inflation projection for FY27 to 5.1%, up sharply from 4.6% in April, with Q3 the peak quarter at 5.9%, approaching the upper tolerance band, before easing to 5.4% in Q4 as the supply shock is expected to wane.

GDP growth

The RBI remains cautiously optimistic about growth, noting that the economy's underlying fundamentals are strong enough to withstand the current supply shock. In June, the central bank revised its FY27 growth projection down to 6.6% from 6.9% in April, with a quarterly profile of 6.6% in Q1, 6.3% in Q2, 6.5% in Q3, and 6.8% in Q4. Private consumption has remained resilient, and fixed investment maintained its momentum despite cost pressures. Domestic demand is expected to remain the primary driver of growth, supported by GST rationalisation, improving business confidence, lower borrowing costs, and the government's higher capital expenditure outlay. Services exports have continued to be robust, and merchandise exports recorded strong growth in April 2026, though elevated freight and insurance costs remain a drag.

However, the MPC acknowledged incipient signs of moderation in some sectors as suggested by high-frequency indicators, and warned that prolonged global supply chain disruptions, heightened volatility in global financial markets, and weather-related shocks continue to pose downside risks. A prolonged disruption, combined with rising fuel prices and tighter global financial conditions, could transform the supply shock into a broader demand-side slowdown, weighing on both private consumption and investment activity.

External sector

The Middle East crisis continues to weigh on India's external sector, with higher global oil prices inflating import bills, while heightened global risk aversion has triggered portfolio outflows and added pressure on the rupee. The goods trade deficit widened sharply by 25% y/y to USD 28.2b in May despite a record export performance, as import growth outpaced gains in both merchandise and services trade. Imports climbed 20.6% y/y to USD 73.4bn. The widening gap highlights the continued strength of domestic demand and the impact of higher commodity imports amid elevated global prices. A key driver was gold imports, which surged 60% during April-May FY27 to USD 9.0bn, reflecting strong domestic demand for the precious metal despite elevated prices.

The MPC noted that weak global demand and elevated freight and insurance costs are headwinds for merchandise exports, while the appreciation of the US dollar index amid shifting rate expectations has added to external pressures. The exchange rate has come under significant pressure, with the rupee depreciating more than 6% against the US dollar since the Iran war began in late February, hitting a record low. The RBI has intervened aggressively to support the currency, weighing on its foreign exchange reserves, though the Governor described reserves as providing a "sufficient buffer against external shocks." The RBI reiterated that its exchange rate policy remains unchanged and that it does not target any specific level or band for the rupee.

Last month, PM Narendra Modi urged citizens to reduce fuel and cooking oil consumption, defer gold purchases, shift to work-from-home arrangements, and avoid foreign travel to conserve foreign exchange. Subsequently, the government raised import tariffs on gold and silver and restricted silver imports to curb outward flows. Overall, the current account deficit is expected to widen in FY27, primarily due to a deterioration in the goods trade balance as imports surge.

Conclusion

While the West Asia crisis persists and risks to inflation have increased, we expect the RBI to remain on hold in August to avoid stifling growth through pre-emptive tightening. The MPC's unanimous decision to pause reflects a judgment that passthrough to domestic prices remains limited and that the supply shock is expected to wane in Q4, buying the committee time to assess whether second-round effects are becoming entrenched. The MPC's retention of the neutral stance signals an intent to retain flexibility, allowing it to adjust policy rates depending on evolving global conditions. Governor Sanjay Malhotra has previously hinted at monetary policy intervention if price pressures become entrenched. With the south-west monsoon now forecast to be deficient, risks to food prices are also mounting. In such a scenario, especially if global oil prices remain elevated for an extended period, the RBI could be prompted to raise policy rates in the second half of 2026.

Further Readings

| Ask the editor | Back to contents |

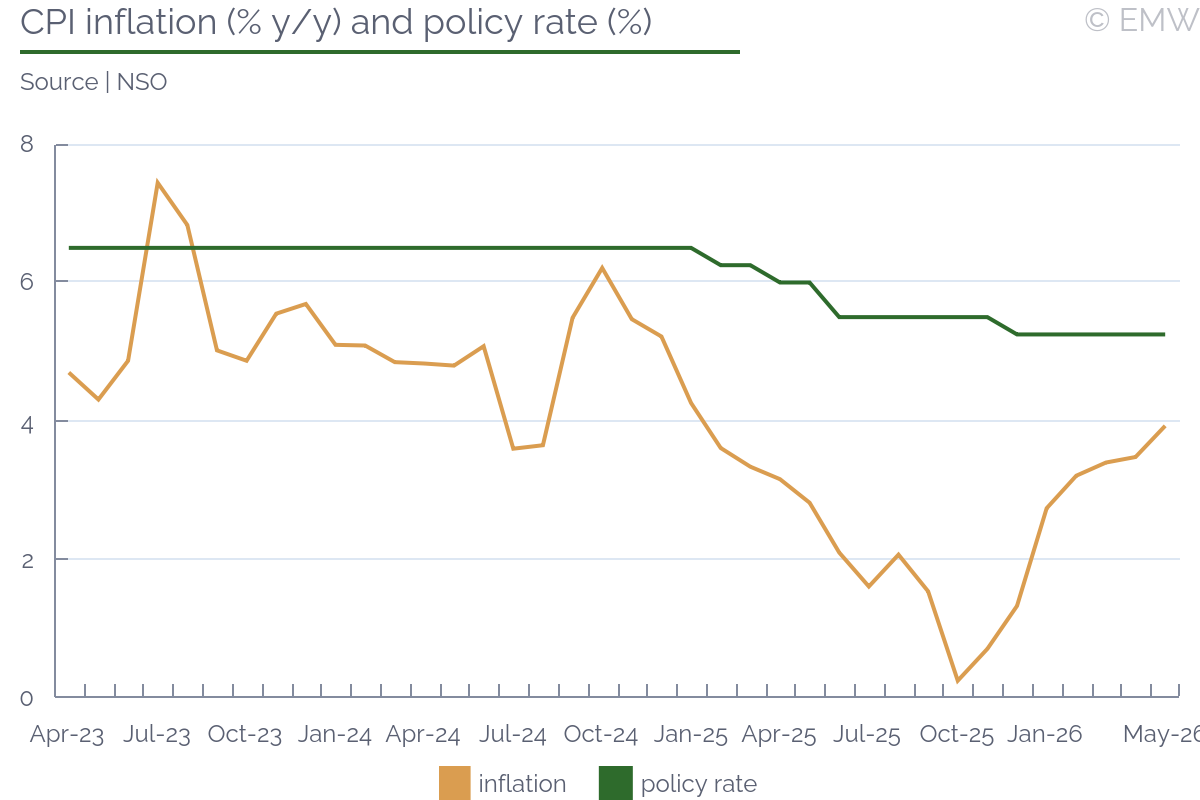

| Bank Indonesia to stand pat after 100bps cumulative rate hikes |

- Next policy meeting: Jul 21-22

- Current policy rate: 5.75%

- Our forecast: Hold

- Last decision: Raise, 25bps (Jun 17-18)

- Rationale: After 100bps rate hikes, BI will keep rate on hold to evaluate impact of hikes

We expect Bank Indonesia to stand pat at its next MPC meeting on Jul 21-22, after its 100bps cumulative rate hikes in the last couple of months. BI managed to surprise markets twice - once with the rate hike in May and then with the off-cycle meeting in June, while the latest rate hike was largely anticipated. This suggests that the market has already factored in the rate hikes, with another one down the road likely to take markets by surprise.

Moreover, the rupiah seems to have stabilised up until Jun 22, only resuming its downward trend in the week starting Jun 23. Should the latter sustain further, we may see BI become hawkish if the rupiah surpasses the USD/IDR 18,000 threshold again and consolidates there. We remind that the off-cycle rate hike came when the rupiah traded at slightly above the aforementioned threshold.

The last three decisions suggest that BI is now more concerned with the exchange rate, rather than economic growth, as CPI inflation remains broadly within its target band. This is no surprise, given the government's ambitious public spending programme, which should support GDP growth on its own.

GDP growth

GDP growth accelerated to 5.61% y/y in Q1 2026 from 5.39% y/y in Q4 2025. Government spending was by far the main factor behind the acceleration in GDP growth, while private consumption is also on a solid growth trend. The BI has maintained its GDP growth forecast at 4.9-5.7%, remaining on the optimistic side.

We should note that the government will continue to boost public spending in H1 2026 to support GDP growth, extending further the trend that started in H2 2025. The measures include speeding up the free lunch programme (MBG), as well as rolling over the placement of IDR 200tn government funds from the surplus budget balance (previously kept with the central bank) into commercial banks in a bid to boost lending. On a related note, those funds, coming from the excess budget balance, could also be used as part of the government's bond buyback programme, which aims to stabilise bond prices.

Exchange rate stability

The rupiah has depreciated by about 7.7% against the USD since the beginning of the year, making it one of the worst-performing EM currencies globally. It stabilised shortly after the off-cycle rate hike, before resuming its downward trend, which led to the latest 25bp rate hike. The latter was followed by a brief period of stability, but the rupiah again started depreciating in the week starting Jun 22.

As a result, so far the BI's measures seem to have only a marginal effect on the rupiah's exchange rate. We should note that apart from the rate hike, BI regularly carries out its so-called triple intervention, which includes purchases on the spot FX market, domestic non-deliverable forwards (DNDF) and buying government bonds on the secondary market. BI also increased coordination with the government, with the government also started bond buybacks on the secondary market to boost FPI inflows.

The central bank also introduced a multitude of other measures aimed at stabilising the rupiah, such as reducing the FX purchase limit from USD 100,000 in the beginning of the year to USD 10,000 from Jul 1. In addition, it also raised the cap on banks' foreign funding portfolio to 40% from 35% previously, aiming to attract more FX inflows.

Concerns over the Fed's policy course have also diminished, with pressure on the rupiah now the main topic. Still, should the Fed tighten monetary policy, this will exert further pressure on the Indonesian rupiah, possibly prompting BI to follow course.

Inflation environment

CPI inflation accelerated to 3.08% y/y in May, up from 2.42% y/y in April, though it still remains within BI's 2.5+/-1% target band. The BI justified the latest rate hikes also as a pre-emptive move to curb inflation. Still, CPI inflation is mainly driven by food prices, which reflect both the rupiah's depreciation, as well as second-round effects from the oil price spike following the US-Iran war. Core inflation remains close to the midpoint of the BI's target band at 2.59% y/y in May.

Looking forward, the outlook for June remains benign as the government kept subsidised fuel prices flat, carrying the burden from the oil price spike. The two successive rate hikes will help curb inflationary expectations, while another hike would also further tame the inflationary outlook. The central bank expressed confidence that CPI inflation will remain under control and within the target band in 2026.

As a result, we think CPI inflation has largely taken a backseat in Bank Indonesia's monetary policy meetings.

Conclusion

Looking forward, we expect BI to remain vigilant about the mounting pressure on the rupiah. We expect it will want to surprise markets again, though not at this point, given that the latest rate hike was largely anticipated. As a result, we think BI will stand pat in July, evaluating the impact of the latest series of rate hikes, with possibly further tightening set for August or September if the rupiah continues its downward trend.

Further reading

| Ask the editor | Back to contents |

| Inflation slows in May, June H1, but no monetary easing should follow |

- Next MPC meeting: June 25

- Current policy rate: 6.50%

- EmergingMarketWatch forecast: Hold

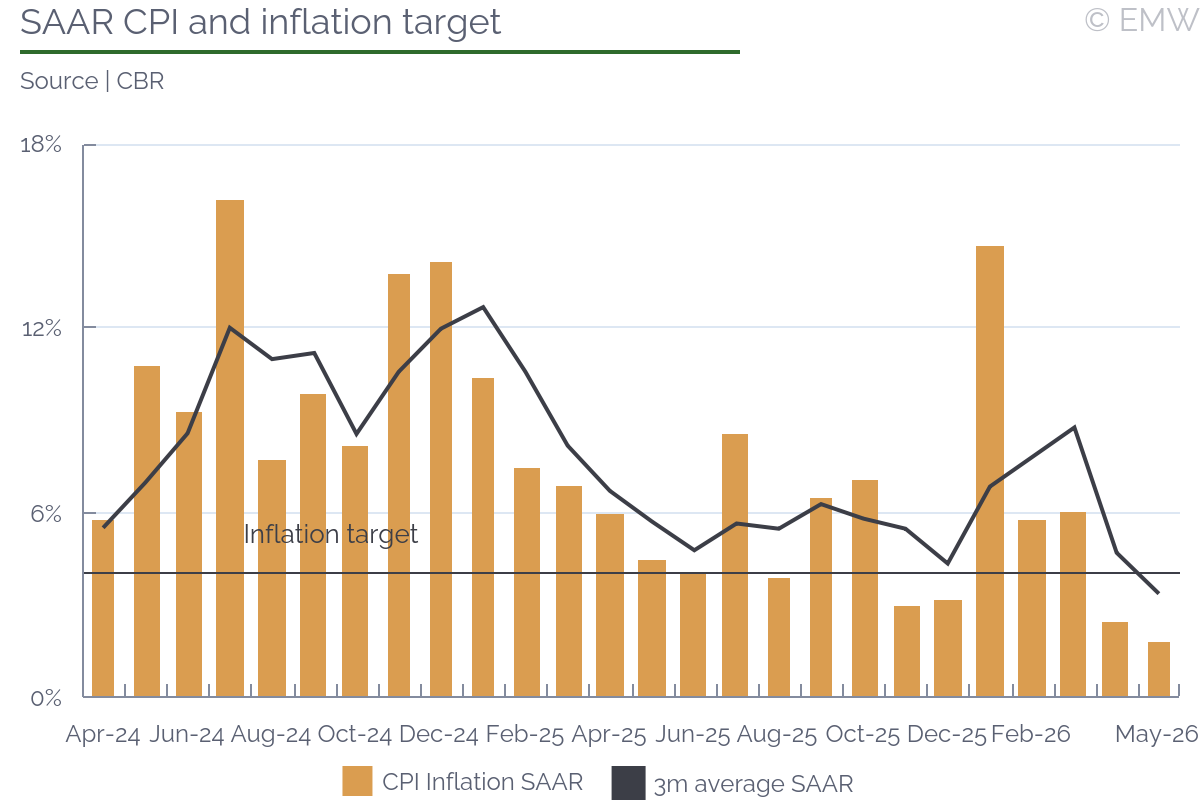

CPI inflation continued to slow in June H1 after a better-than-expected performance in May. This brought general inflation down to 3.55% y/y by the end of the fortnight, seemingly converging to the CB's 3.00% target, down by 0.98pps over the last four fortnights. However, we warn the deceleration has come mostly on the back of non-core inflation, with core inflation remaining above 4.00% and slowing by only 0.15pps over the same span.

Indeed, core inflation shows general inflation is on no path to converge to the CB's 3.00% general inflation target, considering core inflation now adds 26 consecutive fortnights above 4.00% y/y. The pace of service prices is particularly concerning, standing at 4.57% y/y in June H1 and accelerating by 0.13pps in the four-fortnight span discussed.

The service inflation stubbornness comes across the board, in our view, including in housing and education prices. We believe this pressure might be explained by lingering upward pressure on prices from the pace of real wages, including the constant revisions of the minimum wage. Indeed, while the economy has lost momentum and seemed at risk of entering a recession in H1, unemployment remains resilient and real wages continue to improve, pressuring service prices and weakening the competitiveness of the industrial sector, in our view.

With this all, the CB is in no position to cut its Monetary Policy Rate (MPR) anytime soon, in our view. Indeed, the market does not expect any easing soon. In fact, recent polling shows the market expects the CB will keep its MPR at 6.50% throughout 2026 and 2027.

We insist the CB might not be as responsible as the market seems to believe, considering it proved to be very dovish in recent sittings, even since late 2025, cutting its policy rate swiftly even as inflation showed no convergence to its punctual target. This rapid easing, along with unrealistic mid-term inflation forecasts, have weakened the credibility of the monetary policymaker, in our view and in the opinion of some analysts. However, holding the policy rate steady through the long run, even as CPI inflation has positive periods, should help to partially rebuild this credibility.

In our view, the CB's credibility will depend much on who President Claudia Sheinbaum appoints to join the board next year, taking the seat of Deputy Governor Jonathan Heath, considering Heath has been the lone hawkish voice in a dovish Monetary Policy Council (MPC).

We continue to assume the president will select a candidate with the right credentials, probably someone respected from within the CB itself. However, we'd like to see her to replace the outside role played by Heath by picking someone more respected and linked to the private sector. In any case, selecting a new loyalist, as we see Governor Victoria Rodríguez and Deputy Governor Omar Mejía, would significantly weaken the CB's credibility, in our view.

All in all, we remain absolutely confident the CB will hold its Monetary Policy Rate (MPR) at 6.50% in its June sitting. The Monetary Policy Council (MPC) was as clear as possible in the lastest quarterly report presentation, saying the easing cycle has ended with the monetary policy firmly in neutral territory. The insistence that the easing cycle has ended is no surprise, matching the board's stance made in the May sitting,

It's evident the CB does not expect to alter its Monetary Policy Rate (MPR) in the coming months. This should at least cover the next three sittings, in our view, scheduled for June, August and September. As mentioned, the market anticipates this stability will extend further, with 90% of the analysts polled by the CB expecting the policy rate to stand as is until Q1 2027. This consensus wanes thereafter but remains relatively strong, with 77% of analysts anticipating stability by Q4 2027, according to Banxico's latest poll among analysts.

We believe stability throughout 2026 and 2027 might be warranted, given lingering inflationary pressures. However, the dovish position assumed by the bulk of the board through this easing cycle makes us question if the CB will not be looking to trim its policy rate earlier than expected, particularly if the economy disappoints further.

Overall, we expect the board will hold the policy rate at 6.50% through the rest of the year, hoping for core inflation to slow while it does so. We assume the dovish majority would like to clip the policy rate further in 2027; however, it remains to be seen if they'll do so even if CPI inflation, as expected, shows no clear convergence towards the CB's 3.00% target. Indeed, late 2026 comments and the pace of CPI inflation to close the year might increase the chances of easing next year. Currently, the market expects monetary policy stability through the rest of 2026 and through 2027, something that might not recognize how dovish the board is.

| Monetary Policy Council members | ||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||

| Note: Overall bias calculated from voting behavior and comments | ||||||||||||||||||||||||||||||

| Source: Banxico |

| Ask the editor | Back to contents |

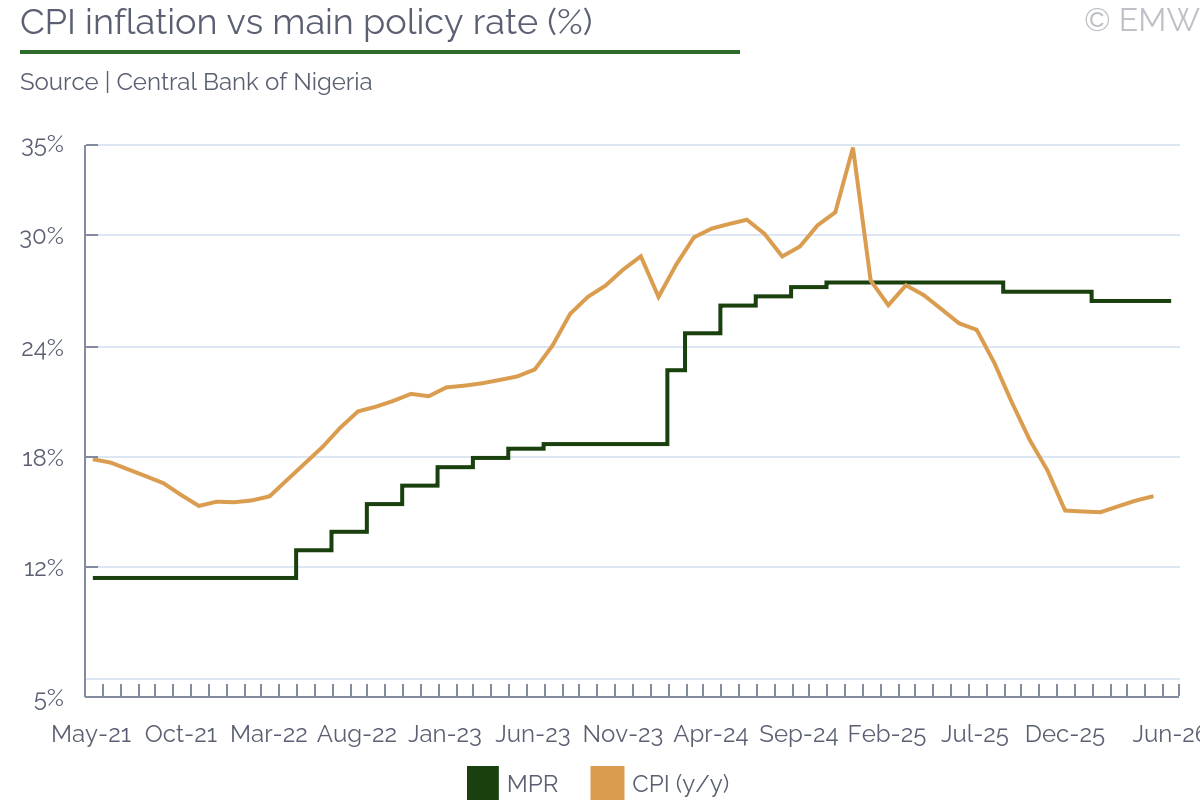

| MPC to hold policy rate in July to allow for return to disinflation |

- Next MPC meeting: 20-21 July

- Current policy rate: 26.5%

- EmergingMarketWatch forecast: 26.5%

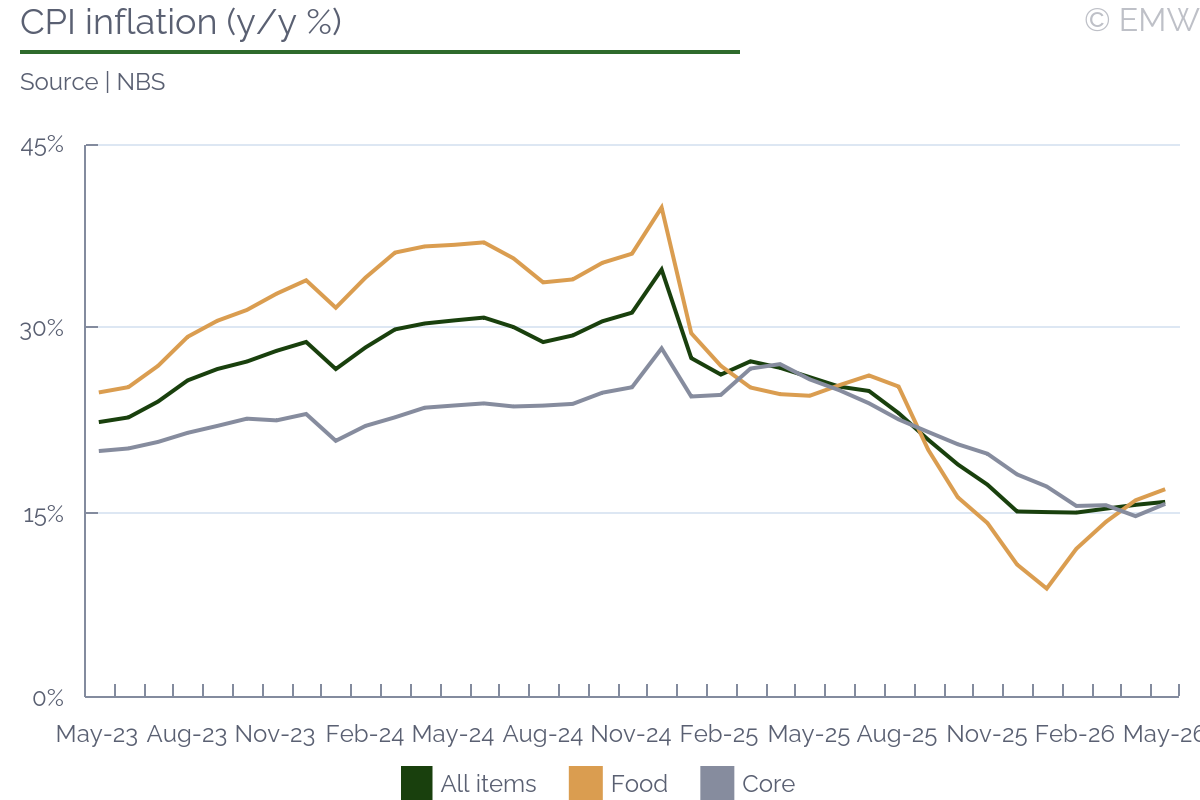

At its last meeting in May, the MPC decided unanimously to maintain the monetary policy rate at 26.5%. This was as higher energy prices fed into inflation during March and April. The most recent data from the statistics office shows inflation rising for the third consecutive month in May, reaching 15.9% y/y from 15.7% y/y in April. CBN governor Olayemi Cardoso has said the moderate rise in inflation is temporary and primarily driven by external shocks linked to the Middle East. The MPC will next meet on 20-21 July, a week after the statistics office releases its June inflation report. The inflation outlook may improve now that the US and Iran have agreed to extend an interim peace deal and reopen the Strait of Hormuz, but we still anticipate another rate hold in July. Even if June inflation moderates slightly, we expect the MPC to remain cautious and assess whether inflationary pressure is truly easing for multiple months before implementing rate cuts.

Local economists at Cowry Asset Management expect Nigeria's headline inflation rate to ease slightly to 15.8% y/y in June, supported by improving food supply conditions and lower global crude oil prices. However, they warn that risks remain in the form of elevated core inflation, high transportation costs, weather-related disruptions to agricultural production and potential exchange-rate volatility. As of May, both food inflation (17% y/y) and imported food inflation (14.7% y/y) have risen for four straight months, as per the statistics office. Transport prices were also up, by 17.1% y/y in May following a 16% y/y increase in April. In its recent Article IV report, the IMF indicated that it expects disinflation to resume in the second half of the year. The IMF advised the CBN to keep monetary policy tight and data-dependent for longer. Given this advice and Cardoso's continued guarded messaging, we expect the CBN to keep the policy rate unchanged at 26.5%.

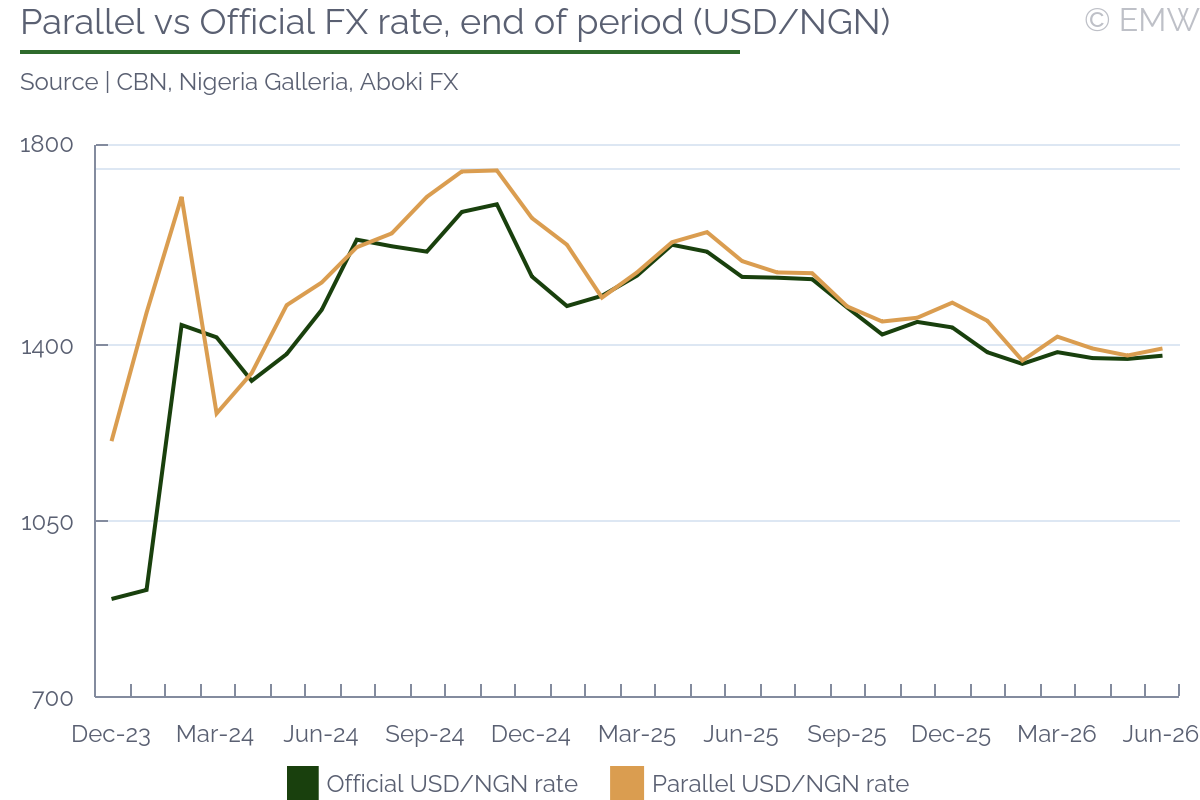

Beyond interest rates, the CBN has also continued to support price stability through FX and liquidity management. The bank launched the latest Foreign Exchange Manual in June which aims to deepen market liquidity and reduce arbitrage opportunities. The bank also intensified liquidity tightening through aggressive OMO, mopping up over NGN 1.69tn in a single auction in early June to reduce excess liquidity in the system. The naira is mildly stronger in June on the official market, reaching USD/NGN 1,370 on June 23 compared to NGN 1,375 at the end of May. However, the currency is noticeably weaker and less stable on the parallel market (NGN 1,395 versus NGN 1,380 on the same dates). Members of the MPC have expressed confidence that the strengthening reserve position will support exchange-rate stability. As of June 19, Nigeria's external reserves rose to USD 51.06bn from USD 49.58bn at the end of May (surpassing the CBN's year-end target of USD 51.04bn). Analysts expect continued reserve accumulation going forward driven by higher oil export inflows and more foreign capital inflows.

Monetary Policy Committee Statement

Monetary Policy Committee Meeting Schedule

| MPC vote by members (bps) | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Source: CBN |

| Ask the editor | Back to contents |

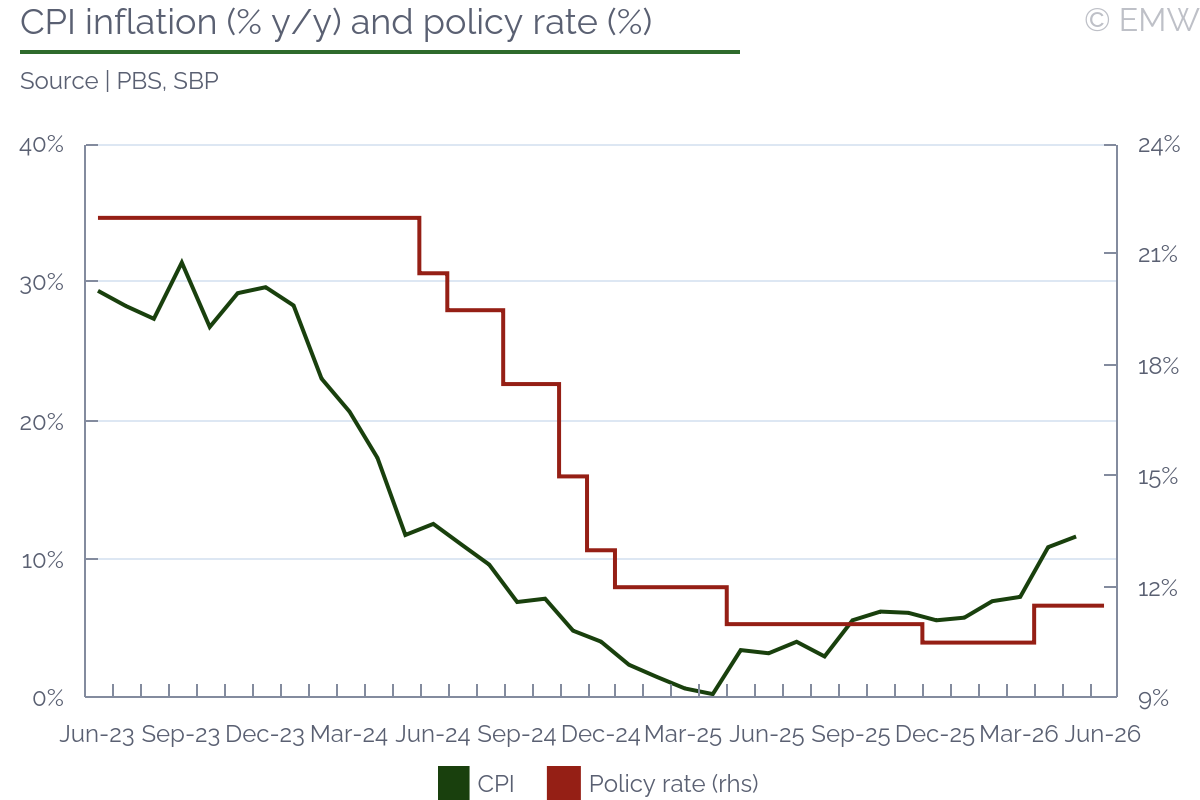

| SBP likely to hold policy rate for extended period |

Next policy meeting: Yet to be announced

- Current policy rate: 11.50%

- Last decision: Hold (June 15, 2026)

- Our forecast: Hold

- Rationale: Slightly favourable inflation outlook and external sector stability support a status quo. SBP sees current stance as appropriate to achieve its inflation target

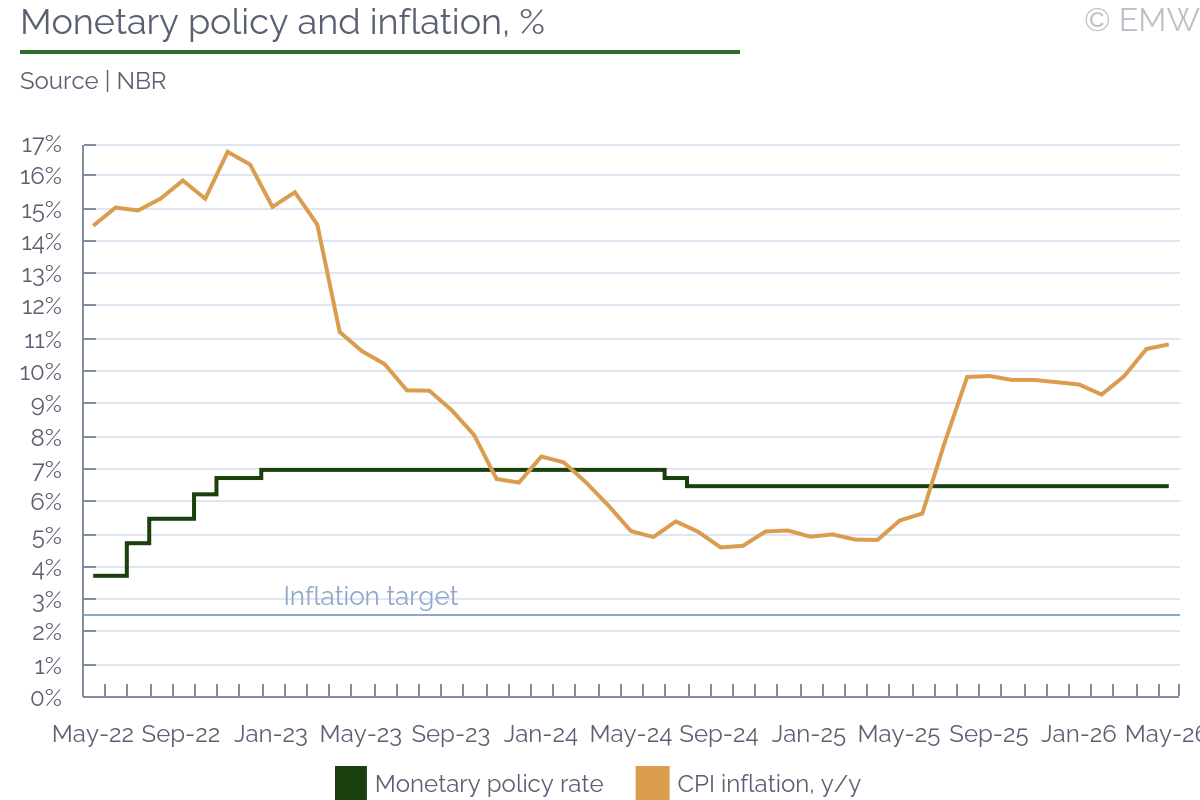

The State Bank of Pakistan (SBP) kept its benchmark interest rate unchanged at 11.50% in a policy meeting on June 15. The decision reflects the central bank's optimism regarding the inflation trajectory and external position amid the easing of geopolitical tensions. The recent inflation outturns did not prompt a rate hike action from the SBP, as had been predicted by 17 of 39 economists polled by Bloomberg (the remaining forecast a hold). The CPI in May hit 11.7% y/y, the highest since June 2024 and pushed the real policy rate on a spot basis into negative territory for the first time in more than two years. This is inconsistent with the IMF's guidance under the Extended Fund Facility, which urges for maintaining an appropriately tight monetary policy. However, the SBP seems to have taken a forward-looking approach, with its (possibly favourable) year-ahead inflation outlook likely guiding the latest rate decision. While the SBP did not provide an inflation forecast, the government sees inflation to average 8.2% while the IMF projects 8.4% in the next fiscal year.

Inflation environment

CPI inflation accelerated to 11.7% y/y in May from 10.9% y/y in April, remaining well above the SBP's 5%-7% target range. The increase was driven mainly by higher fuel, electricity, gas, and transport service prices. Core inflation also firmed, rising from 8.0% y/y in April to 9.0% y/y in May in urban areas. The SBP projected inflation to remain in double-digits over the next few months before gradually easing subsequently. In a sign that the central bank has become somewhat more upbeat about the inflation outlook, the latest policy statement omitted the comment (included in the previous two statements) that inflation is expected to remain above the upper bound of the target for most of FY27.

GDP growth

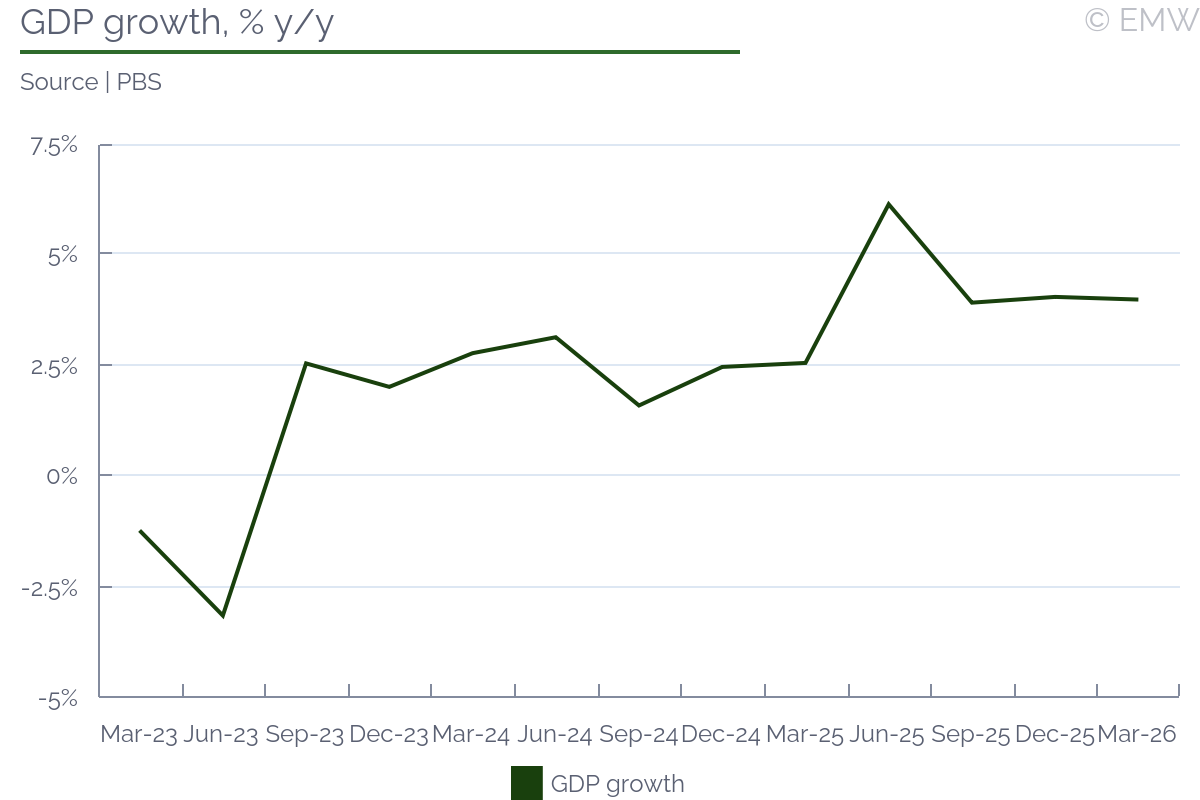

The economy is estimated to have expanded by 3.7% y/y in FY26, up from 3.2% y/y in FY26, as domestic demand strengthened amid easing financial conditions, strong remittance inflows, and relatively muted inflation. After posting a robust recovery in the first three quarters (July-March), when growth clocked in at 3.99% y/y, economic activity showed some signs of moderation in the final quarter. The SBP noted that the slowdown reflected the impact of elevated prices, austerity measures and prevalent economic uncertainty, adding that the pre-conflict growth momentum was notably higher. For FY27, the government forecast GDP growth to pick up to 4.0%. The SBP is likely to release its forecast in the next policy meeting.

External sector

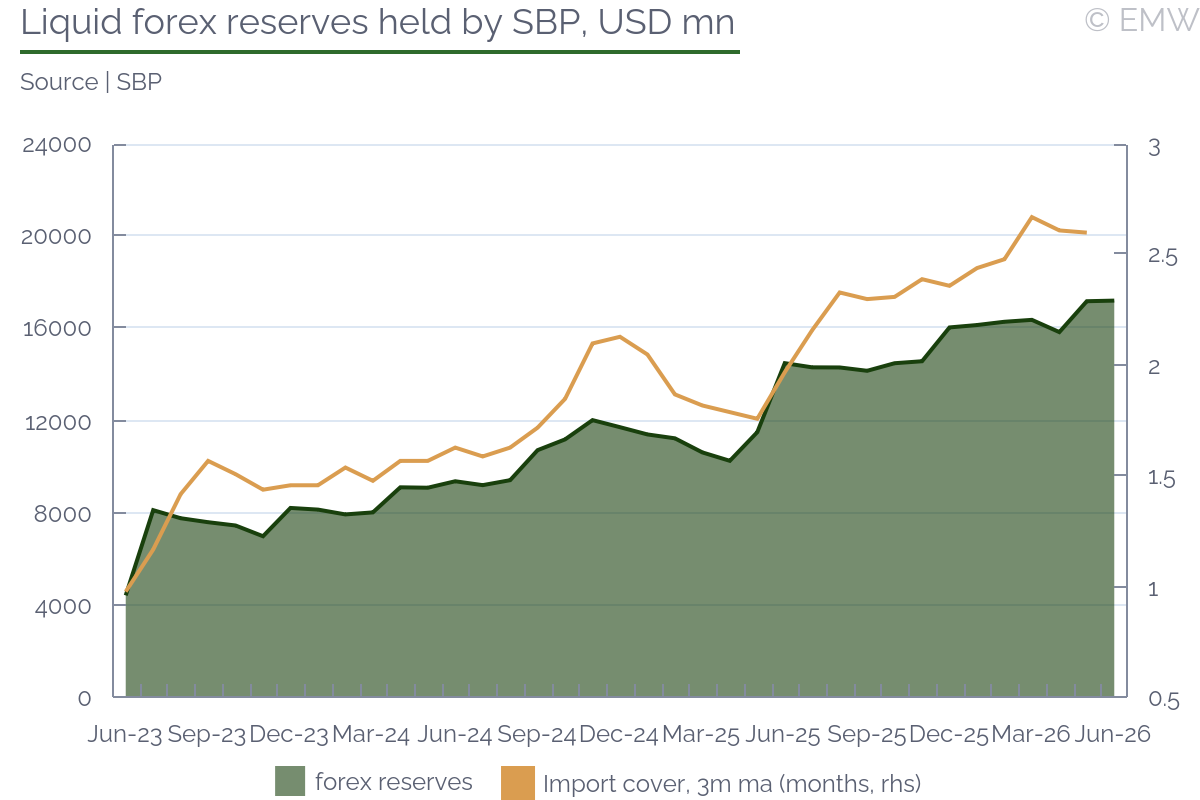

The current account swung back into surplus in May, reaching USD 459mn following a USD 276mn deficit in April, supported primarily by strong workers' remittances, robust services exports, and a decline in non-oil goods imports. The SBP expressed comfort with the external sector, noting that pressures remain moderate. However, elevated energy imports, which, although eased slightly amid softer global oil prices, continued to weigh on the current account. The goods trade deficit rose by 8.5% y/y to USD 3.32bn, also partly driven by weak exports, mainly food and textiles. The central bank maintained its current account deficit forecast for FY26, projecting it closer to 0% of GDP. Further, healthy loan inflows and SBP's continued foreign currency purchases from the interbank market are expected to increase foreign exchange reserves to USD 18bn by the end of June, from USD 17.2bn as of June 5, providing 2.7 months of import cover. The SBP projected the current account deficit to widen in FY27.

Conclusion

In a subtle forward guidance, the SBP noted that the current monetary policy stance remains appropriate to bring inflation down toward its 5%-7% target range over the medium term. The IMF projects inflation at 7% by June 2027. Barring another supply shock stemming from a breakdown of the US-Iran peace deal, we expect the central bank to hold its policy rate in the near-term. The 100bps rate hike in April now appears to be a one-off move.

Further Readings

| Ask the editor | Back to contents |

| BSP likely to raise policy rate on Aug 27 |

- Next monetary policy meeting: Aug 27

- Current policy rate: 4.75%

- EmergingMarketWatch forecast: Hike by 25bps or 50bps

- Rationale: Monetary Board statement of Jun 18; comments by Governor Remolona; peso weakness

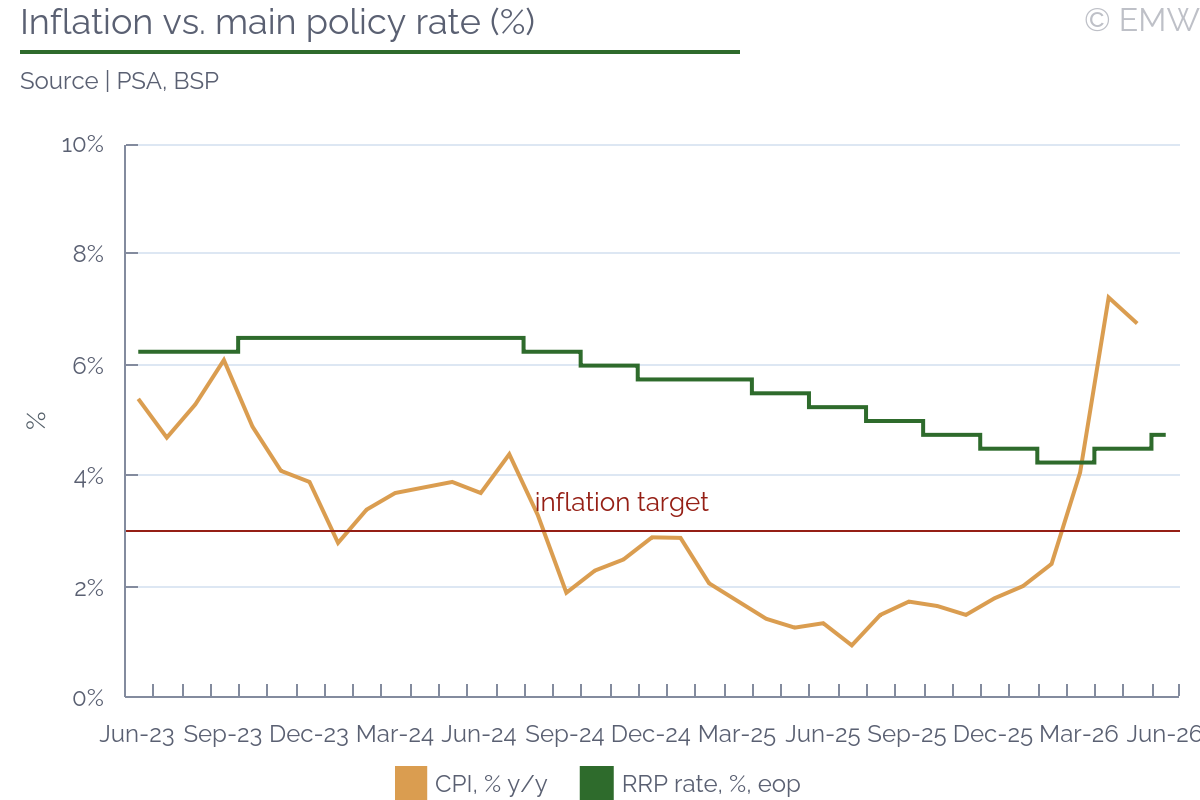

We think that BSP's Monetary Board (MB) will likely raise the policy interest rate by 25bps or 50bps in its meeting on Aug 27. On Thursday, the MB decided to increase the BSP's Target Reverse Repurchase (RRP) Rate by 25bps to 4.75%. The decision was in line with expectations. It was the second consecutive rate hike. The MB cited persisting strong inflationary pressures.

Domestic fuel and food prices continue to be driven by persistently high global oil and fertiliser prices. The increase in core inflation signals that price pressures are broadening and that second‑round effects, such as higher inflation expectations, are emerging.

The central bank's latest forecast is of a higher inflation trajectory. Average headline inflation is projected to exceed the upper end of the 3±1% tolerance range both this year and next year. Inflation is expected to be slightly above the 3.0% target in 2028.

All in all, the MB's decision was that tightening monetary policy is warranted. The policy rate hike will help keep inflation expectations anchored and reduce the risk of second-round effects. The measured key rate increase will also complement fiscal measures in supporting steady consumption and bolstering business sentiment.

The MB will remain guided by incoming data and stands ready to act as needed to ensure that inflation returns to the 3.0% target, the press release concluded.

Following the MB meeting on Thursday, BSP governor Eli M. Remolona Jr. told a press conference that the BSP will consider a 25bp rate hike in August. The central bank has a lot of space to tighten monetary policy, while it may be inclined to take "baby steps" going forward, he added. According to him, a 50bp hike is also an option depending on the data, but large rate moves tend to disturb the markets if reversed. The anchoring of inflation is "not a big issue" for now, he noted. He also said that the central bank could have an off-cycle meeting at any point. The BSP hopes that its decision not to be aggressive in tightening will help the economy somewhat, the governor said.

Inflation

The BSP's new inflation forecast is 6.4% this year and 4.5% next year. The central bank's previous projections were 6.3% and 4.3%, respectively. Headline inflation is predicted to be 3.1% in 2028. The inflation target range is 3±1%.

CPI inflation slowed down to 6.8% y/y in May from 7.2% y/y in April. The CPI rose by 4.5% y/y in Jan-May. Annual core inflation was 4.1% in May, speeding up from 3.9% in April. The seasonally adjusted CPI fell by 0.6% m/m in May, after rising by 3.0% m/m in April. The CPI inflation in May was below BSP's month-ahead forecast range of 7.1-7.9% y/y.

Economic growth

The Philippine government projects economic growth in the range of 3.5-4.5% this year, down from an already reduced forecast of 5.0-6.0%, economic planning secretary Arsenio Balisacan told a local broadcaster on Monday. The Philippine economy expanded by 4.4% in 2025.

The WB cut its GDP growth forecast to 3.7% in 2026, down from 5.3% forecasted in January, according to the Global Economic Outlook released in June. Looking forward, the economy will rebound by 5.6% in 2027 and 2028.

The OECD cut its GDP growth forecast for the Philippines to 3.2% in 2026, down from 5.1% predicted in Dec 2025, according to the latest OECD Economic Outlook released in early June. The growth projection for 2027 was revised down as well, to 5.0% from 5.8%.

LFS, credit growth

The unemployment rate decreased to 4.7% in April from 5.0% in March, but it was higher than 4.1% in Apr 2025, according to the results of the latest labour force survey (LFS). In the y/y comparison, the number of unemployed rose by 17.0% y/y to 2.41mn in April. The number of employed climbed 0.4% y/y to 48.89mn. The labour force hence increased by 1.1% y/y to 51.30mn.

Outstanding loans of universal and commercial banks, net of reverse repurchase (RRP) placements with the BSP, rose by 11.4% y/y at end-April, speeding up from 10.7% y/y growth at end-March, the BSP said. On a seasonally adjusted basis, loans increased by 1.1% m/m at end-April.

Exchange rate

The peso is trading at USD/PHP 61.402 at the time of writing, which compares with USD/PHP 60.595 on Jun 18, the date of the latest MB meeting.

The weakness of the Philippine currency is an important argument supporting our expectation of continued monetary tightening, in our view.

Further reading

Press release after Jun 18 monetary policy action

Schedule of monetary policy meetings

| Ask the editor | Back to contents |

| MPC is clearly on hold for some time, cut questions arise |

- Next MPC meeting: Jul 7-8, 2026

- Current policy rate: 3.75%

- EmergingMarketWatch forecast: 3.75%

Rationale: The Monetary Policy Council has become much less hawkish and, as the chance of rate hikes this year recedes, attention turns to whether the MPC might just again be close to cutting. NBP and MPC chair Adam Glapinski started the dovish drive at his June press conference on Jun 3, saying that the MPC remained in 'wait-and-see' mode as there was no reason now to change rates or to even discuss changing them. Glapinski underscored that the inflation shock from the Middle East conflict wasn't as dangerous as that in 2022 or as bad as feared, and said that the chance of a hike had fallen after May CPI inflation came in at 3.1% y/y, down from 3.2% in April and well below the 3.6% consensus. In fact, that inflation print has motivated a raft of dovish comments from MPC members (see table below).

Most MPC members have come out in June with comments that echo the view that the chance of hikes has fallen sharply. MPC member Gabriela Maslowska, who usually follows Glapinski's line closely, said on Jun 9 that the chance of a hike had fallen while the chance of a cut had increased. Though MPC member Marcin Zarzecki sounded much more cautious on Jun 10 (saying the MPC would remain on hold or hike this year, and thus shying away from backing easing), sometimes cautious MPC member Ireneusz Dabrowski said on Jun 12 that a rate cut this year was more likely than a hike, underlining just how the rate outlook has changed in recent weeks.

MPC member Ludwik Kotecki sounded a note of caution on Jun 15, saying that it was likely rates would remain on hold through year-end and perhaps even to end-Q1 2027. But attention is now firmly on whether the MPC might just be in position to cut rates this year. This will very much depend on how the global oil price responds to the US-Iran peace deal, and indeed on whether it holds. If the oil prices return to their February levels, then there is a chance for much lower inflation this year. The outlook for inflation in 2027 and 2028 was very benign before the war and so if this reality again became the most likely, then the MPC could very well start sounding dovish.

But with so much uncertainty out there, it would not be surprising for the MPC to very cautiously move towards any chance of easing, and that probably means the likeliest policy will be a 'wait and see' one in which rates are held. The July Inflation Report, including the updated CPI and GDP projections, will be important in how they pencil in the outlook, but this report will likely be too beset by uncertainty to provide the MPC with any firm ground to change rates. More likely is that the MPC will wait till September or October to see what happens with the war, and indeed perhaps it is the subsequent November Inflation Report that will provide the pretext for rate changes, suggesting perhaps a late-year move if all is well. If not, rates will likely remain flat. And, one can't rule out a hike if the oil price should surge, say, if war returns to Iran.

| MPC breakdown | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Source: NBP |

Latest NBP inflation report (March 2026)

| Ask the editor | Back to contents |

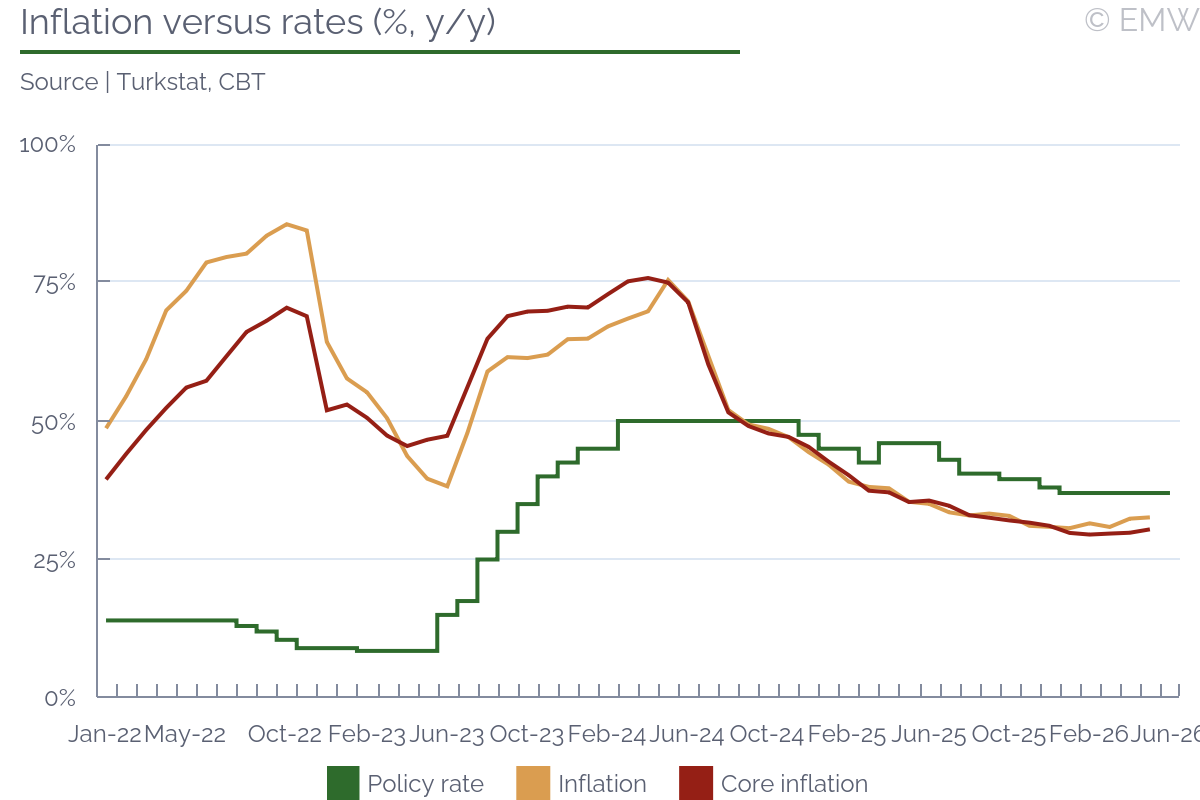

| CBT likely to hold as caution still outweighs easing signals |

- Next MPC meeting: Jul 23, 2026

- Current policy rate: 37.0%

- EmergingMarketWatch forecast: Hold

- Rationale: Better oil and tourism dynamics help, but political risk and inflation inertia keep cautious guidance necessary

We expect the CBT to leave the policy rate unchanged at 37.0% at the forthcoming MPC meeting. At its latest meeting, the MPC noted that the underlying inflation trend eased somewhat in May after the April increase, partly reflecting energy prices. Yet, it maintained a cautious tone on external risks, underlining that energy prices remained volatile and elevated amid geopolitical uncertainty. The CBT also pointed to a continued loss of momentum in economic activity in Q1, while leading indicators still suggested a weak domestic demand backdrop.

One notable change from previous statements was the absence of any reference to preliminary indicators for upcoming month's inflation, we note. The reason for this omission is not clear, in our view. It may simply have reflected the early timing of the meeting within the month or the lack of sufficiently reliable information at that stage, in our opinion. Another possibility is that preliminary indicators were pointing to a relatively benign inflation print, and the CBT preferred not to send an overly dovish signal before gaining more visibility, we think. If this was the case, tomorrow's MPC summary may provide further detail on the CBT's near-term inflation assessment, we assess.

The external backdrop turned somewhat more supportive for the CBT, although we would still treat this improvement with caution, we note. In this regard, the Iran war ceasefire and the recent subsequent fall in oil prices, if sustained, would ease pressure on inflation, the CA deficit and carry-trade sentiment, in our view. The tourism season should also provide an additional reserve buffer, even though tourist arrivals remained weaker than in previous years, we remind. These factors improve the short-term policy setting, but they do not remove the need for a cautious monetary stance, we assess.

The main domestic risk remains the political climate around CHP. We think further legal or political pressure on Ozgur Ozel, and potentially Mansur Yavas, could still create market strain, we note. For now, the available figures do not point to a major increase in local FX demand, which is supportive for the CBT's policy management. Still, political shocks can change expectations quickly, especially when reserve credibility and disinflation confidence remain closely linked, we note.

Overall, the more important issue, in our view, is not whether the CBT has enough justification to stay on hold in the upcoming meeting, but whether it can preserve the perception that policy remains deliberately tight while the easing cycle is being pushed into view. A premature dovish signal would therefore risk weakening the carry narrative before the CBT has secured enough evidence on inflation inertia, local FX behaviour and reserve accumulation, we note. This is why we think the CBT is likely to keep its communication cautious, even if near-term inflation and oil dynamics look more favourable than they did only a few weeks ago. With considerable time still left before the next MPC meeting, we will update our call as the balance between disinflation signals and political-market risks evolves.

Summary of June rate-setting meeting (to be released on Jun 18)

| Ask the editor | Back to contents |

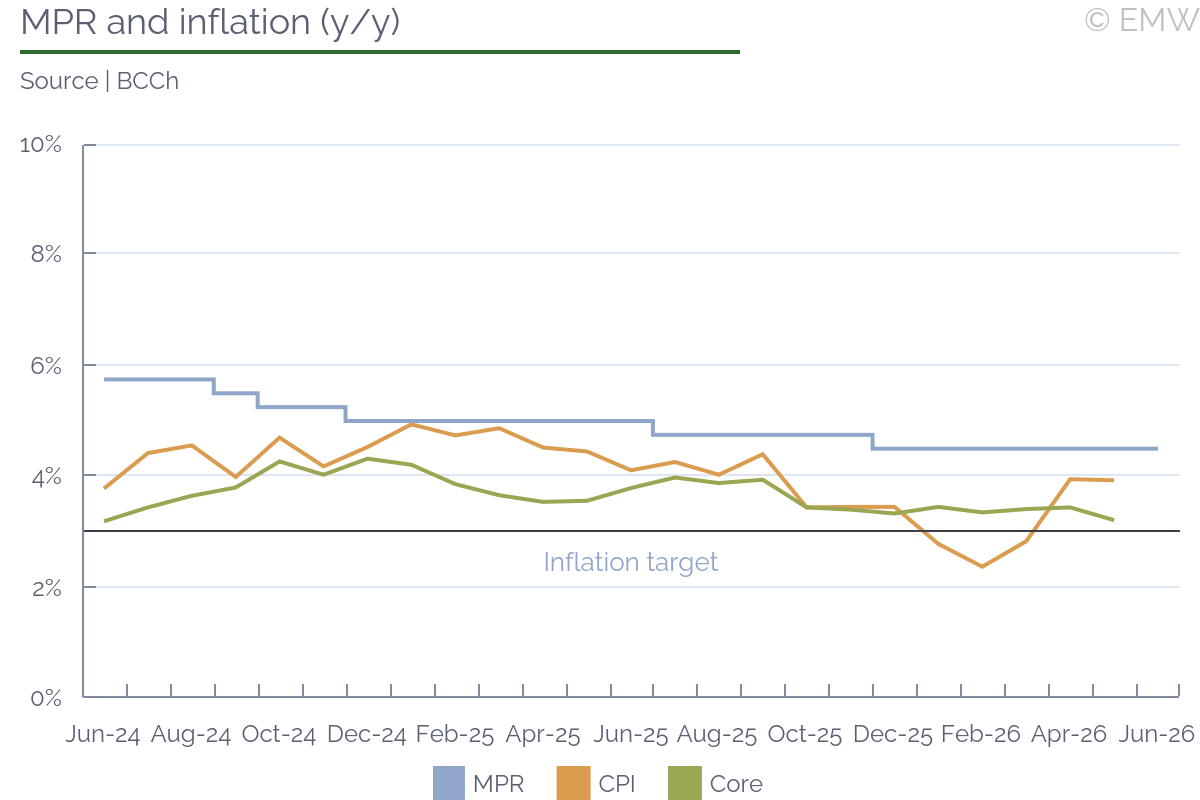

| MPC reinforces 'hold' stance as inflation risks become more balanced |

- Next MPC meeting: July 28

- Current policy rate: 4.50%

- EmergingMarketWatch forecast: 4.50%

Summary

The verbal and non-verbal guidance delivered by the Monetary Policy Council following its unanimous MPR hold at 4.50% in the Jun 16 meeting implied that the set of inflation risks became more balanced after the recent developments in the Middle East, reinforcing the idea that the benchmark rate is likely to remain on hold during this temporary period of above-target inflation. In the absence of new inflationary shocks, the central bank's baseline forecast sees inflation gradually returning to the 3.0% target by Q2 or Q3 next year. If this inflation scenario materializes and GDP growth keeps converging toward its potential level, the MPR would likely be on hold for the next 3-4 quarters, and at that point a 25bps cut that takes the MPR to its neutral level becomes an option.

However, the MPC has been emphasizing that the macroeconomic scenario is subject to a greater-than-usual degree of uncertainty, which requires a careful meeting-by-meeting review of the monetary policy stance. The BCCh's latest monetary policy corridor was symmetrical, suggesting that the probability of hikes or cuts over the next few quarters is balanced, even if a move remains unlikely in the absence of a new shock.

Background

On inflation, the current environment is characterized by a 3.9% y/y inflation rate, which is above the 3.0% monetary policy target. The external energy price shock pushed inflation above 3.0%, while core inflation remained well behaved at 3.2% y/y. Since Chile passed through most of the initial spike in global oil prices, it is now starting to see gasoline prices decline. If the recent decline in global oil prices sustains, the coming decline in local gasoline prices will directly reduce inflation, and indirectly cut off any remaining second-round effects from the initial price spike, accelerating the convergence of inflation down to 3.0%. Expected inflation two years ahead is well anchored at 3.0%

On activity, the BCCh has been cutting its GDP growth forecast for 2026, mainly due to the underperformance of sectors linked to natural resources. The BCCh estimates that the economy is currently working under a negative output gap, but it has characterized it as a slightly negative gap, so for now it is not considered a relevant source of deflationary pressure. Minutes for the Jun 16 meeting did mention some initial evidence of private consumption and investment weakness, but MPC members speculated that the private consumption weakness would be reversed if gasoline prices decline, and noted that investment prospects are looking strong.

Monetary policy moving forward

Since the economy works under a negative output gap and the external price shock is expected to be transitory, the consensus is that inflation will return to where it was before the shock, right at the 3.0% monetary policy target, as the shock fades over the next 12 months. This is important for monetary policy. The MPC's 3.0% inflation target is evaluated within a two-year period, so if the effects of the external shock are seen fading within this period and expected inflation two years ahead remains anchored at 3.0%, it is hard to see any immediate pressure for the MPC to hike in the short term. Of course, the story would change if the conflict in the Middle East worsens or we see another inflationary shock.

A cut appears unlikely while inflation sits above the 3.0% target, but oil prices returning to pre-March levels could accelerate the inflation convergence to Q4 or Q1 next year. The case for an earlier cut would form if the economy continues to disappoint compared to expectations, especially if it starts to show more weakness in private consumption and investment. Basically, if the negative output gap widens in a more significant way and conditions at the Strait of Hormuz continue to normalize, there could be a preemptive cut on account of medium-term deflationary pressure.

| BCCh forecasts | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Source: BCCh |

| Ask the editor | Back to contents |

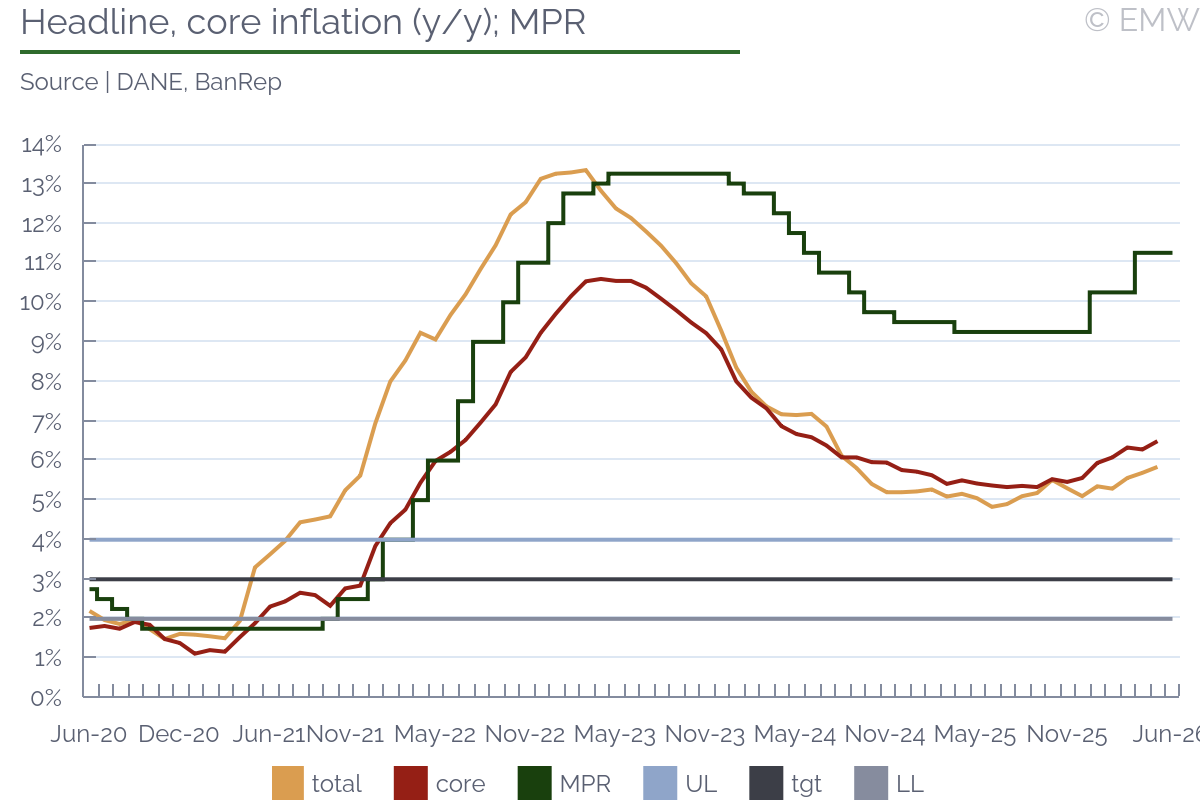

| BanRep's Jun 30 hike call splits 50-75bp as fiscal rally meets min wage shock |

- Next Board meeting: Jun 30, 2026

- Current policy rate: 11.25%

- EmergingMarketWatch forecast: Hike 50bps or 75bps to 11.75% or 12.00%

BanRep's Board of Directors is now in a stronger position. Finance Minister Germán Ávila had previously threatened to boycott the quorum. Decree 2520 of 1993 initially required the finance minister as one of the five members needed to convene the board, but the Council of State recently overturned that condition. That pressure likely contributed to the unanimous hold decision on April 30, despite a clearly deteriorating inflation backdrop. However, the June 21 victory of President-elect Abelardo de la Espriella changes the picture meaningfully. De la Espriella ran as a political outsider with little personal history with former Pres Iván Duque, but his administration leans heavily on Duque-era technocrats, starting with vice president-elect José Restrepo, who was also Duque's final finance minister. That matters for the board. Duque appointed two of its current hawkish members, Mauricio Villamizar and Bibiana Taboada, while Governor Leonardo Villar was elected to his post by the board itself in January 2021, during Duque's term. With Restrepo now inside the incoming government, the board can finally operate with less political friction after almost four years of contentious debates with an executive that repeatedly pushed for policy rate cuts. Looking further ahead to 2029, president-elect de la Espriella will be able to replace Taboada and Villamizar, or reappoint them. We think reappointing them is the safer option. Olga Acosta, whom Petro appointed and later regretted several times, and who ultimately became a swing voter backing the hawkish members, can also find some calm. She will no longer be the executive's target or be labeled by Petro's base and himself as a "traitor" for supporting the hawkish members.

On the external front, there is also good news for the June 30 meeting. The Iran-US MoU, despite recurring threats from Israeli military actions in Lebanon, has increased the odds of fully reopening the Strait of Hormuz, though the agreement only guarantees toll-free transit for 60 days. After this period, Iran and Oman are due to negotiate how the strait is administered, and Iran has already signaled it may charge a transit fee once that window lapses. That matters because input costs for agriculture and livestock, including fertilizers, have been driving food inflation, a concern for the central bank in recent months. If the US-Iran agreement holds beyond that initial window and Iran does not again threaten a prolonged closure of the Strait, one external source of pressure on inflation that began to keep BanRep wary of late should gradually fade.

On the domestic side, the bond market has reacted positively to de la Espriella's victory, with 5Y and 10Y yields moving back to Q3 2025 levels as markets price in fiscal consolidation, tighter spending, and a smaller state than under Petro's expansionary agenda. At the current policy rate of 11.25%, the one-year real rate implied by the market's 6.43% breakeven inflation now averages 4.87% month to date, while the central bank's survey points to one-year inflation expectations of 5.57%, implying an ex ante real interest rate of 5.68%. The average of those two gives a one-year real rate of 5.28%, the highest level so far this year, versus 5.10% in April. On that basis, real monetary conditions are already the tightest they've been year-to-date, so BanRep would not need a large additional hike to keep policy restrictive, as long as inflation expectations stay anchored near current levels.

| Ex-ante real interest rate and policy rate | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Source: EmergingMarketWatch; BanRep; BVC | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Even so, in our view, the market rally depends on de la Espriella fully convincing investors that he will repair public finances and make whatever adjustments are needed to reverse both the widening primary deficit and the broader central government deficit. The May inflation print also showed rising demand-side pressure stemming from the disproportionate 23% minimum wage increase decreed for this year, which has kept inflation elevated mainly through second-round effects. Prices for food away from home and HOA fees have continued to rise, as watchmen, cleaning staff, and restaurant workers are mostly paid minimum wages or wages indexed to the minimum wage. The indexation effect has also pushed up imputed rent, as landlords likely have less incentive to use the standard benchmark (the previous year's inflation rate) and instead rely on higher adjustments in recent contract negotiations amid expectations of rising inflation ahead. BanRep, therefore, cannot risk inflation expectations becoming unanchored, since that would undermine the central bank's credibility in steering inflation back to its 3% target if agents in the economy simply keep expecting prices to rise.

For that reason, our call now splits between 50bp and 75bp hike on June 30. Note that half of the real tightening above comes from market breakevens, which are election-driven and could unwind if the fiscal consolidation narrative disappoints. The deficit hasn't actually been fixed yet, only priced as likely to be fixed, and that gap between promise and execution is what could unwind the breakeven-driven easing if delivery disappoints. The May inflation print is the more direct case for front-loading, since it shows the wage shock already surfacing in realized data, not just in forecasts. Hence, our forecast sits at or above where the street consensus lands. The most recent surveys of the domestic financial sector, including BanRep's monthly expectations survey and Fedesarrollo/BVC's financial opinion survey, show economists converging on a 50bp hike. If consensus is right and CPI inflation starts drifting back down, BanRep could then wait and calibrate whether further hikes remain necessary at all. That said, BanRep has traditionally preferred to front-load, so leaning toward 75bp over 50bp is not very costly, as any further adjustment is by definition uncertain, since many inflationary pressures cannot usually be forecast accurately. With Petro out of the picture and a right-wing president in place, a hawkish board may also feel freer to act on either side of that range without worrying as much about presidential backlash.

Overall, we continue to think the minimum-wage shock, which is still filtering through the economy via higher service and HOA fees, will keep inflation rising, so BanRep's tightening cycle looks far from over. Even so, with 200bp of cumulative hikes year to date and less political friction within the board, the central bank's reaction function can now focus more on how to carry out tightening based on the central bank's staff technical recommendations, but, we believe, without sharply hurting the credit market, which has supported household consumption and allowed firms to keep headcount steady or even hire despite rising wages. Moving forward, we expect BanRep's decisions to become easier to forecast, since they will depend mainly on technical criteria, with an incoming government that, if history is any guide, will respect BanRep's independence.

| Ask the editor | Back to contents |

| Chances for rate cut on Jul 7 strengthen due to soft inflation |

- Current policy rate: 3.75%

- Next monetary policy meeting: Jul 7, 2026

- Expected decision: 25bps cut

The MPC cut the policy rate by 25bps to 3.75% on May 25 but maintained a rather hawkish tone, which was interpreted by some as a defence why it did not implement a steeper easing. The press release and comments of BoI officials after the announcement stressed on still existing risks and deputy governor Andrew Abir insisted that the geopolitical uncertainties required a gradual monetary easing. However, just over a week passed and the BoI governor Amir Yaron softened the tone significantly and suggested that the monetary easing might be faster and larger if inflation expectations continue declining and approach the lower end of the 1-3% target range. Yaron said that the situation has changed in the week that passed since the rate was cut with the likelihood for a deal with Iran increasing that affected energy prices, Israel's risk premium and the forex rate - all in the direction of lower inflation. The US and Iran did announce a deal in the meantime and inflation in Israel remained stable in May, which significantly increases the chances for a rate cut on Jul 7, in our opinion. Still, there is a risk for an on-hold decision but we think it is rather small and would not materialise unless there is a significant deterioration in the security situation.

Inflation remained stable at 1.9% y/y in Mar-May, staying at the mid-point of the 1-3% target range for the fifth consecutive month in May and within the band ever since August. Inflation surprised positively for the third consecutive month in May and was even lower than the softest among consensus forecasts. The shekel appreciation was tamed after the change in rhetoric. The BoI also purchased a significant USD 800mn, which it defined as an effort to maintain the orderly functioning by the markets but some doubted the explanation and insisted this was to contain the shekel appreciation. Even if the forex rate has stabilised, it is possible the inflation to continue benefitting from effects from the shekel strengthening and the easing of labour market restraints due to the significant reduction in fighting. Abir has commented after the May rate cut that inflation was not expected to exceed the upper end of the target (3%) even in case of a shock.

GDP declined by 3.8% in saar terms (seasonally-adjusted annualised rate) in Q1, still lower than the economic contraction in Q2 2025 when the previous war with Iran took place despite the 0.5pps downward revision in the second estimate. GDP level was by about 4.5% lower than its long-term trend would indicate, the BoI has assessed after the first release. A recovery has already started in Q2 with credit card purchases recovering and slightly exceeding their long-term trend line, stability in exports and recovery starting in imports as of April, according to the BoI. Credit continued expanding, the risk premium declined close to pre-Oct 7 2023 levels, and equity indices continued increasing. The labour market was impacted significantly by the war but has already started recovering slightly. Since those assessment new data became available but it only confirmed the trends. Thus, the economy does not seem to need support by rate cuts and the major determinant will remain inflation and the security situation, in our opinion. Both have improved meanwhile.

Board statements, press briefings, minutes from MPC meetings

| Ask the editor | Back to contents |

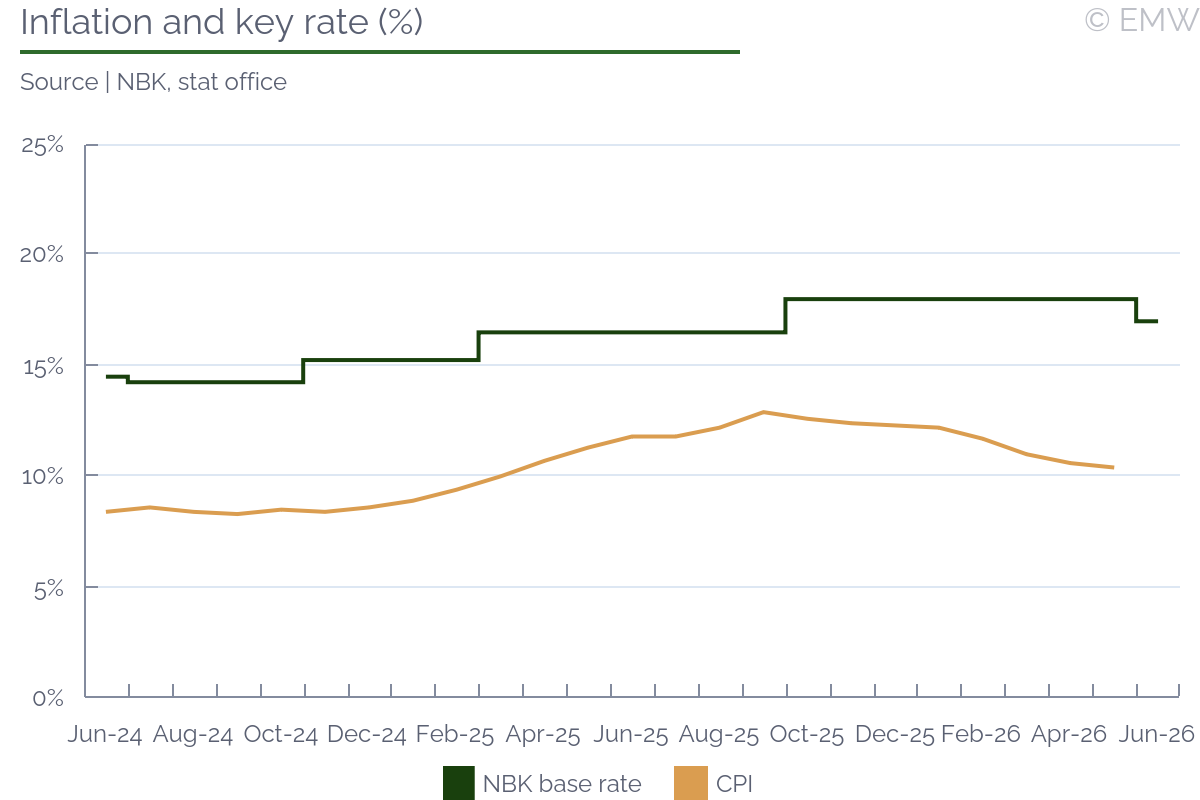

| NBK cuts base rate by 100bps, downgrades year-end inflation forecast |

- Current policy rate: 17%

- Next monetary policy meeting: Jul 24

- Expected decision: hold

On Jun 5 the NBK cut the base rate by 100bps (to 17%), starting the monetary easing cycle earlier than previously suggested. Overall, June's rate cut was certainly a possibility, since inflation has decelerated gradually. At the same time, the cut's scale came as a surprise. As outlined before, we believe the NBK's decision-making is influenced by economic growth considerations, especially after the subdued Q1 performance. We also note that the NBK has insisted its stance remains 'moderately tight' and governor Suleimenov commented that there will not be 'drastic' base rate cuts.

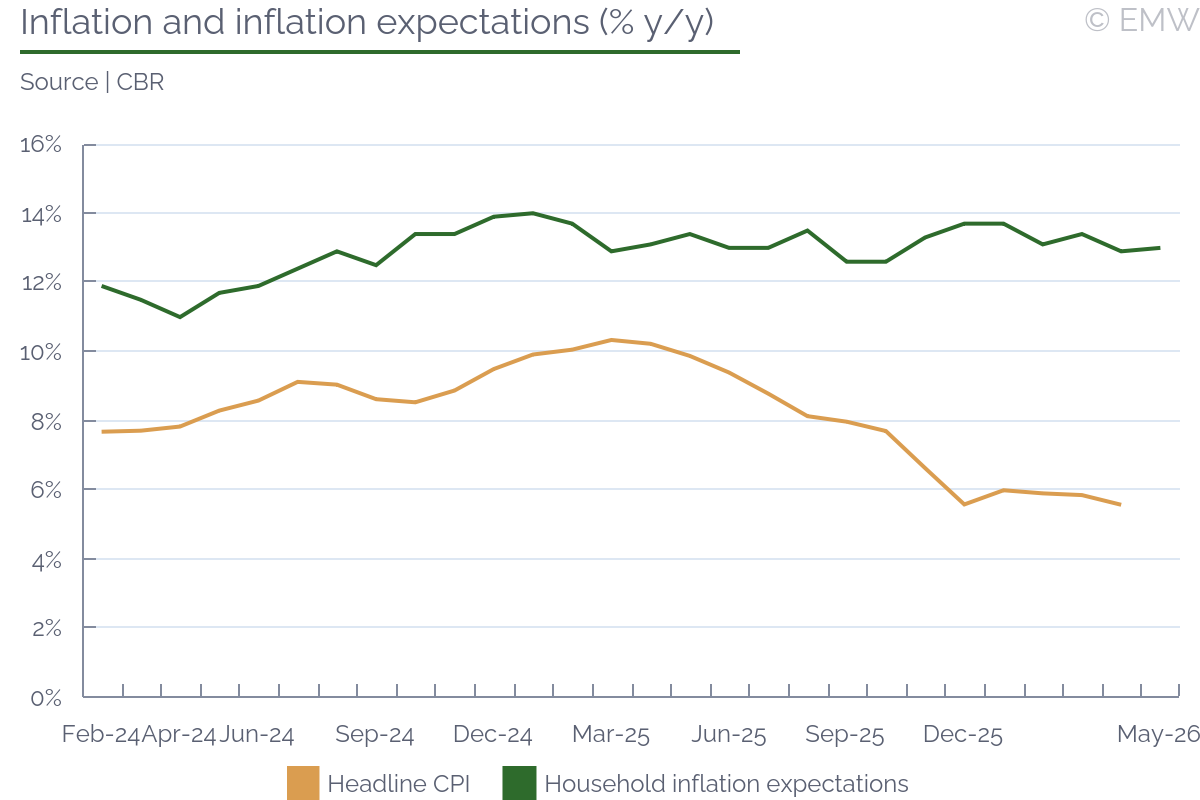

As a whole, the bank has acknowledged the continued prevalence of inflationary tendencies. The main risks it sees are related to tariff and price reform, domestic consumption, quasi-fiscal stimuli, and geopolitical tensions. We remind that households' inflation expectations were higher in May, too. While exchange rate dynamics partly absorbed inflationary pressures early in the year, the tenge's recent depreciation has negative implications. Suleimenov also admitted the national currency is unlikely to strengthen much in the near term due to 'seasonal' factors.

Nevertheless, the NBK downgraded its year-end inflation forecast to 9-11% (from 9.5-11%). In addition, it said the aim is to reach the lower end of this range. In this context, it would be even more surprising if the bank implements another rate cut in July. June's CPI rate would have to be significantly lower alongside favourable external developments. At this stage, we believe the recent 100bps cut came rather pre-emptively and the NBK will wait before continuing the easing cycle.

| Ask the editor | Back to contents |

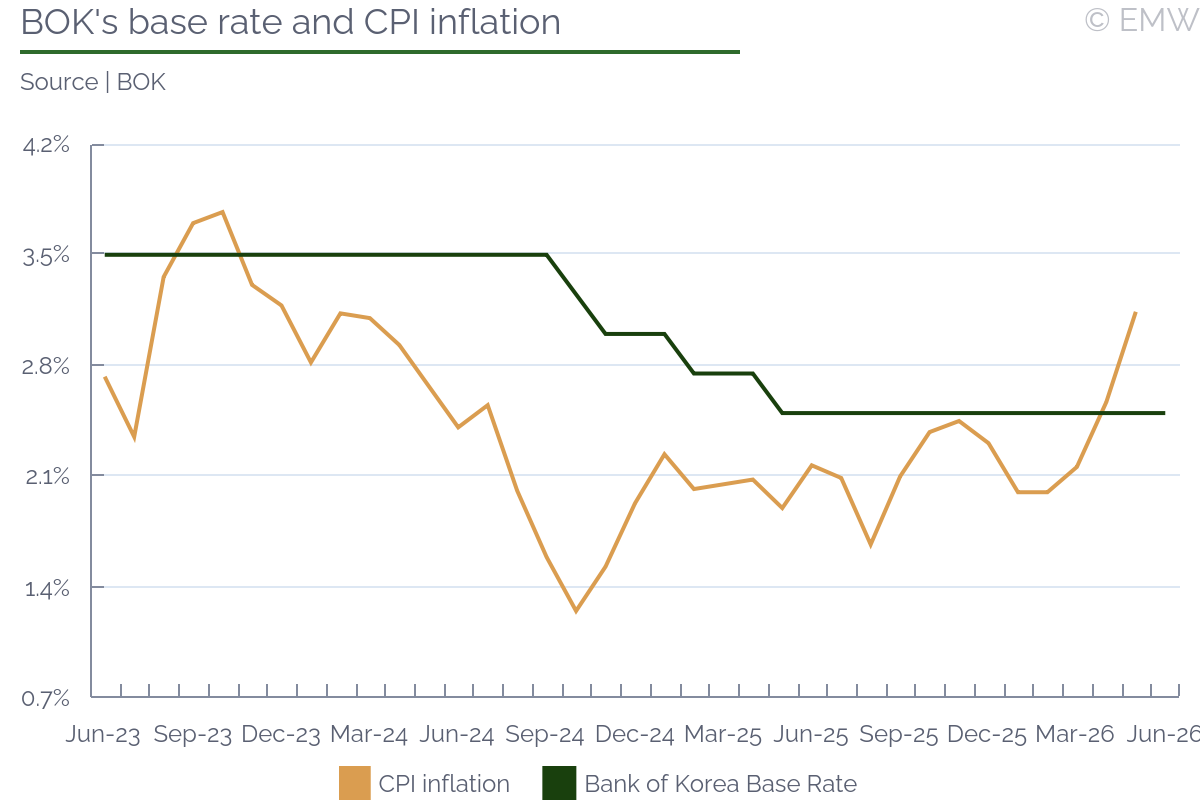

| BOK set to raise policy rate by 25bps in July as inflation pressures intensify |

- Next policy meeting: July 16

- Current policy stance: 2.50%

- Last decision: May 28 (Hold)

- Forecast: 25bps hike to 2.75%

- Rationale: Faster headline inflation, wage pressures, strong growth all point towards small rate hike in July

The Bank of Korea (BOK) looks set to raise its policy rate by 25bps to 2.75% in its upcoming meeting on July 16, in our view. The BOK's dot plot from the meeting on May 28 clearly showed that the vast majority of MPC members expect the policy rate to be raised by either 25bps or 50bps in 2026. At the same time, BOK's governor Shin Hyun-song made a hawkish comment on June 12, saying that the BOK will "focus on price stability and raise interest rates without delay." Finally, the minutes from the BOK meeting on May 28 also confirmed that a hawkish shift has occurred in the BOK, with 2 out of the 6 members already ready for a rate hike as early as the May meeting.

Despite the strong growth figures and intensifying inflation pressures, we don't think that the BOK will opt for a 50bps rate hike instead of a smaller 25bps one. The dot plot from the May 28 already suggests that 50bps cumulative rate hikes will be the limit in 2026. In addition, Shin's comments from June 12 also lead us to believe that BOK will prefer timely and gradual rate hikes, rather than a shock-and-awe large hike. Last but not least, the apparent deal to end the Iran war that was signed this week, ameliorates the inflation outlook for 2026 and will likely solidify BOK's May forecast for 25-50bps rate hikes in 2026.

CPI inflation, housing prices, credit growth and won depreciation favour rate hike

CPI inflation accelerated to 3.1% y/y in May 2026 from 2.0% y/y in February 2026 mainly as a result of higher transport prices. At the same time, core inflation has picked up from 2.3% y/y in February to 2.5% y/y in May. Overall, there are clear signs that inflation has moved above BOK's 2.0% target, which naturally puts pressure on the BOK to act.

Regarding housing prices, recent data is also not very positive as Seoul apartment prices rose by 0.28% w/w in the week ending June 8, equalling to an annualized growth rate of 15.0%. The recent acceleration in housing prices occurred after the May 9 deadline when the heavier capital gains tax exemption period ended, which had pushed additional supply into the market in the preceding period. Separately, the recent deprecation of the Korean won, which pushed the USD/KRW rate above 1,500 in May, is also likely to contribute to BOK's hawkish tone. Both housing prices and exchange rate movements are frequently discussed by the BOK as factors that can influence monetary policy.

Credit growth has also accelerated to KRW 6.9tn in May, which is the highest monthly increase so far in 2026. Strong demand for mortgage loans and acceleration in unsecured lending due to the large stock market investments made by individuals have both contributed to lending growth. The combination of higher inflation, higher housing prices and higher credit growth favours strongly a rate hike, in our view.

Economic conditions ease slightly in April, but chip sector remains buoyant

The economic conditions in South Korea have somewhat eased at the start of Q2, with industrial production moderating to 1.5% y/y growth in April from 4.2% y/y growth in March. In addition, retail sales growth has dipped to 1.6% y/y in April from 5.0% y/y in March. However, exports remain buoyant as they surged by 85.9% y/y in the first 10 days of May led by rising semiconductor prices. Thus, Korea's K-shaped economic performance remains in full force, with chip prices being the main engine of growth.